What’s Next for the European Luxury Market❓

Thursday’s trading session in Europe is going relatively well—Euro Stoxx 50 futures are up 0.31% to 5,902 points, the DAX is up 0.46% to 24,355 points, and the S&P 500 closed yesterday at a new all-time high (+0.8%), and the Nasdaq 100 gained 1.4%. This movement is driven by a combination of three factors: news of a possible extension of the U.S.-Iran truce and the resumption of negotiations, strong Chinese GDP beating forecasts, and excellent results from the trading desks of Wall Street’s largest banks.

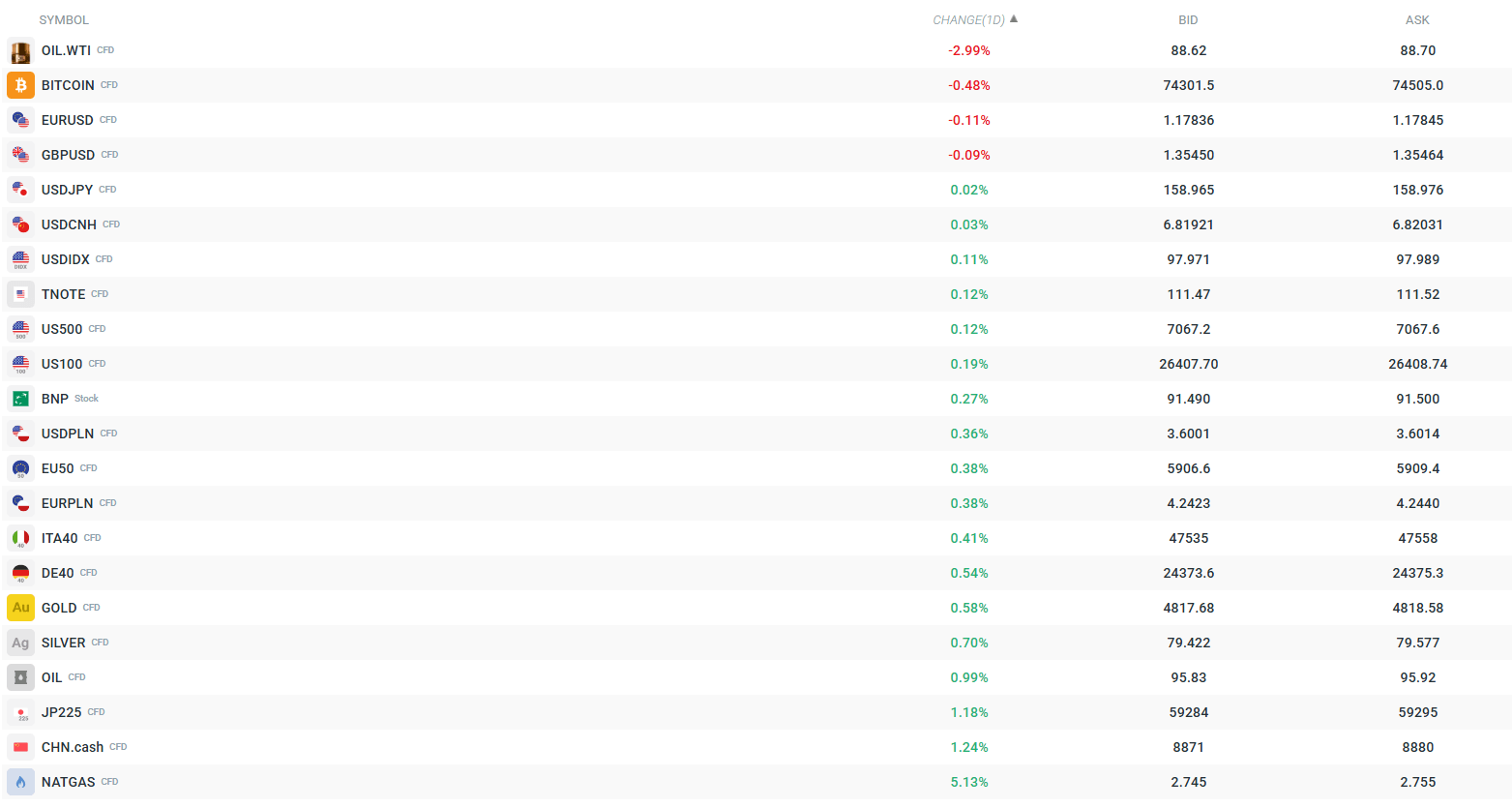

The picture on the commodities markets is mixed. WTI is down -3.00% today to $88.61/bbl due to futures contract rollover (similarly, the volatility spike caused by rollover is affecting NATGAS prices!). Brent is behaving differently and is up 0.94% to $95.78. Precious metals are rising steadily: gold +0.53% to $4,815/oz, silver +0.77% to $79.47/oz — the market continues to price in an inflationary geopolitical premium.

However, macroeconomic data complicate the picture on the inflation front. Eurostat revised eurozone inflation for March to 2.6% from 2.5% — this marks the first time this year that inflation has exceeded the ECB’s target, and the upward revision was preceded by similar moves from France, Italy, and Spain. Core inflation stands at 2.3%, while services inflation is at 3.2%. The ECB is likely to hold off on a decision at its April 29–30 meeting, although the market is pricing in two 25-basis-point hikes by the end of the year. The foreign exchange market is calm. EURUSD is down 0.09% to 1.1785, GBPUSD is down 0.09% to 1.3546, and USDJPY is virtually unchanged (+0.01%) at 158.95. The USDIDX dollar index is rising slightly by 0.11% to 97.97 — still below the psychological barrier of 100 points. Bitcoin is down 0.53% to $74,260.

