European stocks on the rise. ASML powers chip stocks while defense sector pulls back

European equity markets are posting strong gains, with both the STOXX Europe 600 and Euro Stoxx 50 climbing to fresh record highs. Investor sentiment has improved on expectations that the Federal Reserve may delay further rate hikes following weaker-than-expected U.S. labor market data. The rally is no longer driven solely by technology, as industrials, financials, and defense stocks are also attracting buyers. Germany’s DAX continues to lead the region, reaching another all-time high. With U.S. markets closed today for Independence Day, investors are focusing primarily on developments across Europe. Meanwhile, Brent crude is trading near $72 per barrel, while EUR/USD has eased to around 1.144 following the latest European PMI releases.

Key takeaways

- The STOXX Europe 600 is up 0.5% in morning trading, remaining close to record highs.

- Germany’s DAX gains nearly 0.9% , setting another all-time high, supported in part by Siemens after a broker upgrade.

- The FTSE 100 adds 0.3% , while France’s CAC 40 also rises 0.3% , highlighting broad-based strength across European markets.

- Aalberts climbs 4.3% and A.P. Moller-Maersk B gains 3.5% , while EQT falls 1.9% and Redcare Pharmacy declines 1.7% .

- Defense stocks continue to outperform amid ongoing geopolitical tensions and expectations of higher military spending.

- The market rotation has broadened to include cyclical sectors, industrials, and financials, while Pluxee jumps around 6% following its quarterly earnings release.

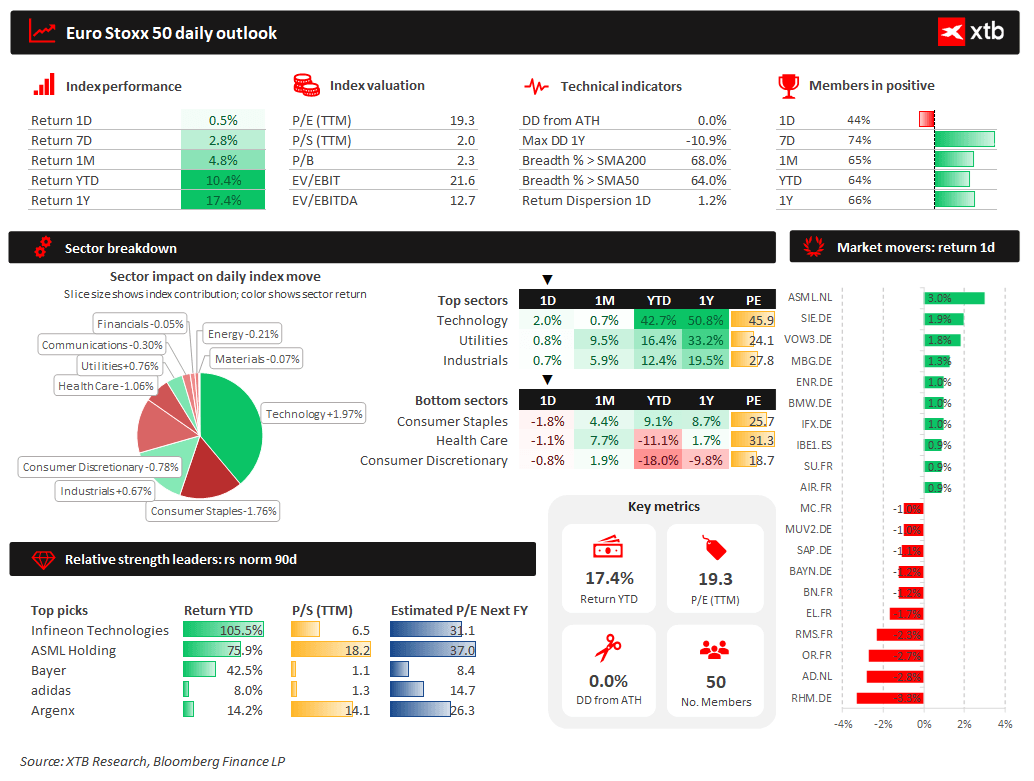

Euro Stoxx 50 daily outlook

The Euro Stoxx 50 remains at record highs, advancing 17.4% over the past twelve months and more than 10% year-to-date . Technology is the largest contributor to today’s gains, while defensive sectors such as consumer staples and healthcare continue to lag. Around 68% of index constituents are trading above their 200-day moving averages, confirming broad market participation in the ongoing uptrend. Infineon Technologies and ASML remain among the strongest relative performers, suggesting that Europe’s semiconductor sector continues to be one of the key drivers of the region’s bull market.

