Defense stocks fall after NATO Summit – Rheinmetall drops 4%, KNDS suspends IPO

Key takeaways

- Rheinmetall is down nearly 4% despite maintaining a highly favorable long-term outlook for European defense spending.

- Investors are increasingly focusing on contract execution and operational performance rather than additional political commitments to higher defense budgets.

- KNDS’ suspended IPO suggests that institutional investors have become significantly more cautious toward the European defense sector.

- Weaker sentiment is also evident across other major European defense stocks, including BAE Systems, Dassault Aviation, Leonardo, Saab, and Kongsberg Gruppen

Shares of Rheinmetall (RHM.DE) are down nearly 4% following the NATO summit in Ankara, while the broader European defense sector is also trading under pressure despite the alliance reaffirming its commitment to strengthening military capabilities. The move may signal that investors are shifting away from buying the defense narrative and are beginning to evaluate companies based on execution and fundamentals.

Good news does not always mean a higher share price

At first glance, the market reaction appears counterintuitive. NATO has effectively confirmed the long-term trend of rising defense spending, while Europe’s largest defense contractors continue to enjoy record order backlogs. In theory, Rheinmetall shares should be moving higher. The problem is that markets price the future, not the present. Much of the positive news has already been reflected in share prices following the extraordinary rally of the past two years. Once valuations become elevated, investors begin asking different questions: How quickly can companies execute their contracts? Can they maintain margins? Will political commitments ultimately translate into sustainable earnings and free cash flow? This is a classic transition from trading the narrative to trading the fundamentals.

Investors now care about execution, not promises

A good example is Germany’s cancellation of the troubled F126 frigate program. Berlin’s decision demonstrated that even record defense budgets do not guarantee smooth execution of military projects. Procurement procedures remain lengthy, while delays and cost overruns continue to affect major programs. Following that announcement, Rheinmetall entered its sharpest correction phase, with weakness spreading across the broader European defense sector. Investors increasingly recognize that the biggest risk for defense contractors is no longer a lack of demand, but rather their ability to execute contracts efficiently and governments’ willingness to deliver on ambitious procurement plans. Another factor influencing sentiment is the geopolitical backdrop. President Donald Trump recently expressed confidence that the war in Ukraine could eventually come to an end, arguing that Russia may ultimately have to soften some of its demands. At the same time, his support for expanding Patriot missile production in Ukraine and providing additional security guarantees suggests Washington intends to negotiate from a position of strength while Russia continues to face economic challenges and limited progress on the battlefield. If the war were eventually to move toward a frozen-conflict scenario, some investors may begin questioning whether Europe’s current rearmament momentum can be sustained. Rising fiscal deficits and shifting political priorities could reduce the urgency of massive defense spending over the coming years.

KNDS’ suspended IPO says more than another earnings report

Perhaps the clearest indication of changing investor sentiment came from KNDS’ decision to suspend its planned IPO. The company did not postpone its listing because of weak fundamentals. On the contrary, KNDS reported an order backlog exceeding EUR 33 billion and expects revenue to grow by roughly 30% next year. The issue was valuation. Shareholders concluded that institutional investors were no longer willing to pay the multiples that seemed achievable only a few months ago. That decision may prove to be one of the strongest signals yet that global capital is becoming more selective toward European defense stocks.

Not the end of the bull market, but a new phase?

This does not necessarily mark the end of the long-term bull market for European defense companies. The sector’s fundamentals remain arguably the strongest since the end of the Cold War. Europe is likely to continue increasing defense spending for many years regardless of short-term political developments. What is changing is the way investors value these businesses. Until recently, announcing another defense spending package was often enough to push share prices higher. Today, investors want to see new factories, higher production capacity, expanding margins, and growing free cash flow. That suggests the next phase of the defense investment cycle may be driven far more by operational execution than by political headlines alone.

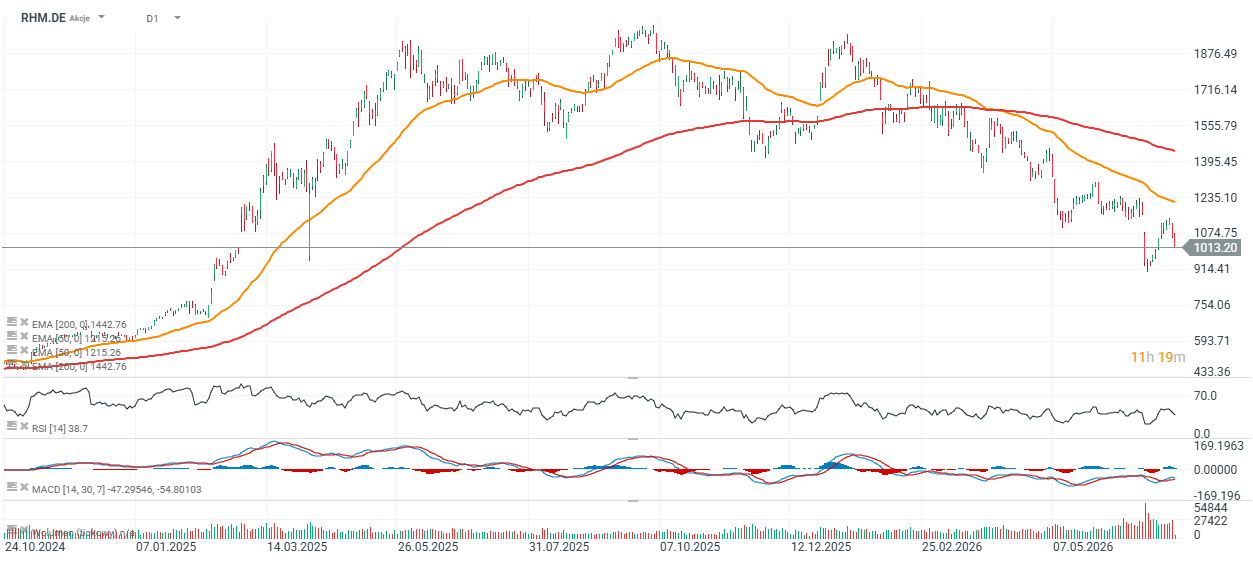

Rheinmetall (D1 chart)

Rheinmetall shares have fallen by approximately 50% from their all-time highs and are currently trading around 30% below the 200-day exponential moving average (EMA200, red line). The chart continues to point to a deeply negative trend and reflects persistent investor pessimism, as many market participants continue taking profits—or, in some cases, cutting losses—following the stock’s extraordinary rally over the past two years.

Source: xStation 5