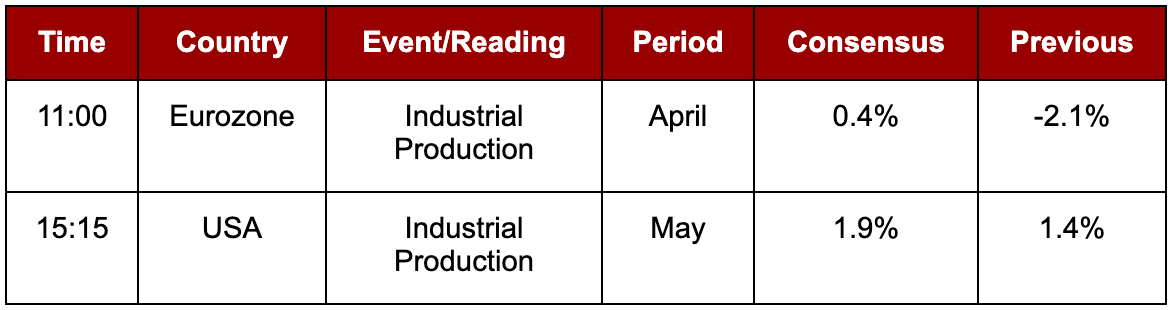

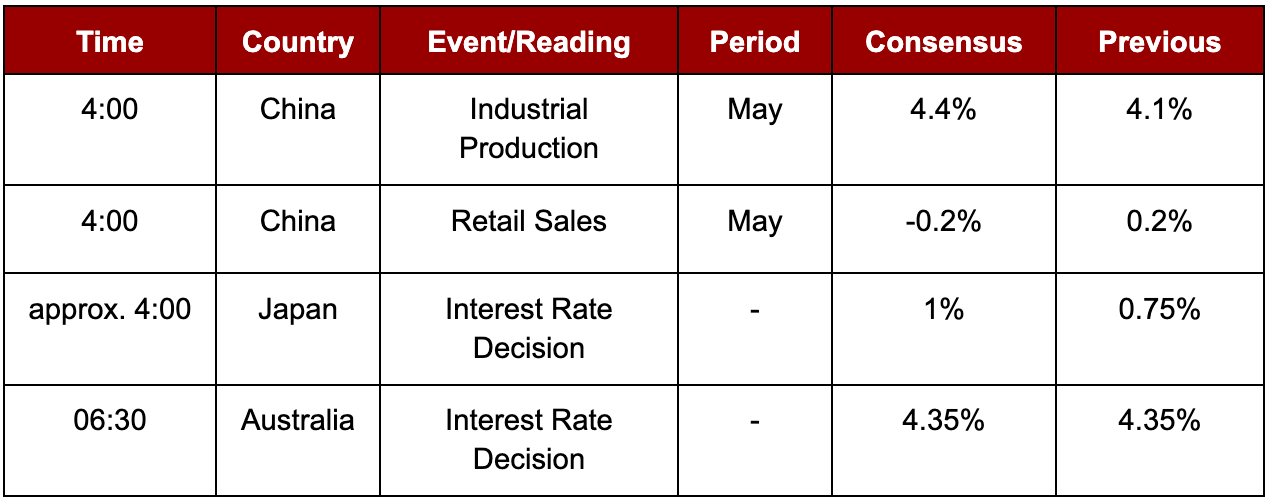

Today, the markets are predominantly driven by the agreement reached between the US and Iran, which is overshadowing all macroeconomic releases from major economies. These readings are quite scarce anyway. On Friday evening, we only received soft data regarding consumer sentiment and inflation expectations from the University of Michigan. Scheduled for today is the publication of industrial production data for the Eurozone (April) and the United States (May). However, investors are already looking ahead to tomorrow’s monetary policy decisions in Australia and Japan, which will kick off a highly intensive week on this front. There are strong indications that the Bank of Japan will opt for another interest rate hike, raising the benchmark rate to 1%.

Macroeconomic Data Friday

- The June University of Michigan report proved promising:One-year inflation expectations declined to 4.6% (from 4.8% the previous month).Five-year expectations dropped even more significantly (from 3.9% to 3.4%).The consumer sentiment index rose to 48.9 (compared to 44.8 in May).

- One-year inflation expectations declined to 4.6% (from 4.8% the previous month).

- Five-year expectations dropped even more significantly (from 3.9% to 3.4%).

- The consumer sentiment index rose to 48.9 (compared to 44.8 in May).

Macroeconomic Calendar Monday

Tuesday

Earnings Calendar US

- Canopy Growth (CGC.US) – BMO (Before Market Open)

- Quantum (QMCO.US) – AMC (After Market Close)

- Dave & Buster’s Entertainment (PLAY.US) – AMC (After Market Close)

- Nuvve Holding (NVVE.US) – AMC (After Market Close)

- Regencell Bioscience (RGC.US) – AMC (After Market Close)

3 Markets to Watch Crude Oil (OIL)

The announcement of the agreement between the US and Iran led to a nearly 4.5% drop in Brent crude prices. The signing of the deal is scheduled for this coming Friday. In the meantime, the Strait of Hormuz will be demined.

Gold (GOLD) The decrease in global geopolitical anxiety has paradoxically led to an increase in precious metal prices, which we attribute primarily to falling treasury bond yields worldwide. However, the price of gold still remains close to its 2026 lows.

NIKKEI 225 (JP225) Today’s news from Washington allowed the index to gain nearly 5%. The Bank of Japan (BoJ) meeting awaits us overnight from Monday to Tuesday, which is expected to bring an interest rate hike. The forward guidance outlined by policymakers will be crucial for both the yen and the NIKKEI 225.