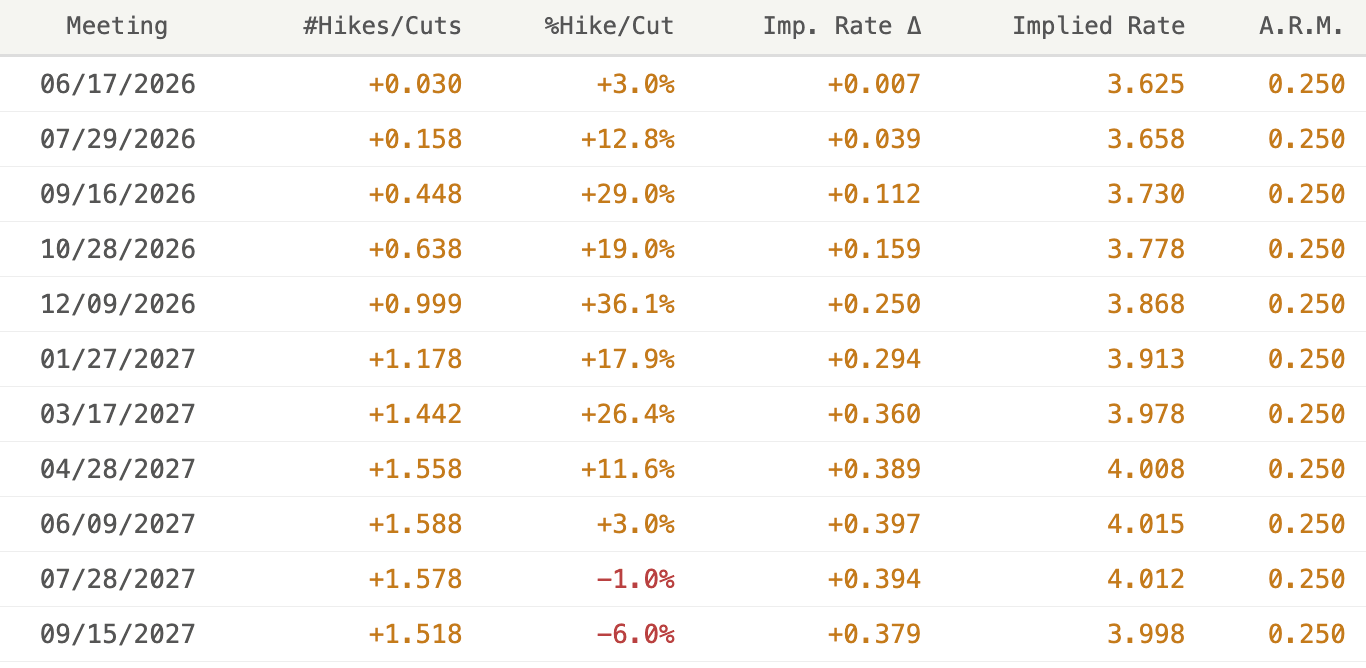

This week’s key macro data, US CPI Inflation, is set to be released at 1.30 PM. At 1:30 PM, this week’s most critical macroeconomic data will be released – May’s CPI inflation in the United States. Following the shock triggered by Friday’s NFP report, investors are frantically searching for any arguments suggesting that monetary policy tightening will not be necessary after all. A decline or stabilization in price pressures could be key – yet very little points toward such a scenario. Futures-based pricing of US interest rates currently factors in a hike in the fourth quarter of the year. This hawkish repricing is supported not only by signs of stabilization in the labor market and signals of dynamically rising price pressures, but also by the fading prospect of an agreement between the US and Iran. Figure 1: Market-Implied FOMC Rate Pricing (2026 – 2027)

