PayPal – Sale, Stagnation, or Revolution?

PayPal shares jumped by nearly 20% during Wednesday’s session, breaking above the $55 level. This move followed reports about a joint acquisition offer submitted by Stripe and the private equity fund Advent International. The consortium reportedly proposed $60.50 per share, valuing the company at over $53 billion. These figures matter because they represent a premium of more than 25% versus the market valuation at the time the offer was made. The rise in valuations shows that investors treated the bid seriously, although the share price still remains below the funds’ offer. If acquired, Stripe would gain access to PayPal’s more than 430 million consumer accounts, the Venmo network, and a range of other assets. In practice, this would complement Stripe’s offering with a large retail and consumer market. The combined group would process around $3.7 trillion in payments annually.

Is PayPal cheap?

Among analysts focused on value stocks, PayPal is known for having a valuation that for many years has not reflected the company’s fundamentals. The company has long ceased to be a “growth” company, but it remains in a very solid position. In the first quarter, it increased revenue by 7% to $8.35 billion, and total payment volume reached $464 billion. Over the last 12 months, PayPal generated about $6.8 billion in free cash flow. However, the offer does not mean the company’s operational problems have disappeared. Operating margin shrank to 18.4%.

Management forecasts that in the second quarter adjusted EPS will fall by around 9%, and dollar transaction margin will decline by about 3%. Pressure is also rising from Apple Pay, Google Pay, and banking solutions. The new CEO, Enrique Lores, is trying to reverse this trend through an ongoing reorganization of the company. The plan calls for at least $1.5 billion in savings over a three year horizon, although a significant portion of the funds is expected to be reinvested into product development. The biggest test remains accelerating “branded checkout” and monetizing Venmo more effectively.

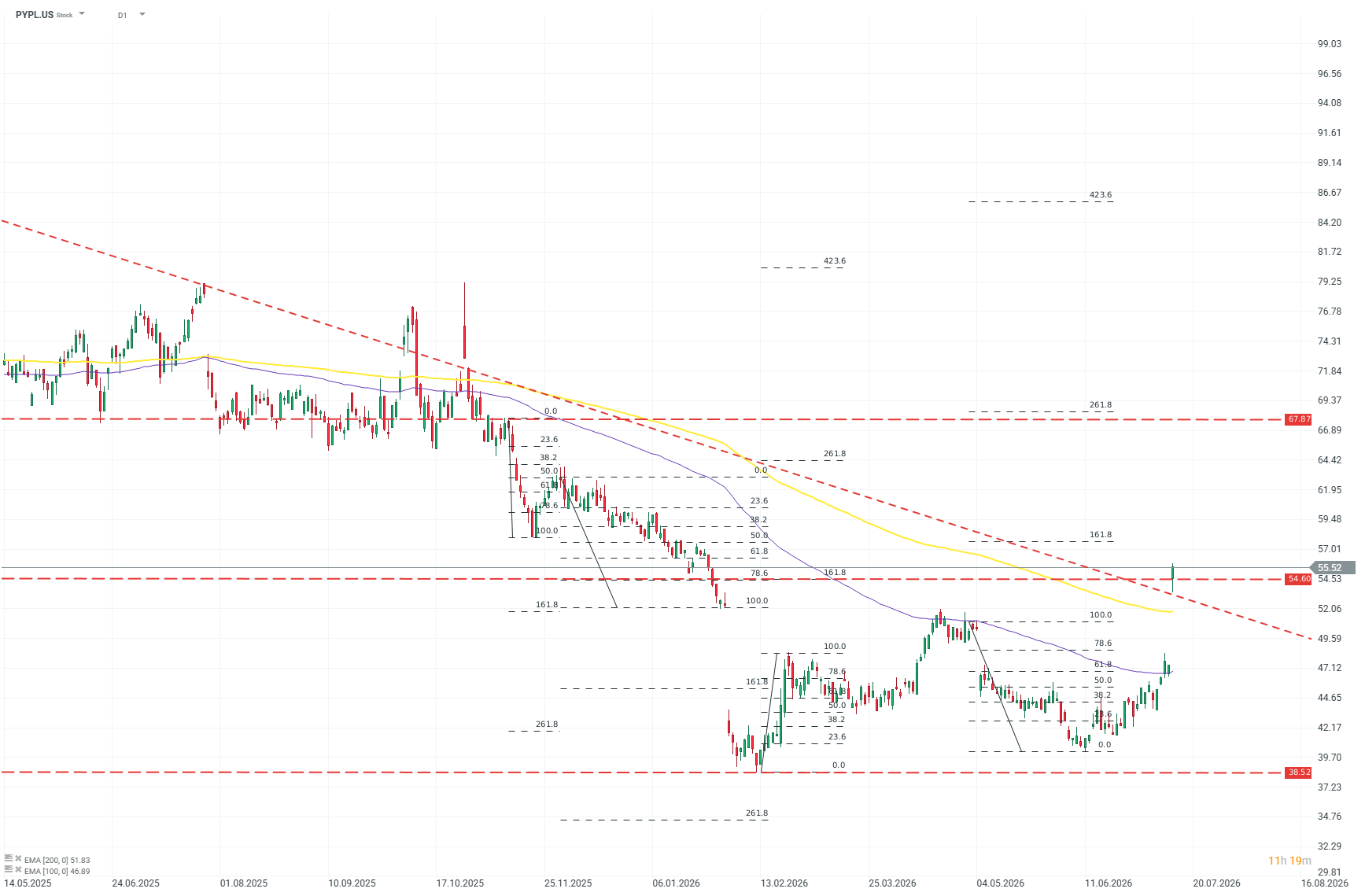

PayPal technical analysis (D1)

Although the company is still far from its peak, the recent rally is a strong bullish signal. In a single move it broke through the long term downtrend line and cleared resistance around 54. Source: xStation5

After many years of a persistent downtrend, PayPal is suddenly back in the spotlight, prompting questions about the company’s outlook. Everything depends on whether PayPal decides to accept the acquisition offer. The most interesting twist would be rejecting the proposal. That would be a clear signal of strength and of shareholders’ and management’s confidence in their strategy.