Source: XTB Research

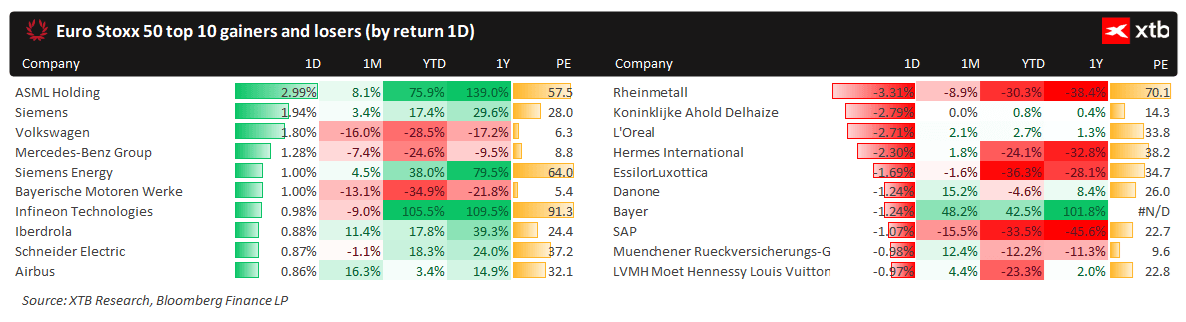

Market movers Today’s session has been dominated by technology and industrial stocks, with ASML leading the gains after rising nearly 3% , reinforcing the strength of Europe’s semiconductor sector. Other notable outperformers include Siemens , Volkswagen , and Mercedes-Benz , pointing to improving sentiment toward cyclical companies. On the downside, Rheinmetall is the weakest performer as investors take profits following its recent strong rally, while L’Oréal , Hermès , and Ahold Delhaize also trade lower. On a one-year basis, Infineon , ASML , and Siemens Energy remain among the strongest performers in the index, whereas luxury goods companies and parts of the automotive sector continue to underperform.

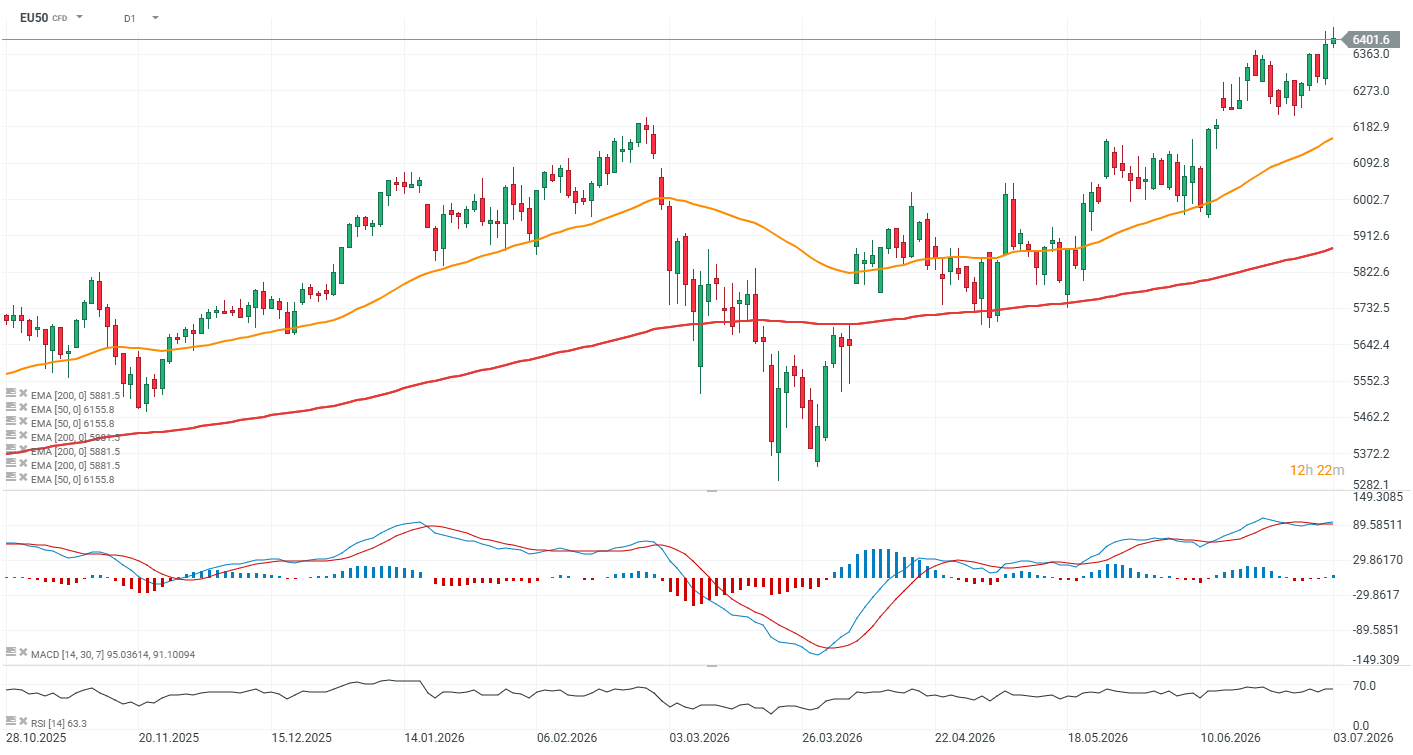

Source: XTB Research EU50 (D1)

The Euro Stoxx 50 futures contract has climbed to fresh all-time highs above 6,400 points , extending its strong bullish trend. European equities have proven more resilient than their U.S. and Asian counterparts amid recent volatility in semiconductor and memory-chip stocks, while technology shares are staging a recovery during today’s session.

