Major European indices are holding near record highs during Monday’s trading, although movements vary by country and sector. The STOXX 600 is up slightly, with the benchmark index holding near all-time highs after its best week since May; the UK100 (+0.16–0.17%) and W20 (+0.16%) are gaining, while the DE40 (-0.10%) and EU50 (-0.12%) are losing ground.

The main driver of market sentiment is the wave of mergers and acquisitions in Europe, particularly the announcement of Castlelake’s acquisition of easyJet for 5.5 billion GBP, which led to gains in the transportation and media sectors, as well as the easing of tensions in the Middle East following the resumption of oil flows through the Strait of Hormuz.

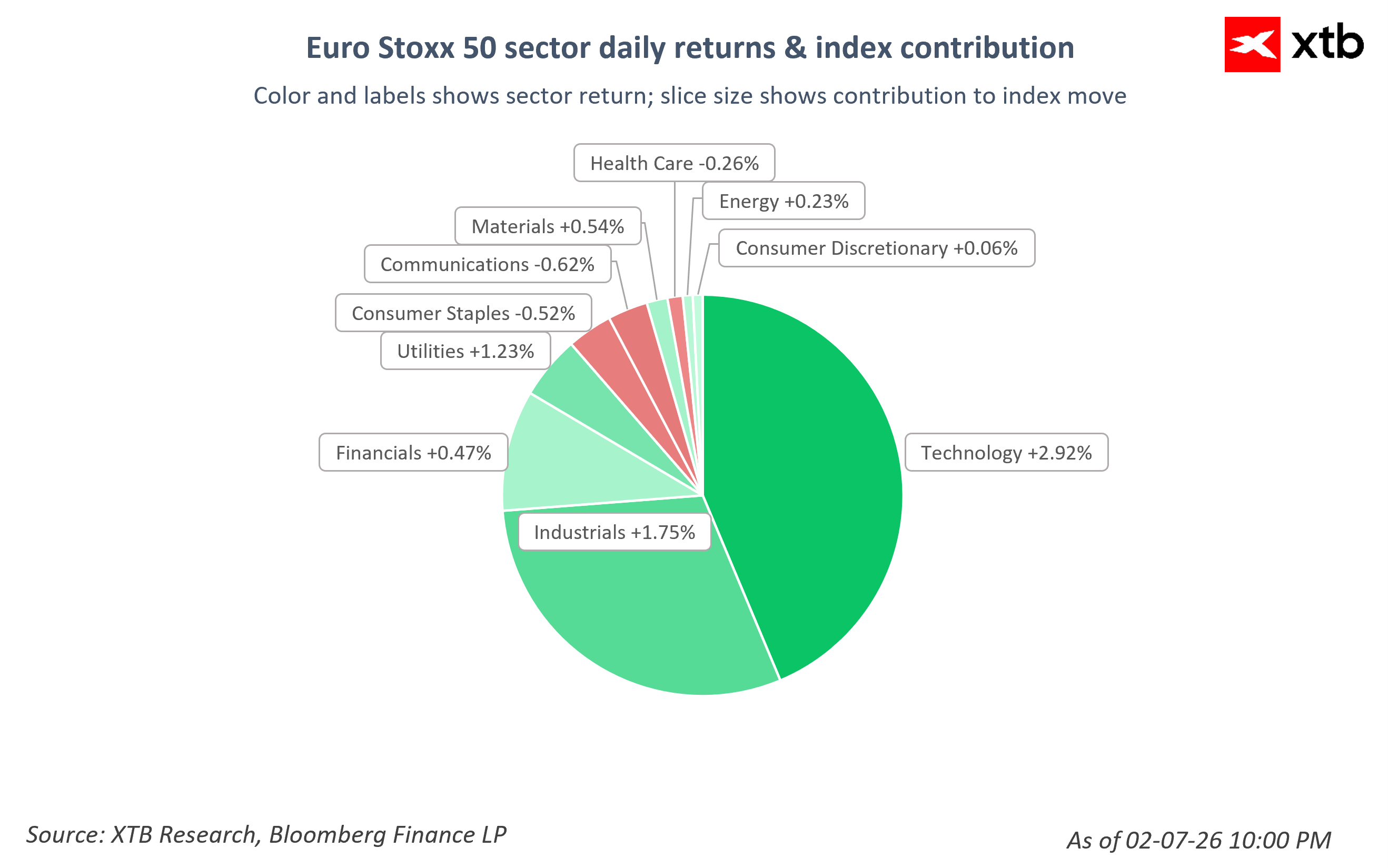

Oil prices are falling following OPEC+’s decision to increase production by 188,000 barrels per day starting in August—Brent fell 1.4% toward four-month lows near $71, while WTI CFDs are trading at 68.63–68.69 (-0.13%). The U.S. dollar is strengthening slightly; the USD index (USDIDX) is up 0.22% to around 100.8, and against the yen, the dollar is approaching 40-year highs at 162.3, while the euro is weakening to 1.142. Among the sectors, technology is performing the best (+2.92% in the Euro Stoxx 50, with the greatest impact on the index), along with industrials (+1.75%) and utilities (+1.23%), driven by mergers and optimism surrounding AI.

The worst performers are transportation (-0.62%), basic consumer goods (-0.52%), and healthcare (-0.26%); at the company level, commodities are also under pressure—gold is down 0.49% and silver 0.40%, Corporate Information Transportation decisions and developments in the deal-making sector are generating the most excitement in the market today.

Maersk and Hapag-Lloyd are plummeting (Maersk down as much as 9%, its worst day since May; Hapag-Lloyd down 4.6%) following the announcement that their joint service through the Suez Canal will resume, which threatens to put pressure on freight rates and profits after months of bypassing the Red Sea.