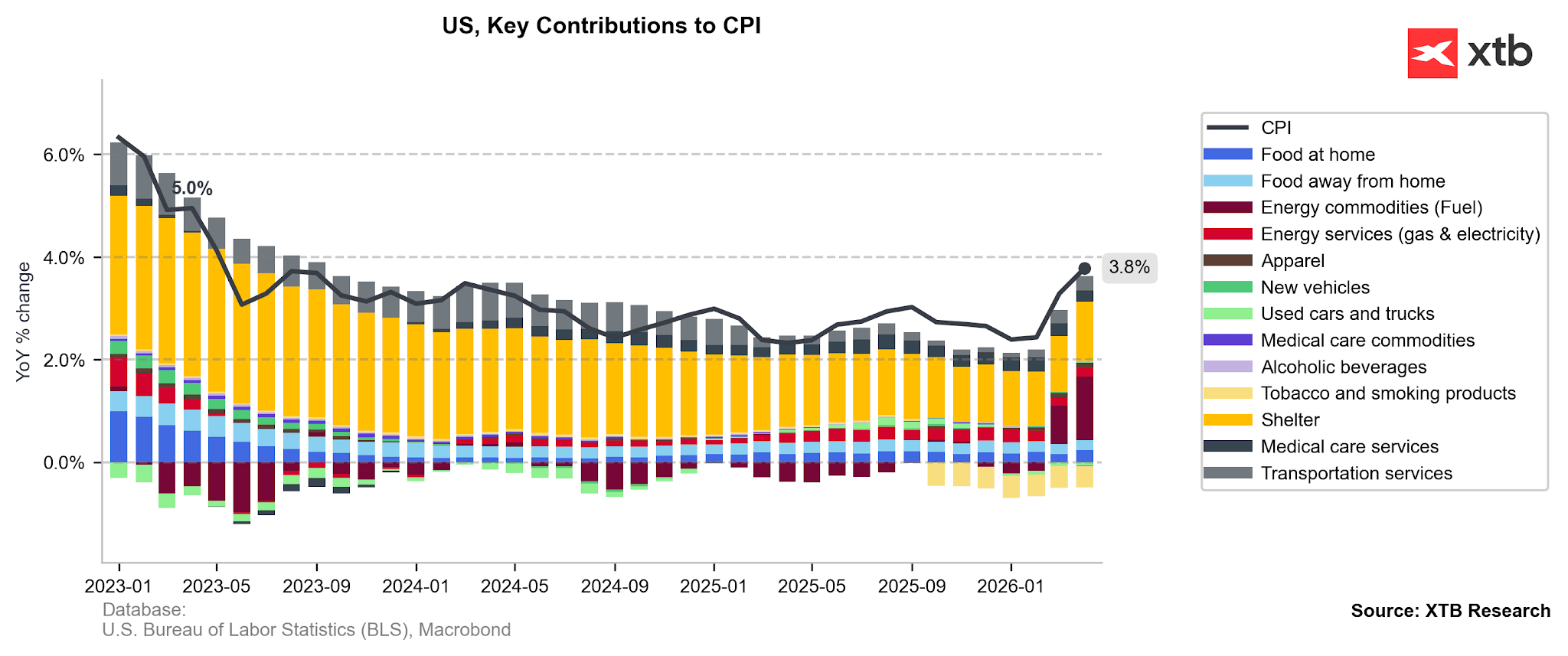

Source: Bloomberg, 12.05.2026 Headline inflation rose to 3.8%, its highest level since May 2023. Core inflation also surprised to the upside, growing by 2.8% YoY and 0.4% on a monthly basis. The greatest concern at the time was triggered by higher momentum in core services inflation (3.3%)—a metric that reliably reflects deeply entrenched price pressures. Today, perhaps somewhat unexpectedly, we will be closely watching highly volatile food (3.8% in April) and energy prices (17.9% in April). If they show high values again, they could unanchor inflation expectations at elevated levels. This, in turn, could translate into higher wage growth and consumption down the road, creating so-called second-round effects. Figure 2: Sector Contribution to the Change in Annual US Inflation Dynamics (2023 – 2026)

