- EUR/USD broke to a fresh multi-week low this week before steadying near a tentative floor.

- The slide came despite the ECB’s first rate hike since 2023, a move forced by the energy shock rather than by strength.

- With the eurozone economy contracting, the Euro stays chained to broad Dollar direction into next week’s US data.

The Euro did something this week that ought to be impossible: it fell in the same fortnight the European Central Bank (ECB) delivered its first interest rate hike since 2023. EUR/USD slid to a fresh multi-week low near 1.1400 before clawing back to a tentative floor around 1.1450; the lesson is that not every rate hike is a vote of confidence. The ECB tightened because an energy shock forced its hand, not because the eurozone economy is firing. That distinction is why the single currency cannot turn a hawkish central bank into a rally.

A hike that smells like surrender

Look at what the ECB actually did and the bind becomes obvious. It raised the deposit rate for the first time in nearly three years while simultaneously cutting its growth forecasts and lifting its inflation projections, an unambiguous stagflation signal. Euro-area inflation has climbed to its highest in nearly three years on surging energy costs tied to disruptions through the Strait of Hormuz, even as the bloc’s economy contracted in the first quarter. Tightening into that mix is a defensive move; currency markets know the difference between a central bank hiking from strength and one hiking because it has no choice.

Out-hawked across the Atlantic

Even on the narrow question of rate differentials, the Euro is losing. The ECB paired its hike with no-preset-path guidance, which markets read as a one-and-watch rather than the start of a campaign; German Bund yields barely budged. The Federal Reserve (Fed), by contrast, held at 3.75% but revised its dot plot higher, pricing toward a hike of its own from a position of relative economic strength, with the US Dollar Index parked at a 13-month high. When both sides lean hawkish, the currency attached to the stronger economy and the firmer conviction wins; right now that is unambiguously the Greenback.

A bounce on a short leash

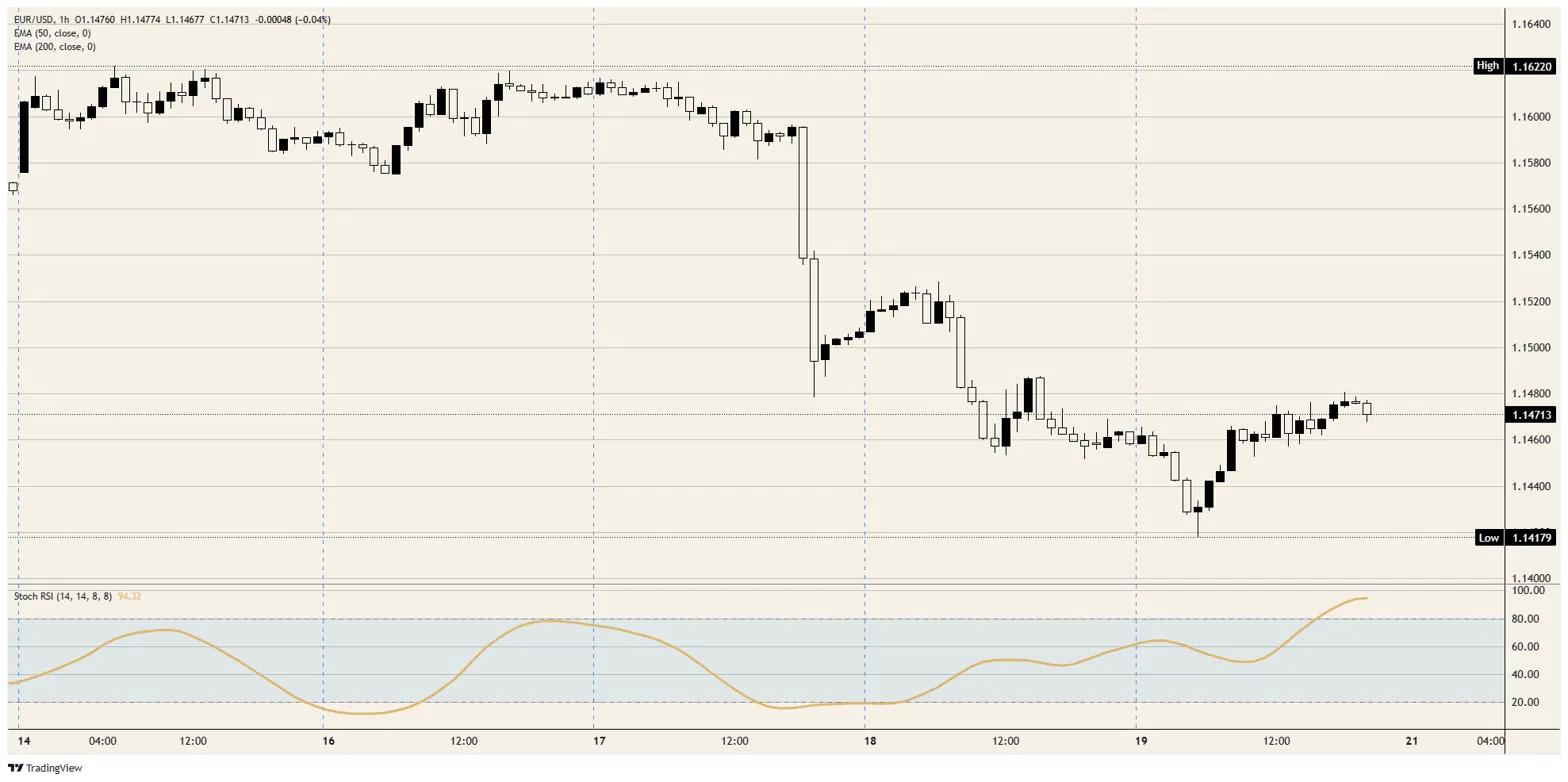

The near-term picture is the one part of the Euro story that favours the bulls, and only just. Price has carved out a tentative floor near 1.1450, with the hourly Stochastic Relative Strength Index (Stoch RSI) pushing into overbought after the bounce off the lows, a sign the immediate move is stretched. There is room for a corrective rally toward the 1.1500 area, though it stays on a short leash: the daily chart sits below both the 50-day and 200-day Exponential Moving Average (EMA), clustered near 1.1600, with the broader trend still pointing lower.

A wall of ECB speakers and Tuesday’s still-contractionary flash Purchasing Managers Index (PMI) prints will not change that calculus; whatever bounce the Euro manages is unlikely to survive a hot reading from next Thursday’s US data, when the third estimate of first-quarter Gross Domestic Product (GDP) and the May Personal Consumption Expenditures Price Index (PCE) land together at 12:30 GMT.

Resistance: The 1.1500 area is the first test, then 1.1550; the heavier barrier is the 1.1600 zone, where the 50-day and 200-day EMA converge and any recovery would have to prove itself.

Support: The tentative floor near 1.1450 is the level bulls must defend. Below it sit the 1.1400 handle and this week’s low; a clean break there reopens the downtrend.

Bias: Tactically neutral with scope for a short-term bounce toward 1.1500 while 1.1450 holds, but bearish on any longer horizon. The Euro remains a hostage to the Dollar; a hot US PCE next week is the most likely trigger to drag it back to 1.1400 and beyond. Only a soft US inflation print gives the bounce real legs.

EUR/USD hourly chart