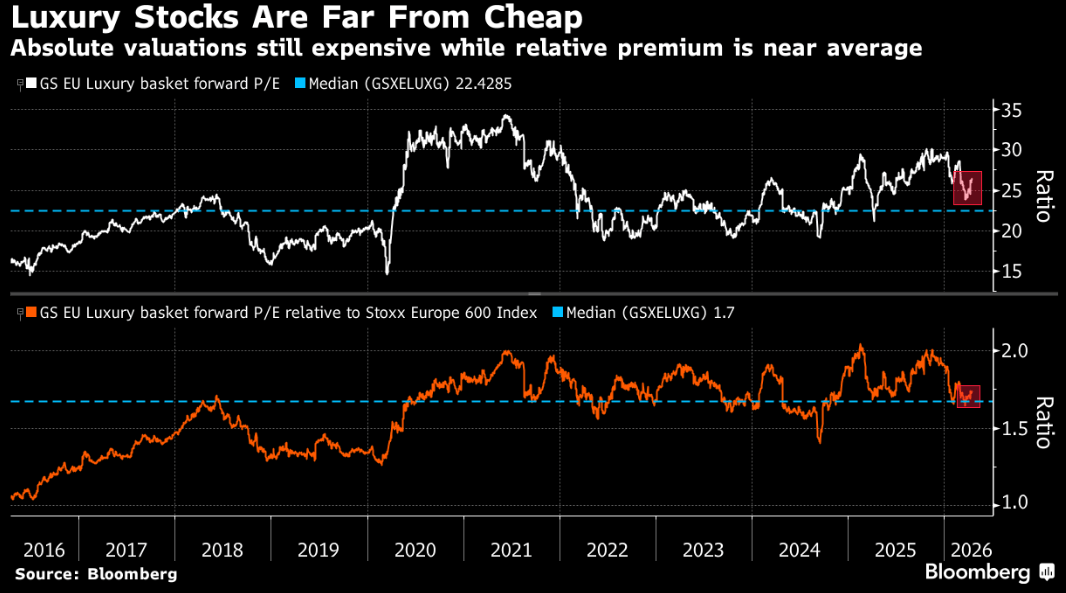

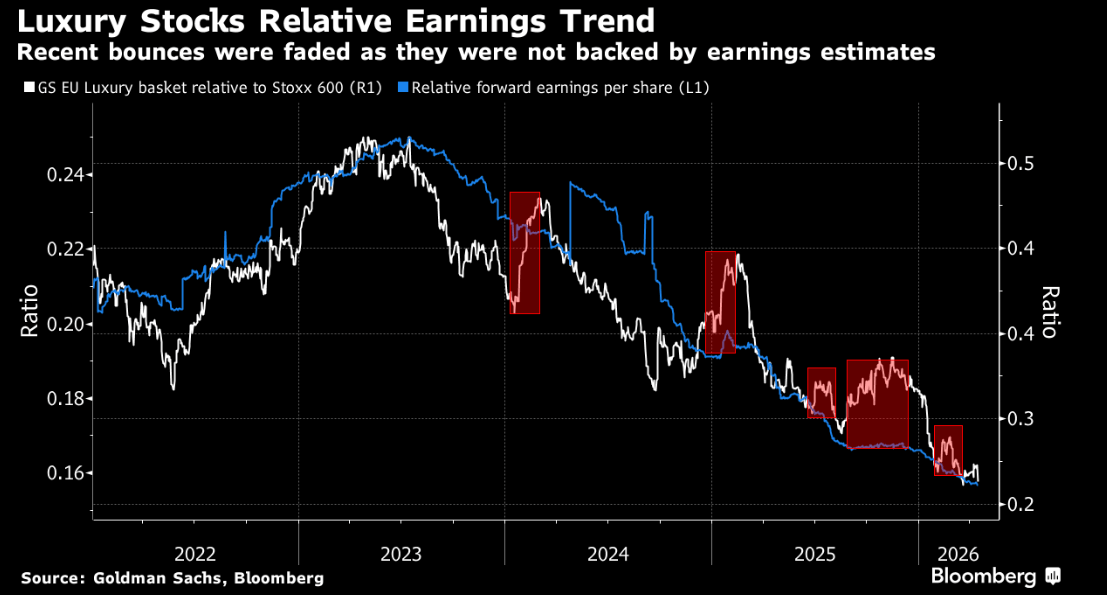

Current volatility in key markets. Source: xStation Goldman Sachs’ luxury stock index has fallen 13% year-to-date , while the Stoxx 600 has risen 4.2%. Three reports this week—LVMH (decline in fashion and leather goods sales), Hermès (decline in the Middle East, weaker tourist traffic in France), and Kering (Gucci -8%)—dashed hopes for a quick rebound. Barclays analysts wrote: “Earnings momentum has stalled and provides no fundamental support for prices.” Goldman Sachs notes that every sector rebound over the past few years that was not backed by upward earnings revisions has fizzled out—and today history seems to be repeating itself.