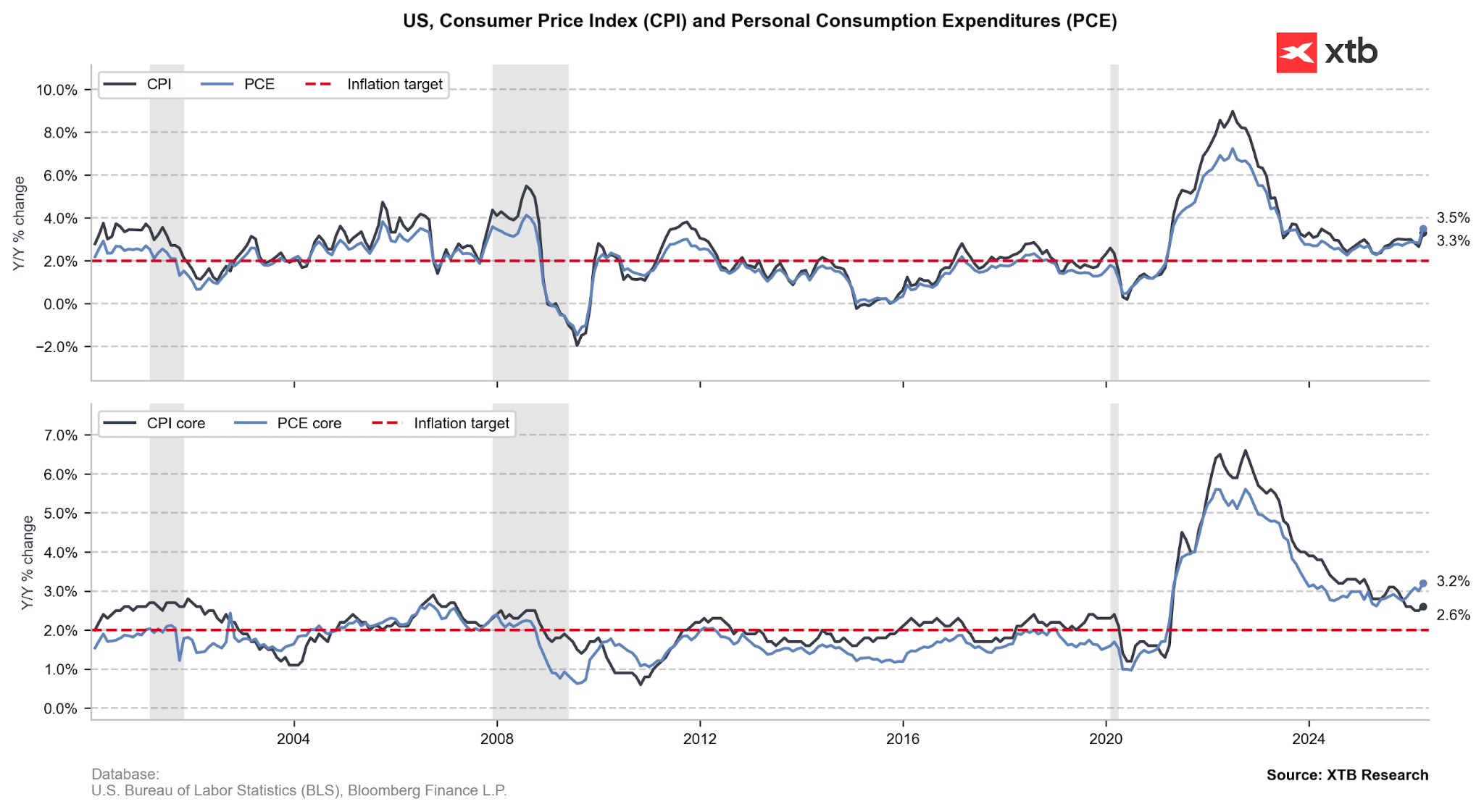

Source: XTB Research, 10.06.2026 Indeed, the average consumer feels inflationary pressure not in core terms, but in nominal terms, with a disproportionately heavy emphasis on fuel and food prices. A rise in the headline metric will not, in itself, serve as an argument for a rate hike, as it is inherently treated largely as transitory—the core metric is far more valuable in this regard. However, it could drive up inflation expectations, which would be highly significant information for the Committee. This could lead to higher wage growth and consumption in the future, creating so-called second-round effects. Figure 3: US CPI and PCE Inflation (2000 – 2026)

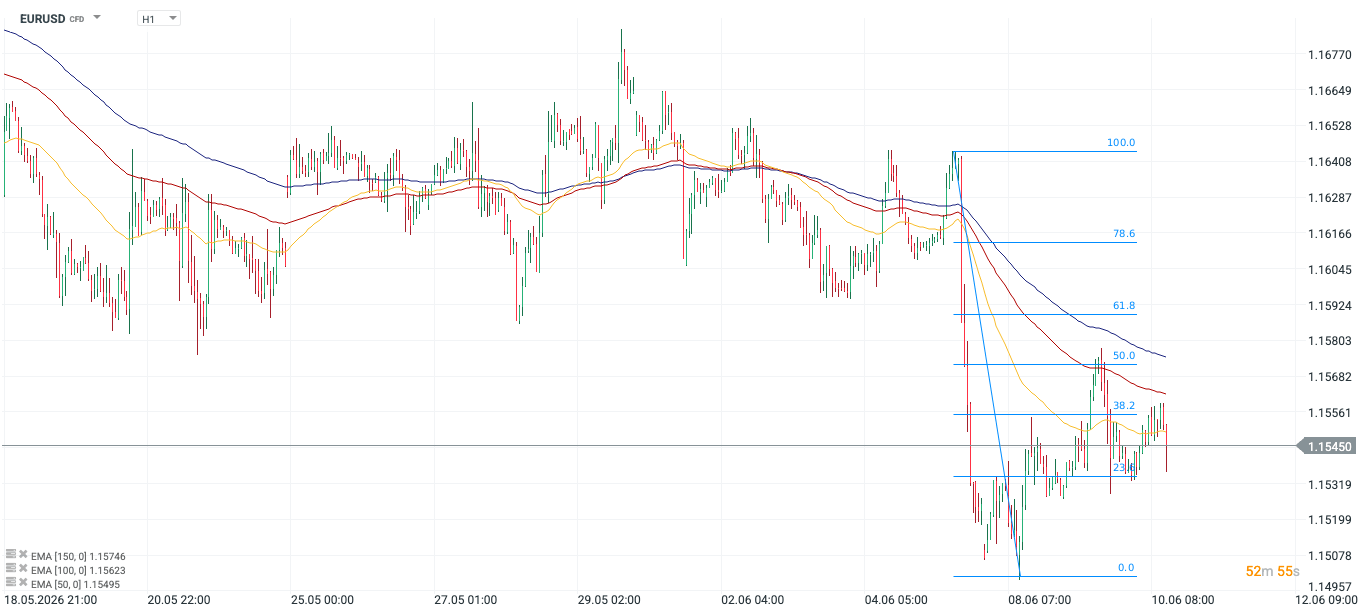

Source: XTB Research, 10.06.2026 Ahead of the reading, the dollar is weakening very modestly against the euro—by 0.1% on the day and 0.2% compared to Monday’s opening. Aside from speculation regarding May’s inflation level, attention is anchored on headlines from the Middle East and tomorrow’s ECB decision, where the central bank will most likely raise interest rates for the first time since 2023. Figure 4: EURUSD (18.06 – 10.06)

Source: xStation, 10.06.2026