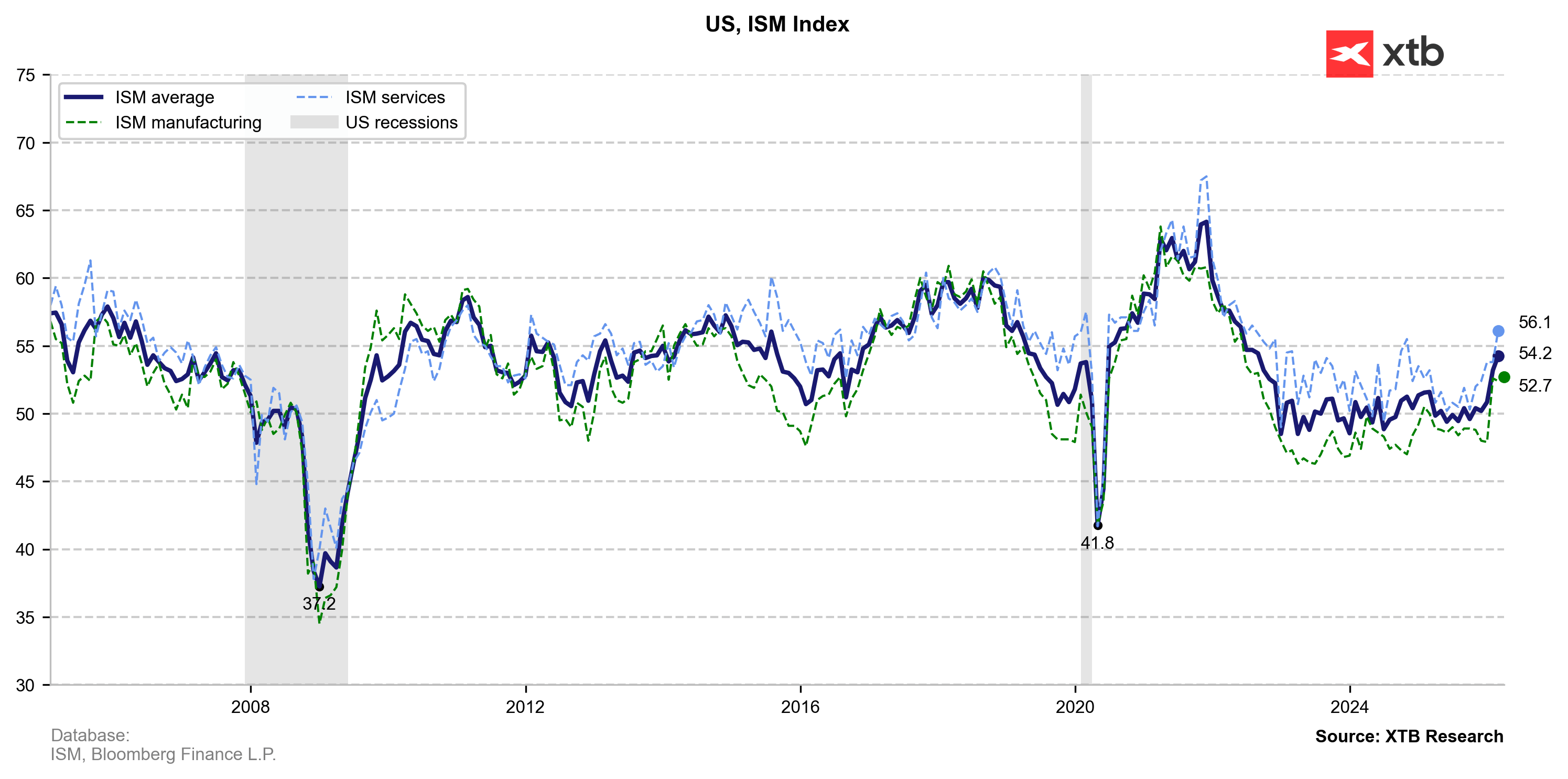

ISM Shows That, Expansion Continues But, Inflationary Pressure Surges

The headline index of 52.7 (vs. 52.5 expected and 52.4 previously) marks the third consecutive month of expansion, but the report’s internal details are cooling market enthusiasm.

- Inflationary Shock (Prices Paid: 78.3 vs. 73.0): This is the report’s critical takeaway. Input costs are rising at their fastest pace since mid-2022. Such intense price pressure (commodities, tariffs) is a major “red flag” for the Fed, pushing back the timeline for potential rate cuts, altough the market is pricing only 20-30% probability of interest hike this year.

- Sustained Recovery (Headline PMI: 52.7): Manufacturing has definitively moved past the 2025 slump. The U.S. economy’s resilience provides the Fed with more room to maintain its restrictive monetary policy.

- Waning Demand Momentum (New Orders: 53.5): While orders are still growing, the pace has decelerated compared to February (55.8). This suggests that the initial wave of New Year optimism and restocking is beginning to fade.

- Weak Labor Demand (Employment: 48.7): Despite rising production, the sector remains in contraction territory regarding hiring (reading below 50). Firms may be pivoting toward automation or trimming labor costs to offset soaring material prices.

This report is decidedly hawkish, especially looking from the inflation side. The combination of robust growth and a massive spike in input costs should support the US Dollar and Treasury yields while weighing on tech valuations (US100). The “higher for longer” interest rate scenario has just become even more plausible.

Of course, EURUSD is responding to the hope that the conflict in the Middle East will end soon. Decreasing risk in negative for the US dollar and the EURUSD is once again above 1.16, breaking above the downward trend line.

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.