Source: xStation5

Eurozone economy stabilizes after two months of contraction

The Eurozone’s Composite PMI rose to 50.0 from 48.5 in May, marking its highest reading in three months and the first return to expansion territory since March. Services remain in contraction at 49.4 , although the pace of decline has slowed considerably, while manufacturing improved enough to offset weakness in services. One of the most important developments was a sharp slowdown in cost inflation, with service-sector input cost inflation recording its largest decline since the survey began in 1998 (excluding the COVID lockdown period), largely reflecting easing energy price pressures following the Middle East conflict. Employment stabilized after May’s sharp decline, while business expectations improved to their strongest level since the conflict began. Overall, the data reduce the likelihood of additional ECB rate hikes in the near term.

Country breakdown Germany

- Services PMI: 48.6 (vs. 46.8 expected; 46.8 previous)

- Composite PMI: 49.5 (vs. 48.0 expected; 48.0 previous)

- Services remained in contraction for a third consecutive month, although at the slowest pace since April. Cost pressures eased significantly despite still-soft demand, particularly from abroad.

France

- Services PMI: 46.8 (vs. 47.4 expected; 47.4 previous)

- Composite PMI: 47.2 (vs. 47.6 expected; 47.6 previous)

- Business activity contracted at the slowest pace since March following an exceptionally weak May. Business confidence improved modestly, while cost pressures weakened for the first time since October.

Italy

- Services PMI: 50.2 (in line with expectations; previous 49.4)

- Composite PMI: 50.8 (vs. 50.9 expected; previous 50.4)

- Economic activity returned to growth after three months of contraction, supported by stronger domestic demand. Cost and price inflation continued to ease, while business confidence reached its highest level since November.

Spain

- Services PMI: 54.2 (vs. 50.9 expected; previous 50.1)

- Composite PMI: 53.3 (vs. 50.9 expected; previous 50.2)

- Spain recorded the strongest growth in business activity and new orders this year, with employment rising at its fastest pace since March and output price inflation falling to its lowest level since January.

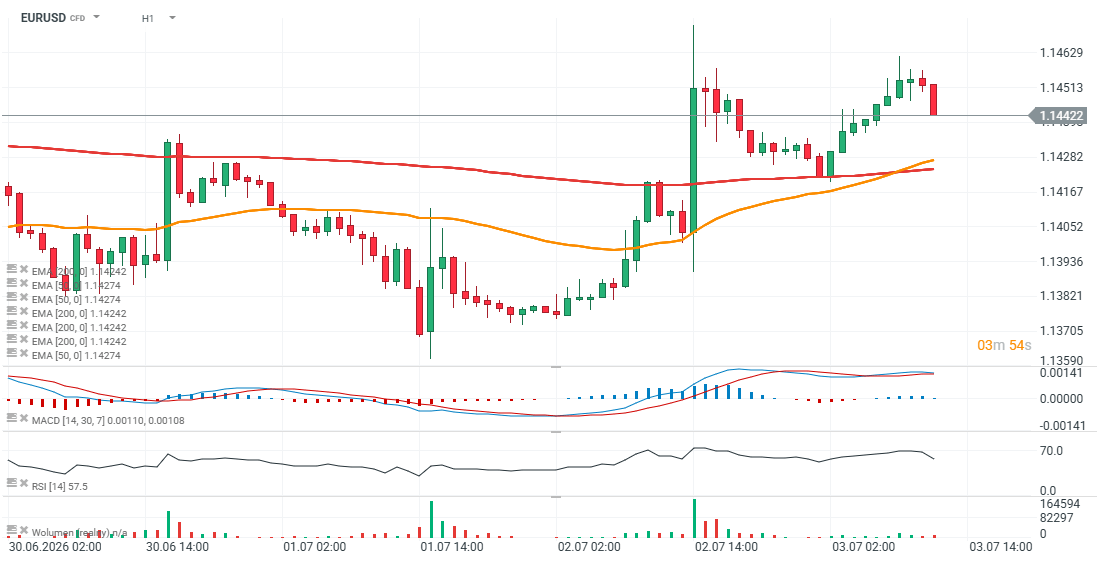

EUR/USD (D1) The EUR/USD pair has slipped to around 1.144 despite relatively solid Eurozone PMI data. Markets appear to be interpreting the latest figures as supportive of a prolonged ECB pause, while lower oil prices continue to reduce inflation risks across the Eurozone.

Source: xStation5