he yen strengthened on Friday following an announcement by Japanese Finance Minister Satsuki Katayama that the government intends to encourage pension funds, including the GPIF, to increase their investments in domestic financial assets — a move that many analysts regard as potentially more effective in supporting the currency than direct intervention. The market reacted with a sharp, though so far short-lived, rebound in USD/JPY from above 162 to 161.29, representing a move of almost 0.7 per cent.

Can pension funds sustain this reversal in the trend?

The key question traders are asking is: will the government actually bring about a structural change in the GPIF’s asset allocation, or is this merely verbal intervention without any real action? Today’s reaction can be described as a ‘knee-jerk reaction’, highlighting that the sustainability of further yen purchases requires concrete commitment, not just declarations. Since 2020, the GPIF has maintained a symmetrical 50/50 allocation between domestic and foreign assets, and as recently as March 2025, the fund confirmed that it has no plans to change this structure until 2030, which is indicative of significant institutional inertia.

Investors need to see concrete action, not just words, for the trend of a weakening yen to be reversed — including more aggressive interest rate rises by the BOJ, a reduction in the fiscal deficit, and a genuine change in the GPIF’s asset allocation. This does not alter the fact that even a slight ‘structural shift’ in the allocation would have a huge impact given the scale of the fund, whilst supporting the currency, bonds and shares. History shows, however, that the GPIF has already made radical shifts in its allocation (for example, in 2014 it reduced the share of domestic bonds from 60% to 35%, whilst increasing its equity holdings), so the scenario of a change is not unrealistic, but it requires a formal decision by the fund’s board, not merely a comment from the minister.

Kumiharu Shigehara, the former chief economist at the BOJ, offers a different perspective in the debate, warning that a weak yen is not a strength, but a warning sign — real wages in Japan have been falling for four years running, and the benefits of depreciation mainly go to exporters and asset holders, whilst households pay a higher price for imported energy and food. In his view, a sustained strengthening of the yen requires fiscal credibility, normalisation of monetary policy and productivity growth — not mere rhetoric or intervention.

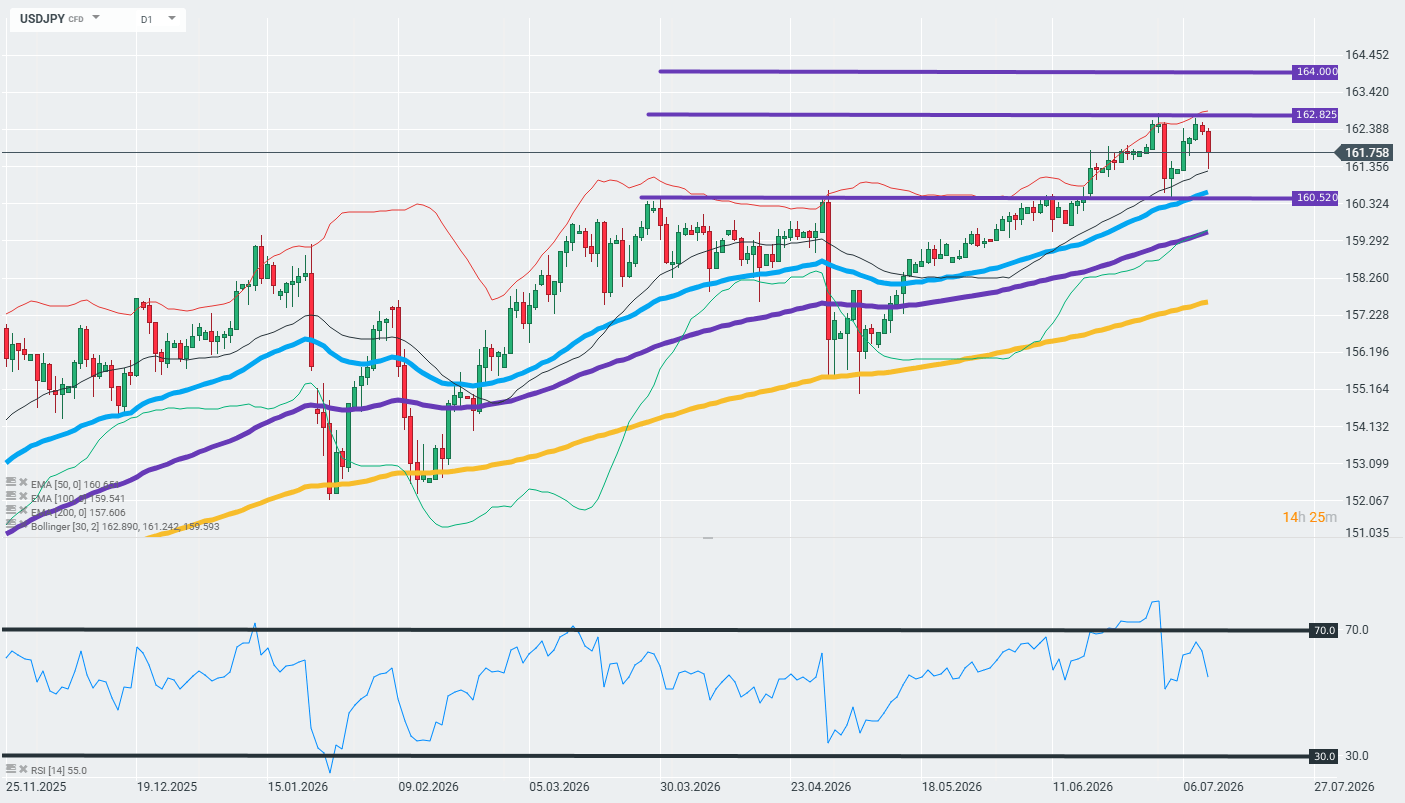

Technical analysis of the USD/JPY chart

The USD/JPY daily chart shows a clear, long-term uptrend that has been in place since November 2025, with the price consistently holding above all three EMAs (50, 100, 200), which confirms the strength of the trend.

- Short-term resistance: 162.825 — the high from recent sessions, from which the price has just rebounded lower following the news about the GPIF

- Long-term resistance: 164,000 — the next target level should the trend continue

- Key support: 160.520 — former resistance from March–April 2026, now acting as structural support, coinciding with the 50-period EMA (160.65)

The market reaction to Katayama’s comments shows a typical ‘sell the rumour’ pattern following a strong rally — the price is testing the resistance level at 162.825 and is being rejected back towards the support level at the EMA50/160.520, but this has not yet broken the main uptrend (higher lows since November).

Is the movement sustainable?

The answer is: probably not in the short term, unless the GPIF takes a formal decision to change its strategic allocation. Fundamental differences in interest rates between the US and Japan, geopolitical tensions surrounding Iran and Japan’s growing fiscal deficit are structural factors that continue to weigh on the yen, regardless of government statements. Until we see concrete steps — a genuine revision of the GPIF’s allocation, a more hawkish BOJ or progress in fiscal consolidation — Friday’s strengthening can be viewed as a technical correction within the USD/JPY uptrend, rather than a reversal of that trend. However, should a genuine change occur, the directional move could unfold very rapidly, given that investors have long been accustomed to the JPY’s tactical weakness against the USD.