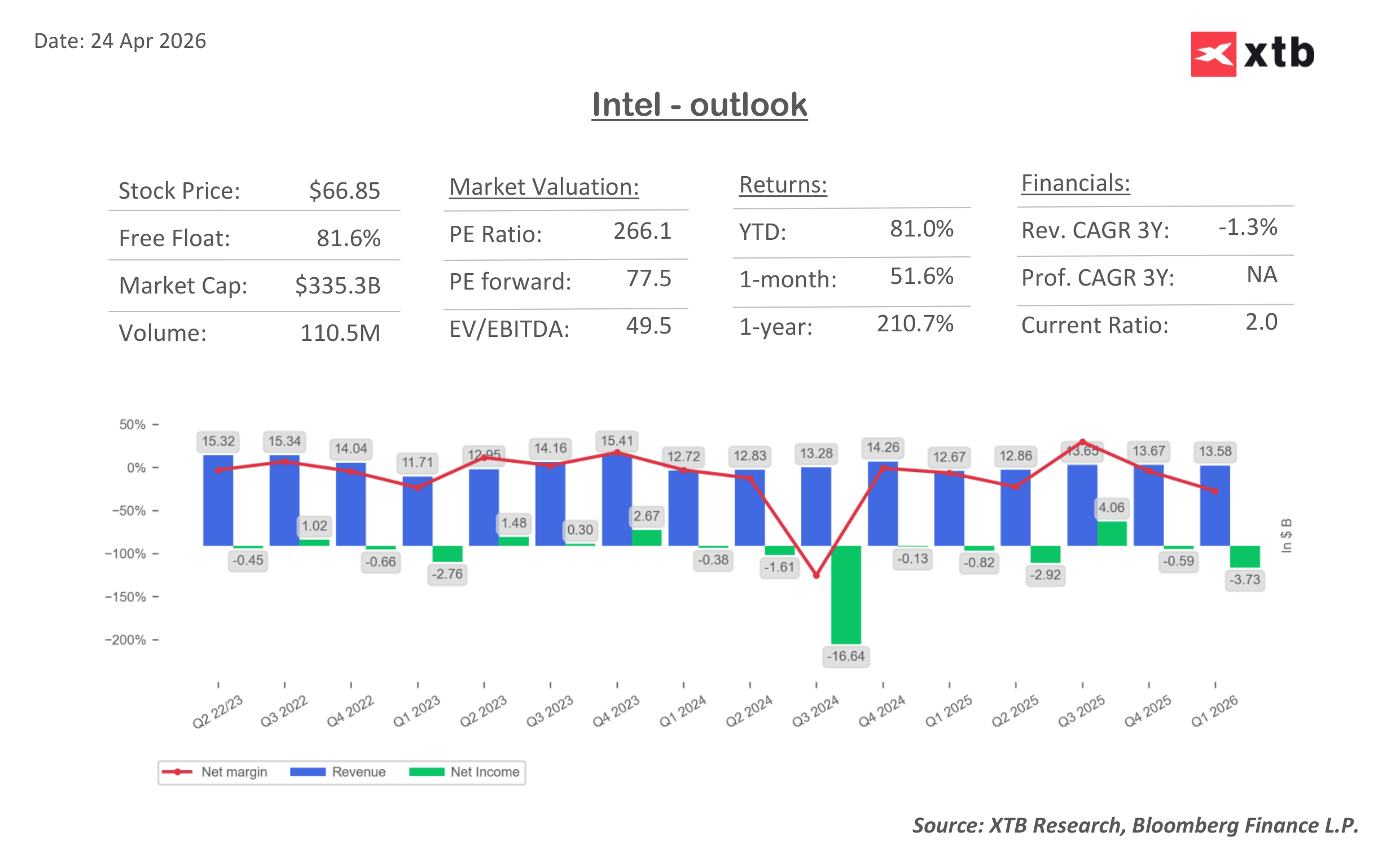

Intel: AI drives results, and CPUs may be the next stage of the revolution

Intel’s results for the first quarter of 2026 clearly reinforce the view that the company is beginning to emerge from a multi-year period of operational weakness. The report itself delivered a solid beat versus expectations, but even more important are the forecasts for the coming months, which give the release a distinctly more growth-oriented tone and acted as a catalyst for a strong market reaction.

Key financial highlights for Q1

- Revenue $13.58 billion, 7.2% YoY, above consensus

- Adjusted EPS $0.29 vs expectations around $0.01

- Gross margin 41% vs 34.5% forecast

- Data Center & AI $5.05 billion, 22% YoY

- Foundry $5.42 billion, 16% YoY

- Operating income $1.67 billion vs $0.69 billion a year earlier

The scale of the positive surprise is visible not only in revenue, but above all in profitability. The increase in gross margin to 41% suggests improvements in both the sales mix and cost efficiency. This indicates that actions taken in recent quarters are starting to translate into tangible financial results. The Data Center & AI segment remains the primary growth driver, posting 22% YoY. This confirms that artificial intelligence is already generating real and growing demand, particularly in server infrastructure. Increasing importance of inference and edge-related applications is reinforcing the role of CPUs within the broader ecosystem.