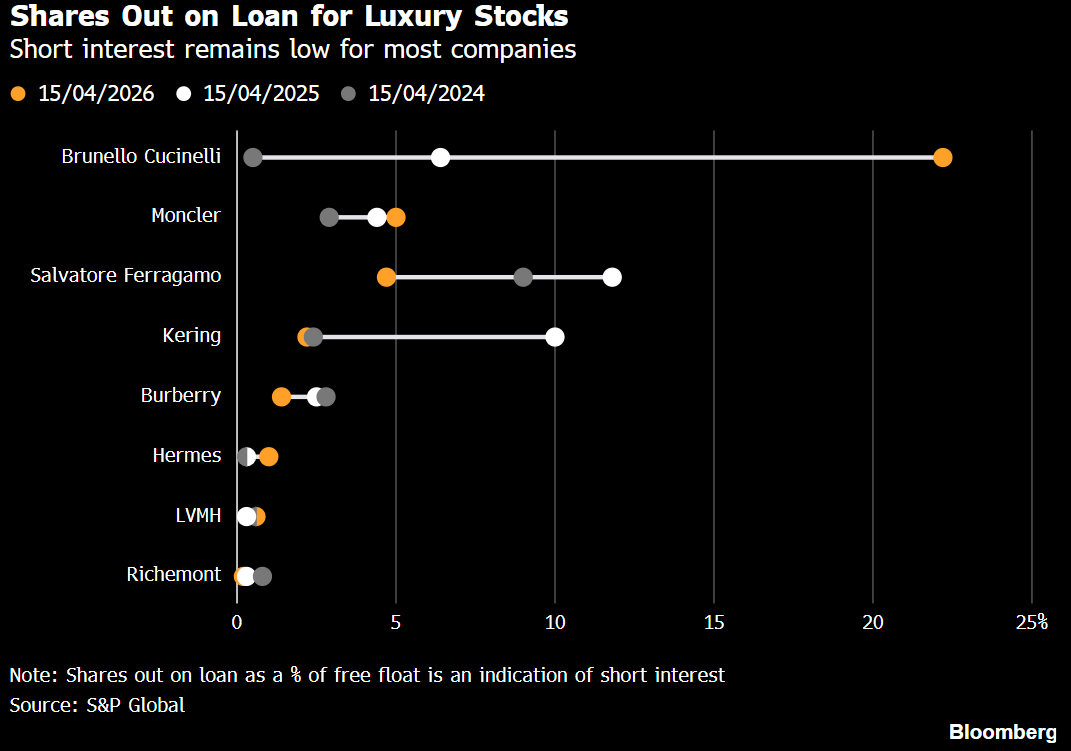

The sector’s premium over the broader market has shrunk to 75% (from ~100% on several occasions in recent years), but with the prospect of further downward revisions to EPS, it still does not look “cheap.” Short selling is returning for now only to Brunello Cucinelli (short interest has exploded to about 22% of the free float from 4% a year ago).

Looking at the sector’s historical average valuation, current figures are consolidating around the mid-range. Source: Bloomberg Financial Lp

On the other hand, earnings forecasts for companies in this sector are being continuously revised downward. Source: Bloomberg Financial Lp

However, for most companies, we don’t see much interest in short positions, with the exception of Brunello Cucinelli. Source: Bloomberg Financial Lp

Company News EasyJet — down 8.7%, the biggest drop since 2022 EasyJet has warned that it will incur a pre-tax loss of between £540 million and £560 million in the first half of the current fiscal year, with the conflict in the Middle East alone adding £25 million to fuel costs in March. Bookings for the third and fourth quarters are lower than a year ago, and CEO Kenton Jarvis acknowledged that summer bookings are currently slightly below last year’s levels. The company’s shares plunged by as much as 8.7%, marking their largest one-day drop since June 2022.

Kering — down 4.6%, cautious outlook Kering fell as much as 4.6% today following its Capital Markets Day, during which management presented the “ReconKering” strategy, which aims to double the operating margin from FY25 levels in the medium term and achieve a return on capital of over 20%. Analysts reacted to the targets with caution: AlphaValue/Baader assesses them as a “cautious stance reflecting the uncertain geopolitical and consumer environment, particularly with regard to Gucci and China,” while Oddo BHF states outright that the financial ambitions presented do not constitute “any groundbreaking revelation.” The company has set three clear milestones: completing structural restructuring and restoring financial discipline by the end of 2026, entering a phase of sustainable growth by the end of 2028, and regaining its leadership position in the “Next Luxury” segment by 2030.

Pernod Ricard — -2%, disruptions caused by the war in the Middle East Pernod Ricard expects that disruptions caused by the war in the Middle East will contribute to a decline in annual sales of up to 4%, while the company continues to grapple with weak demand in its key US and Chinese markets. The group’s direct exposure to the Middle East accounts for only about 2% of revenue, but the real issue is the traffic restrictions at Dubai International Airport, through which 5% of the group’s duty-free sales pass. In the quarter ending in March, the first signs of improvement emerged, with organic net revenue rising by 0.1%, beating analysts’ expectations of a decline of over 1%.

Tesco — +2.7%, strong annual results Tesco surprised the market positively by reporting an adjusted annual operating profit of £3.15 billion, up 0.8% year-over-year and above the consensus estimate of £3.11 billion, with revenue reaching £72.46 billion. However, the company issued a wider-than-usual guidance range for the next fiscal year, with the midpoint falling short of market expectations due to increased uncertainty related to the conflict in the Middle East.