By Friday afternoon, market sentiment is dominated by fears of further military escalation in Iran. The concentration of U.S. forces in the Persian Gulf is expected to increase, and markets are increasingly concerned that any potential offensive by the U.S. and Israel could also involve Saudi Arabia. Such a scenario would represent an extreme escalation, potentially leading to reciprocal strikes on critical infrastructure across the region—from power plants to desalination facilities. Markets have largely ignored yesterday’s statement from Donald Trump, who announced overnight that the period of non-aggression toward Iran’s energy infrastructure had been extended by another 10 days, until April 4.

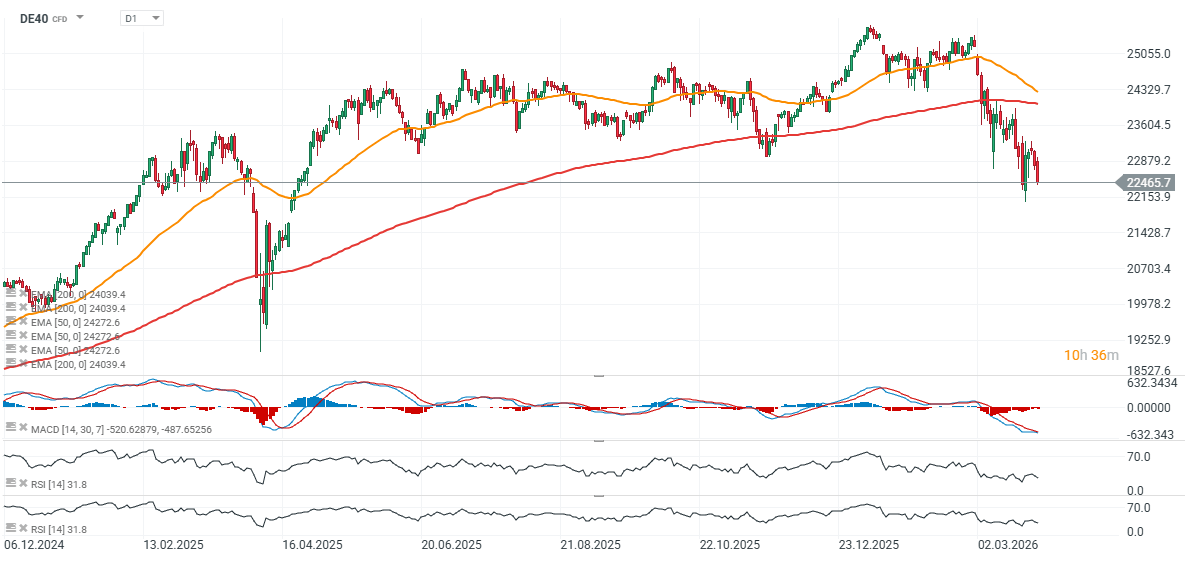

European equities are under pressure, with broad-based declines across major indices. The Euro Stoxx 50 is down more than 1.3%, while Germany’s DAX is falling over 1.5%. ECB President Christine Lagarde warned yesterday that markets may be underestimating the scale of the energy shock gradually feeding into the global economy. She highlighted that Europe could be particularly exposed through energy markets, supply chains, and critical inputs such as helium, which is essential for semiconductor production. Lagarde also noted that the shock could persist for years, with the economic adjustment unfolding gradually. European heavy industry, as well as sectors such as chemicals and logistics, appear especially vulnerable to a potential downturn driven by elevated oil and gas prices.

- The cyclical media sector is among the worst performers today, with European companies in the segment down around 3% on average. CTS Eventim is in focus, with shares plunging 16% following a disappointing full-year outlook.

- Markets remain highly sensitive to headlines regarding further military escalation, including the possibility of increased U.S. ground troop involvement in the region. Ahead of the weekend, investors are clearly reducing risk exposure.

- The Strait of Hormuz remains a key focal point for global markets. In the view of market participants, only tangible progress toward reopening the strait would provide a more durable improvement in sentiment.

- The economic impact of the conflict is increasingly visible in macro data, with recent readings pointing to a sharp slowdown in private sector activity in March. This reinforces concerns about a mix of weaker growth and rising inflationary pressures.

- Interest rate markets have also repriced expectations for the ECB. The probability of a rate hike in April has risen to around 71%, compared to expectations of no hikes for most of the year prior to the outbreak of the conflict.

- Rising bond yields are adding further pressure to equities, with the German 10-year Bund yield climbing to its highest level since 2011, reducing the relative attractiveness of stocks and increasing the cost of capital.

- Against the broader market weakness, Pernod Ricard stands out, gaining around 3% after confirming discussions regarding a potential merger with Brown-Forman, the owner of Jack Daniel’s.

- AstraZeneca is also outperforming, with shares up 3.4% after its experimental respiratory treatment Tozorakimab met primary endpoints in two late-stage trials, supporting the broader healthcare sector.

- Overall, the session reflects a consistent pattern: investors are reducing risk, bond yields are rising, and the main transmission channels of geopolitical tensions into markets remain energy prices, inflation expectations, and central bank policy.

- Earlier this week, the STOXX 600 briefly approached correction territory, falling around 10% from its February peak. However, subsequent comments from Donald Trump regarding a potential extension of the deadline for reopening the Strait of Hormuz helped to partially stabilize market sentiment.

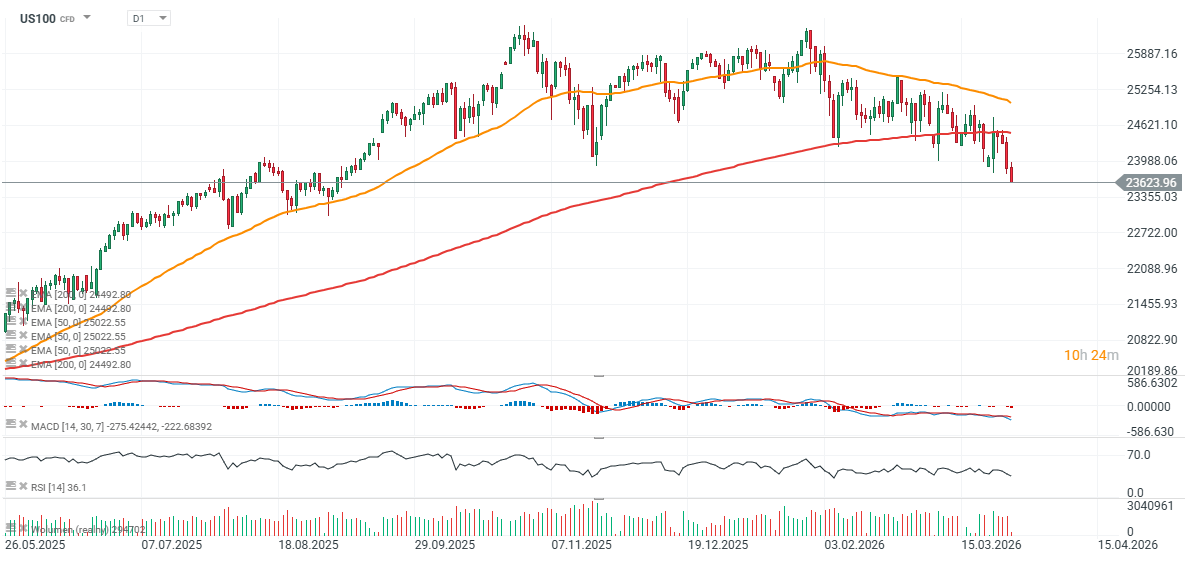

Charts: DE40 and US100 (D1 interval)

Source: xStation5

Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.