Meta Platforms will report earnings today 🗽What will social media giant show?

Meta Platforms (META.US) is set to report its Q1 2026 results at one of the most demanding moments for the broader technology sector. While expectations for revenue and earnings are elevated, the real focus of this release is shifting toward three key areas: the scale and trajectory of CAPEX, the pace of AI monetization, and the quality of forward-looking signals. In particular, whether the company maintains its aggressive AI investment plan—estimated at up to $115 billion in 2026—will be critical, as commentary on this front could influence valuations across the entire AI infrastructure value chain, including companies such as Arista Networks and CoreWeave.

High expectations and the role of AI in driving growth Market consensus points to revenue in the range of $55.4–$55.5 billion and EPS of approximately $6.65–$6.67, implying around 30–31% year-over-year growth. This would mark the strongest growth rate since 2021, primarily driven by continued improvements in advertising efficiency through AI and increasing monetization of the user base. At the same time, it is important to note that Meta enters this period following a series of optimization measures—including a roughly 10% workforce reduction—aimed at freeing up resources for AI investments. This combination of strong top-line growth, cost restructuring, and rising CAPEX will be central to assessing the quality of the results.

CAPEX as a benchmark for the broader market The most important aspect of this report may not be the quarterly figures themselves, but rather the update on investment plans. Meta is currently one of the largest investors in the global AI race, and its spending on infrastructure—spanning data centers, chips, and model development—represents a major driver of demand across the sector. The market will be particularly sensitive to whether the company maintains its current CAPEX trajectory or adjusts it in response to macroeconomic volatility and cost pressures. Sustaining elevated investment levels would likely be interpreted as a strong signal of continued momentum in the AI cycle, supporting valuations of infrastructure providers such as Arista Networks (data center networking) and CoreWeave (AI compute capacity). Conversely, any signs of increased capital discipline could trigger a broader reassessment of expectations across the segment. In this sense, Meta remains one of the key barometers for the AI market.

Muse Spark and the question of monetization scale The early April launch of the Muse Spark model has significantly raised expectations around the company’s technological capabilities. The model was deployed ahead of schedule, reducing investor uncertainty and accelerating the narrative of Meta’s return to the forefront of AI development. However, the key question is less about technological capability and more about the speed of commercialization. So far, Meta has effectively leveraged AI to improve ad targeting and platform efficiency, but the market will be looking for more direct monetization pathways—especially given the scale of ongoing investments.

Macro backdrop and near-term risks Q1 results also reflect a period of heightened geopolitical volatility. The conflict in the Middle East and rising energy prices may have weighed on advertising spend in March, particularly in sectors sensitive to consumer discretionary income. In addition, the broader AI sector is facing increasing scrutiny around valuations and the sustainability of the current investment cycle. Against this backdrop, Meta’s commentary could shape not only its own outlook but also broader sentiment across Big Tech.

Bank of America: Muse Spark as a catalyst for sentiment re-rating Bank of America highlights that the earlier-than-expected rollout of Muse Spark removes a key overhang for the stock. Analysts see potential for iterative improvements in model performance over the coming quarters, which could drive a similar sentiment shift to what was observed with Google following progress in its Gemini models. The bank also points to an attractive valuation relative to AI opportunity and above-industry ad growth, maintaining a positive stance on the stock.

Goldman Sachs: Strong growth, but limited visibility and focus on CAPEX Goldman Sachs remains constructive on Meta’s fundamentals, particularly within advertising, but emphasizes limited near-term visibility due to macroeconomic and geopolitical uncertainty. This increases the importance of forward guidance. The bank is closely watching updates on CAPEX and operating expenses, viewing them as critical to assessing the balance between growth and financial discipline.

JPMorgan: AI-driven advertising as the core growth engine JPMorgan expects Meta’s revenue growth to be largely driven by continued improvements in advertising performance enabled by AI. While investment in AI remains elevated, the bank notes that the company appears to be maintaining financial guardrails. Holding CAPEX guidance steady would likely be interpreted as a positive signal, reinforcing confidence in the investment framework.

Truist: Strongest growth in years and improving monetization Truist forecasts that Meta will deliver its fastest revenue growth since 2021, supported by both user growth and improved monetization through AI integration across advertising and consumer products. Analysts also note that the company is beginning to close the gap with leading players in large language models, while its existing use of AI in recommendation and ad systems is already generating tangible business benefits.

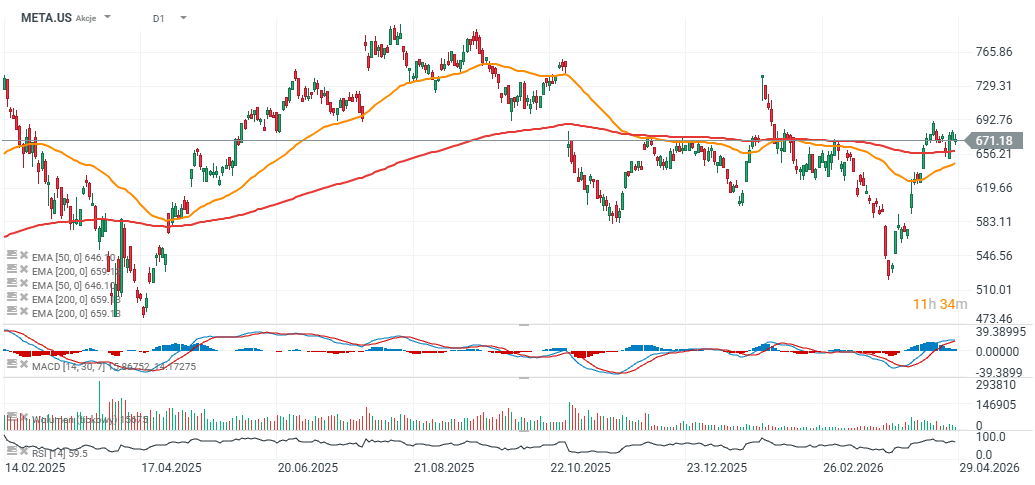

Wedbush: AI “flywheel” and direct CAPEX-to-revenue conversion Wedbush presents one of the more assertive investment theses, pointing to a “flywheel” effect in which AI investments directly enhance ad efficiency and drive revenue growth. In its view, the market continues to underestimate the strength of this relationship. Cost optimization efforts, including workforce reductions, further support Meta’s ability to sustain high levels of investment while driving profitability. Meta Platforms chart (D1 interval) Meta Platforms shares are still trading around 15% below their all-time high near $780, but in recent sessions they have managed to break above the 200-day EMA, signaling strong demand and a potential reversal of the previous downtrend.

Source: xStation5