Where did the name “Eldorado” come from?

Since the Houthi attacks in the Red Sea in 2023, most carriers, including Maersk and Hapag-Lloyd, have rerouted their ships along the longer route around the Cape of Good Hope, which added 10–14 days to Asia-Europe voyages. This forced reroute absorbed approximately 2 million TEU of fleet capacity—or about 8% of the global container fleet—which artificially limited available supply and kept freight rates 25–40% higher than before the crisis. For shipowners, this was effectively a “free” mechanism for limiting the oversupply of vessels, which drove record profits despite structural overinvestment in the fleet.

Why is it ending now?

The decision by Maersk and Hapag-Lloyd to resume their joint Gemini service via the Suez Canal signals that carriers consider the security situation in the Red Sea stable enough to begin a “gradual return” to the trans-Suez corridor. A return to the Suez route shortens voyages and releases previously frozen shipping capacity onto the market, which—as Bank of America warned back in February—will exacerbate the existing problem of structural oversupply of vessels. HSBC analysts estimate that a faster-than-expected return to normalcy could mean an additional drop in freight rates of up to 10%, which would pose a real threat of losses to Maersk and Hapag-Lloyd. Maersk itself warned as early as February that falling rates, combined with the influx of new ships, could result in a drop in profits of up to 50 percent in 2026.

What the Numbers Say

Long-term contracts on key routes—Far East to Northern Europe and Far East to the Mediterranean—had already fallen to their lowest levels since before the crisis at the start of the year, at times even dipping below spot rates. This shows that the market is pricing in a further erosion of the “war” premium in advance. It is worth noting, however, that the latest readings of the Drewry World Container Index rose by 9% in July to $4,530 per 40 -foot container, mainly due to a seasonal peak in demand and FAK/PSS rate increases on trans-Pacific and Asia-Europe routes—which proves that the normalization process will not be linear and that short-term rebounds may occur.

What does this mean for airline stocks?

The market reacted unequivocally negatively to today’s decision by Maersk and Hapag-Lloyd—it is precisely the fear of the end of this “safety premium” that lies behind today’s sell-off of both companies, not the operational event itself. The Suez Canal Authority forecasts a full return to normal traffic in the second half of 2026, which means that pressure on shipping companies’ rates and margins will intensify in the coming quarters, and investors are already beginning to price in the end of the sector’s structurally elevated profitability.

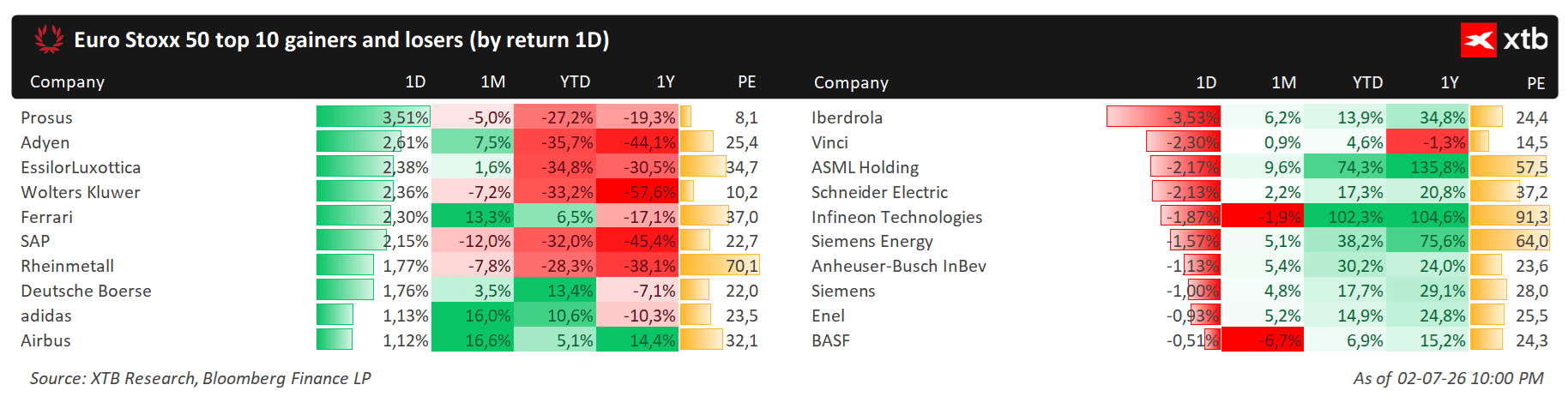

- easyJet is up more than 10% to its highest level since 2022 after accepting an improved takeover offer from Castlelake worth 5.5 billion GBP (6.90 GBP per share), though investors remain cautious about EU regulatory requirements and shareholder approval.

- Carlsberg shares rose as much as 3.7% following the formation of a strategic joint venture with Sapporo, which will bring the Danish brewer $643 million in cash and accelerate its debt reduction, increasing the likelihood of a new share buyback.

- Exail Technologies is up 2.5% (more than +50% year-to-date) following its acquisition by Thales, reflecting the growing demand for underwater drones sparked by the crisis in the Strait of Hormuz.

- BE Semiconductor is down 7.5% following reports from South Korea about a possible further delay in the full implementation of hybrid bonding technology, which is weighing on the tech sector despite positive sentiment surrounding AI.

- KGHM announces further expansion outside Europe (Morocco, Argentina, Canada, the U.S.), while Airbus is informally aiming for more than 900 deliveries this year following a strong June, while maintaining its official forecast at 870 units.