Key takeaways

- Market hopes for a deal are still alive

- US stocks on best run since 2023

- Growth divergence reflects equity performance

- AI theme roaring ahead as we move into June

- What to watch in the new month

- Key events in the coming week: Global PMIs, US NFPs, SpaceX hype

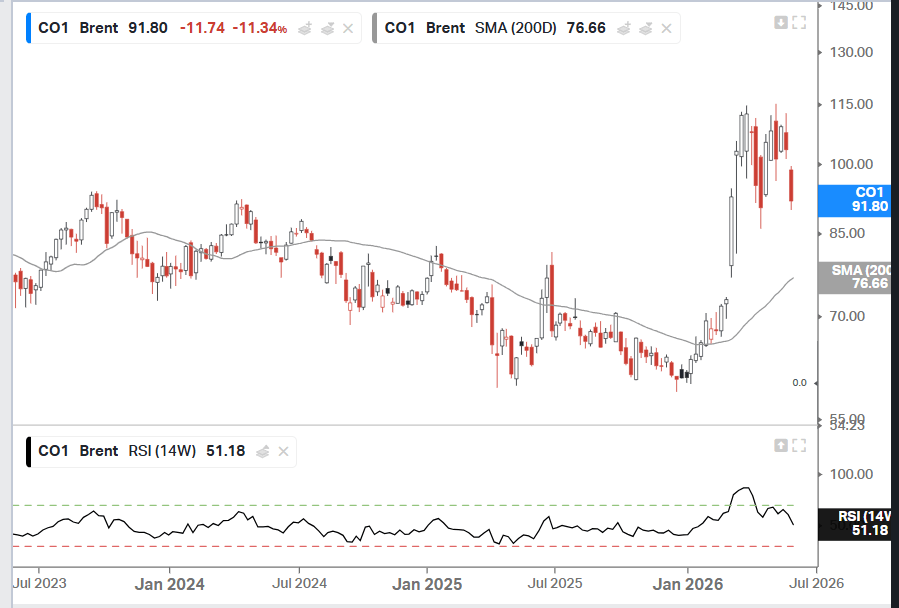

The Week Ahead: Will payrolls justify American exceptionalism? At the start of the new week, the oil price is up by 1.5%, and Brent crude is trading above $93 per barrel. This comes after the US and Iran both exchanged fire over the weekend. Stocks have been slightly impacted by this, European futures point to mild losses later this morning, while US equity futures suggest that further gains are coming, extending last week’s record highs. Even though there have been attacks from both sides, the market is holding onto the fact that negotiations ae ongoing, and an elusive Iran/ US deal to end the war in the Middle East and to reopen the Strait of Hormuz will still be found. As the focus switches to a raft of macro releases later this week, investors will need to watch how this plays out, and any delay in reaching a deal could knock market sentiment.

Market hopes for a deal are still alive

Financial markets are clearly leaning towards a deal getting done, but the crisis has now entered its 4th month. The latest reports suggest that President Trump has demanded changes to the latest Memorandum of Understanding, which could lead to more negotiations over the coming days, meaning that a potential deal may not come until late this week. However, markets seem to have infinite patience when it comes to this conflict ending.

US stocks hitting best run since 2023

Last week was the 9th consecutive week of gains for the S&P 500. It rose by more than 1.4%, which brings its gains for the year so far to a whopping 10%. In May alone the S&P 500 rose 6%, while the Nasdaq jumped 9%, as the tech sector leads US markets higher. The US tech sector rose by 5% last week, and by 20% in May, as the AI theme reinforces its dominance in global markets. This is the longest winning streak for US equities since December 2023 and comes amidst the backdrop of the Middle East war. May threw multiple challenges at investors including geopolitical developments, volatility in the energy markets, political risks, divergent economic data and strong corporate earnings. The latter factors help to explain the outperformance of US stocks. In contrast, European indices underperformed their US peers last month. The FTSE 100 rose by 1.9% last month, and the French Cac rose 1.3%.

Growth divergence reflects equity performance

The equity performance reflects multiple factors, including the decline in the oil price, which dropped 16% in May for Brent crude, its worst monthly performance for over a year. This is hindering the FTSE 100, which is heavy on oil majors and other commodity-linked stocks. In Europe, the growth outlook is hurting equity performance. France is sliding towards recession, and the ECB could be on the cusp of raising interest rates, which is one reason why the stock market gains are not able to keep pace with the US. Although US Q1 GDP was revised down from 1.6% from 2%, this is still enviable compared to Europe, where GDP was 0.6% in the UK, 0.3% in Germany and -0.% in France for the first quarter. Interestingly, the Asian indices are proving to be extremely resilient to geopolitical risks. For example, the Japanese Nikkei rose by 10% last month, and South Korea’s Kospi jumped nearly 30%. This is partly linked to strong growth, Japan’s economy grew by 0.5% last quarter, but South Korea had a strong 1.7% growth rate, its fastest rate of growth for 6 years, as it benefits from strong exports of semiconductors and other AI-related exports, which is firing up interest in its stock market.

AI theme roaring ahead as we move into June

For now, there is no reason to think that the AI theme will fade as we move into the final month of Q2. Thus, we may continue to see outperformance of US and some Asian stocks as we start a new month. As we move into June, earnings momentum and a falling oil price are boosting stocks and sustaining a bond market rally, led by the UK. However, as we move into the middle of 2026, there are a few themes to watch that could have a major impact on risk sentiment.

