Scenario Analysis – What to expect from weekend peace talks

Markets are in a jubilant mood as we lead up to the weekend. Spurred by a milder March reading of US inflation than expected, rate cut expectations are building, and stocks are rallying. Headline CPI in the US rose at a 3.4% annual rate, a hefty jump from the 2.4% rate in February, but lower than the 3.5% expected core prices rose by a 2.6% annual rate, also weaker than expected. The BLS reported that the index for energy rose by 10% in March, driven by a 21% rise in the price of gasolene.

US price growth not as bad as feared

The jump in gasolene prices accounted for three quarters of the rise in inflation last month, according to the BLS. Airline fares also rose sharply last month, but this was partly offset by a drop in medical costs and in used car prices. Today’s data suggests two things: 1, the inflationary impact from this crisis has been huge, but it is offset by weaker inflation growth elsewhere, such as a moderate increase in shelter costs, a drop in the cost of utilities and no change in food prices last month. 2, if the Strait of Hormuz is not reopened soon, then the impact on inflation could spread to food prices and to core inflation, which typically takes longer to absorb energy price shocks.

The immediate market reaction has been relief. A higher-than-expected reading for inflation could have spooked financial markets as we lead up to the weekend. Instead, this supports current expectations of a rate cut from the Federal Reserve by year end, which is boosting the market mood.

Markets optimistic about peace talks

Some concrete economic data that quantifies the effect of the war as being less onerous than first anticipated, combined with hopes for successful peace talks is helping US stocks to extend their longest winning streak this year. Rather than selling stocks on a Friday in case of an escalation of the conflict in the Middle East over the weekend, the market is willing to ‘give peace a chance.’

Stocks have strong week, as dollar reverses course

The dollar is weaker across the board on Friday after the lower-than-expected US inflation print, which is boosting hopes of a rate cut from the Fed. However, the bond market is less enthusiastic, and bonds are selling off across Europe after Forties crude from the North Sea reached a fresh record high above $147 per barrel. Until the Strait of Hormuz is fully open and Gulf energy infrastructure is operational, the bond market is likely to trade with a more cautious tone compared to stocks.

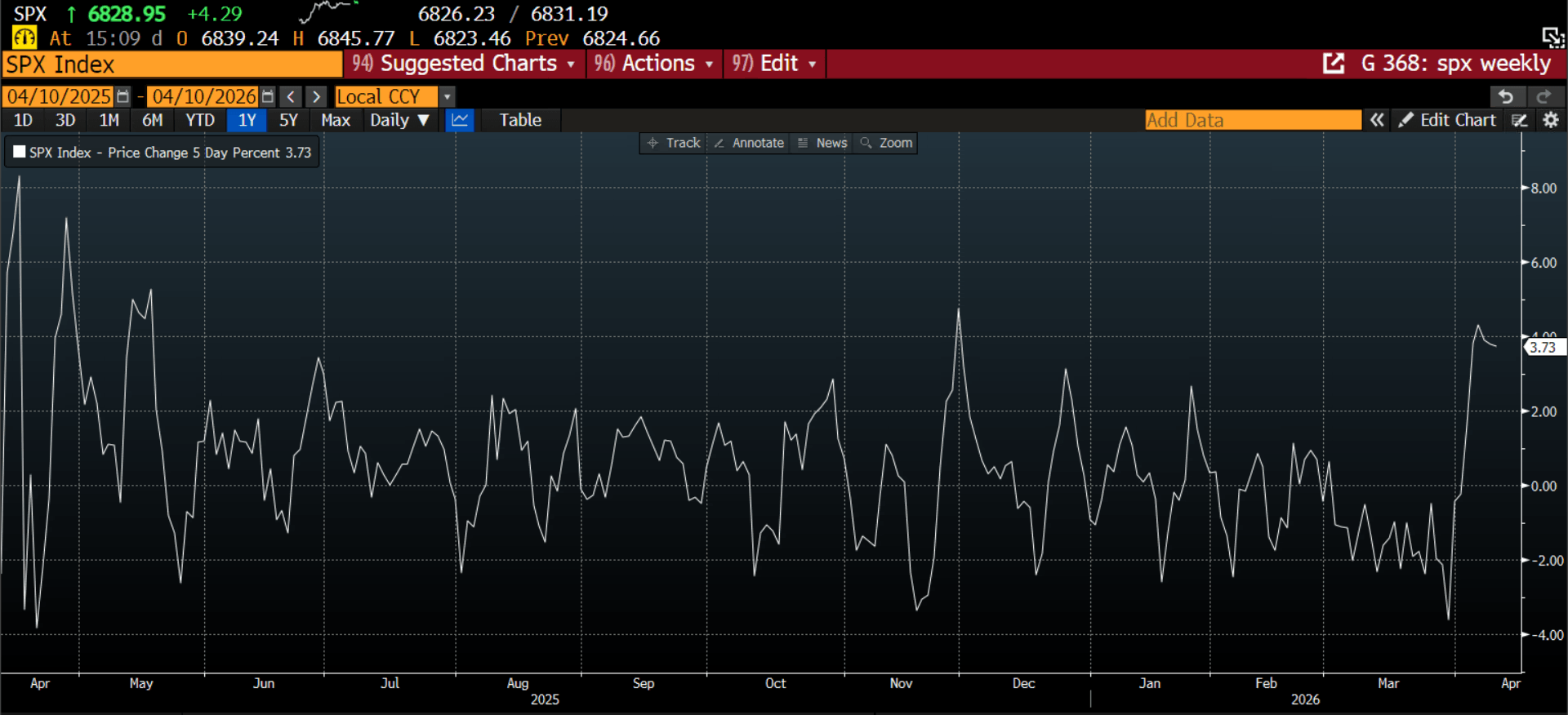

Stocks are on course for their best weekly performance of the year so far, as you can see below, and this has been spurred by the market’s conviction that President Trump will continue with a ceasefire and the conflict in the Middle East is now at its end stages. The Trump reversal index is now back at levels last reached before the war started. The market is pricing for a positive outcome from the negotiations between the US and Iran this weekend, below, we assess potential outcomes from this weekend’s talks and their impact on financial markets:

Peace talks, assessing the potential outcomes

1, Positive outcome: The two sides agree to reopen the Strait of Hormuz, which leads to an immediate reopening of the waterway. An even better outcome would be one without tariffs to pass through the Strait. The oil price is likely to fall back to pre-war levels for Brent, between $75 and $80 per barrel, stocks could surge and bonds will also rally, leading to another sharp decline in global bond yields. We believe there is a low probability, 30% or less, of this perfect outcome happening straight away.

2, Moderate outcome: The negotiations end without a deal, but more talks are expected. The prospect of prolonged negotiations could knock sentiment at the start of next week, but any weakness could fade if there are continued pledges to work towards a lasting peace. While stocks may extend this week’s rally, a high oil price could stymie further gains, especially if there is no concrete plans to reopen the Strait of Hormuz. We think that this is the most likely outcome and think there is a 70-80% chance that further talks will be needed.

3, Negative outcome: The talks fail, both sides walk away and the bombing in Iran and around the Gulf resumes. This could see the oil price reach fresh highs above $120 per barrel for Brent, stocks will tank and bond yields will surge. We believe that this is also a low probability outcome, with 10-15% chance.

Overall, the outcome of negotiations are the main focus for markets as we end the week.

Chart 1: S&P 500, weekly performance chart 1 year

Source: XTB and Bloomberg

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.