ASML – JPMorgan revises its forecasts for the European star of the capital markets

ASML (ASML.NL) is one of the most unique companies on the stock market—the Dutch manufacturer of lithography machines is the world’s sole supplier of EUV (extreme ultraviolet) systems , without which modern chip production is impossible. The company has been growing steadily for years, driven by the boom in AI, data centers, and next-generation semiconductors. In 2025, ASML reported €32.7 billion in revenue , and for 2026, management provided guidance of €36–40 billion —a growth rate that means every analyst on Wall Street and in Europe must keep a close eye on this company.

JPMorgan: Consensus “Far Behind” The latest market signal is very telling. JPMorgan analyst Sandeep Deshpande raised the price target to €1,900 (from €1,515), thereby matching UBS’s record Street high. More importantly, it’s not just about the price, but about a major revision of financial models. JPMorgan sees ASML delivering 90/105 EUV systems in 2027/28, which translates to EUV revenue ~10%/~20% higher than the current consensus. Immersion DUV revenue in 2027 is expected to be 35% above Street estimates . Overall, JPMorgan forecasts 2027/28 sales to be 16.7%/21.8% above consensus and EPS of 31.7%/35.4% above – this is not a marginal deviation, it is a fundamental breakthrough.

Forward P/E Ratio – Not So Cheap Anymore

And here we come to the crux of the matter, as illustrated by the chart from the Bloomberg Terminal (P/E Estimate Relative). The current BEst P/E is 41.48x – and this is clearly in the upper range of the historical range over the last 5 years. The histogram on the right shows that the current level of ~41x is in the upper quartile of the distribution – fewer than 5–6% of historical observations were higher. Looking at forward projections, the data shows a 2026 forward P/E ratio of ~43x for 2026 and ~32.6x for 2027. This means that the company is already “priced in” for a very optimistic scenario—and that is precisely why, even given JPMorgan’s bullish stance, it is worth watching to see whether EUV order fulfillment will actually exceed the consensus. Key Conclusion ASML is structurally one of the strongest businesses on the stock market. Record Q4 2025 bookings ( €13.2 billion, double expectations ), a monopoly on EUV, and the management’s clearly positive tone regarding demand—all of this is bullish. But P/E analysis reminds us that a good company and a good investment are not always the same thing – at 41x forward earnings, the market has already priced in a great deal of good news. If JPMorgan is right and the consensus is indeed too low, there is room for further gains. However, if actual results fall even slightly short of expectations – the correction could be just as sharp as the gains.

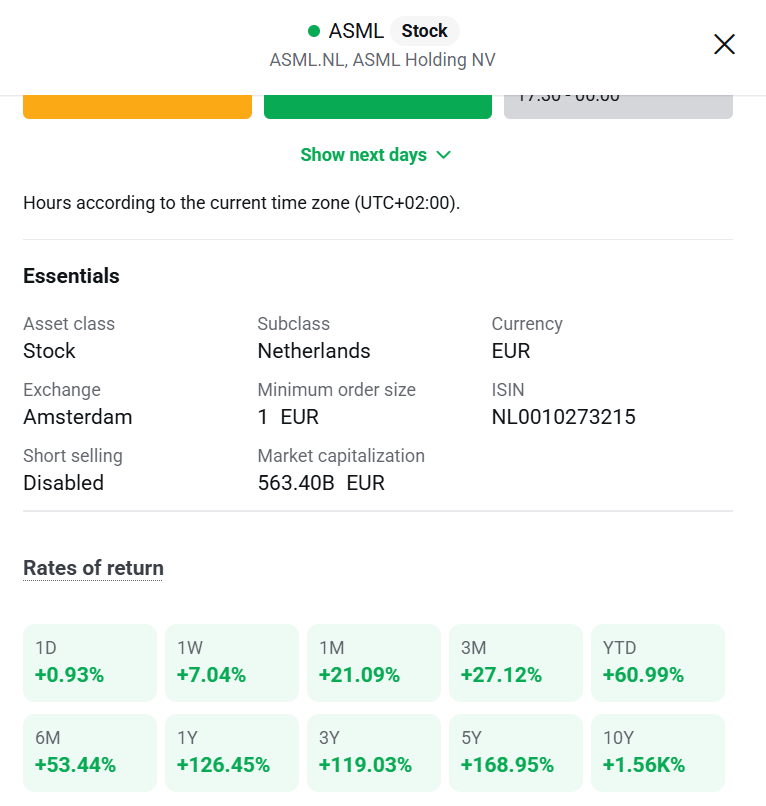

Since the beginning of the year, ASML shares have risen by nearly 61%. Source: xStation