1, Earnings revisions

So far, earnings revisions are going in a positive direction. In April and May, analysts increased their EPS estimates for Q2, by 2.5% for the S&P 500. The average earnings revision in the last 5 years is -1.6%, which suggests that analysts are expecting another monster earnings season from the US. Energy and tech are leading the upward revisions, as the oil price remains robust, and analysts are predicting that the AI theme still has legs. Positive earnings revisions are a powerful driver of stocks, and this could protect the bulls as we move into June.

2, Geopolitics

Betting markets are still predicting a strong likelihood of the Strait of Hormuz reopening by the end of this month. While this could get oil and other commodities flowing around the globe once more, it might not be a one-and-done opening of the Strait. There is the potential that Iran uses the Strait as leverage down the line, and this cannot be disregarded. Due to this, after a 16% drop in the oil price last month, there may not be much room for further declines, even if we get a deal in the coming days. The Brent crude oil price may struggle to fall much below $90 per barrel on the back of a deal getting agreed, which could embed inflation into global supply chains for the long term. The UK is also worth watching this month. UK 10-year yields fell 24bps last month, and the bond market is banking on a change of leadership of the Labour party will not impact the current fiscal rules. Thus, even if Andy Burnham wins this month’s by-election in Makerfield, the market may not price in a fiscal collapse of the UK. Burnham has been tamed by the bond market, and he may not even win the by-election. If he does, there is still the potential for a new general election if he shifts dramatically from Starmer’s manifesto. Thus, the market is willing to ignore UK’s politics for now, but that could change as we move closer to the election date.

3, Central banks

Just because there is a deal expected to be reached between the US and Iran, don’t expect the world’s major central banks to shift to an immediate dovish stance. We do not think that this is likely for a few reasons. Looking at the US first, growth in the US remains robust, inflation is also elevated. Although the core PCE was slightly weaker than expected last month, there has still been 62 months of PCE data that is above the Fed’s target rate in the US, which makes it hard for new Fed chair Kevin Warsh to advocate for rate cuts. Warsh said that he prefers trimmed mean PCE data, however, this is known to underestimate subtle shifts in inflation dynamics, such as the change in the price of goods. Warsh may need to tread carefully, lest he jeopardize the Fed’s credibility on inflation fighting. The outlook for the Fed will be critical for the dollar this month.

The USD index has eked out a 0.9% gain in the past month, as its upward momentum has been derailed by hopes that the war in Iran will come to an end. This has given EM FX a welcome breather, for example, the South African rand is up more than 3.5% vs the USD in the past month. Strengthening EM FX could make their stocks more attractive in the coming weeks, and we may see a broadening of the stock market rally. The question of inflation fighting credibility is also a concern for other central banks including the ECB and the BOE.

The ECB is expected to hike rates twice this year, although the growth outlook, especially for France, could dim the prospect of a second hike in September, especially if the Strait of Hormuz does reopen. For the UK, the interest rate futures market has scaled back its expectations for rate hikes from the BOE in recent weeks. There is now 1 hike expected, which could be a stretch, even if the BOE signals that it remains watchful about second round inflation effects from the energy price spike. Ahead this week, the focus is likely to be on macro data, with the set piece coming on Friday with the release of the May labour market report for the US. Below, we highlight some key events to watch.

1, US data:

There will be plenty of economic data for traders to get their teeth into this week, including the ISM surveys for the US and global PMI surveys. The focus will be on the economic lead indicators and what the PMI surveys tell us about the strength of the private sector, which has moderated sharply in recent months. This data could reinforce the economic exceptionalism of the US. However, it may also tell us some potential pitfalls for the months ahead, especially if we see any sign that a slowing global economy is weighing on the US outlook. The ISM manufacturing prices paid component, which will be released on Monday, is also worth watching, as it could tell us if oil-driven inflation is permeating deeper into the pipeline.

2, NFPs:

The market will be looking for another NFP beat for last month, after a strong run of US payrolls growth. The market is expecting a reading of 96k, and for the unemployment rate to remain steady at 4.3%. Average earnings are expected to moderate slightly to 3.5% from 3.6%, but an upward surprise could be problematic for the Fed, as it may suggest second round inflation effects from the energy price spike. Overall, while payrolls is in focus this week, a breakdown in negotiations between the US and Iran could shift the narrative on the global economic outlook before we even get to NFPs.

3, IPO bonanza

The number of trillion-dollar companies listed predominantly in the US is set to surge in the coming weeks and months with some major IPOs lined up. Elon Musk’s SpaceX is expected to list in the US on 12th June, and it could value the company at $1-$2 trillion. This week we expect the build up to the IPO to gather pace. The SpaceX IPO is notable because of its large allocation to the retail market, thus a traditional roadshow may not yield the excitement some may expect. Instead, it’s worth gauging the online reaction to see how fired up the retail community are in the lead up to this IPO. The outcome of SpaceX’s IPO could determine enthusiasm for OpenAI’s listing, which is expected to take place in Q3/ Q4 this year.

Chart 1: S&P 500 monthly chart

Source: XTB Chart 2: Brent crude oil price

Source: XTB and Koyfin