The first phase of the AI boom was largely driven by GPUs, where NVIDIA established a dominant position. However, there are growing indications that the next phase could shift the center of gravity toward CPUs, especially in the context of scaling and broader adoption of AI applications. The foundry segment is expanding at 16% YoY and is gradually becoming a more meaningful part of the business mix. Improved capacity availability suggests that previous supply constraints are easing, supporting both shipment volumes and pricing.

Guidance remains the key focus for the market. For the second quarter, the company expects revenue in the range of $13.8 billion to $14.8 billion and EPS of $0.20, clearly above prior expectations. In addition, projected gross margin of around 39% points to continued improvement in profitability. On a broader view, the company signals sustained strong demand and the potential for above-seasonal growth in the coming quarters of 2026, supported by AI expansion and improved supply conditions. This suggests that the momentum seen at the start of the year could continue into the second half.

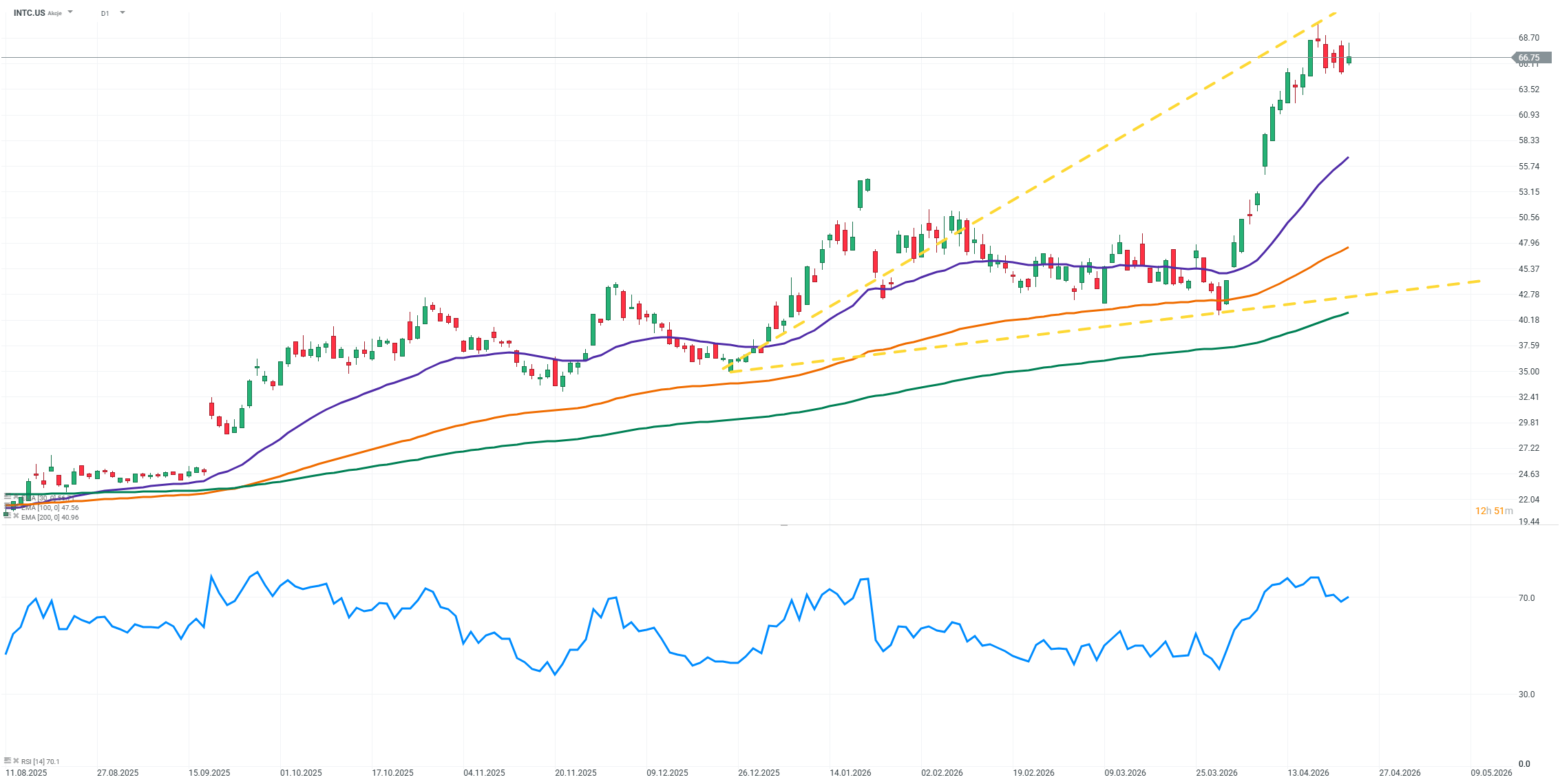

The market reaction was very strong, with the stock rising more than 20% in premarket trading, also lifting other companies in the semiconductor sector. It is worth noting that Intel shares have already gained more than 70% year-to-date. Despite the clear improvement, challenges remain. Pressure from high capital expenditures is still evident in cash flow levels, highlighting that the transformation process continues to require time and consistent execution.

Overall, the reported results and outlook point to an increasingly credible improvement in the company’s fundamentals. Support from rising AI-driven demand, better capacity availability, and improving operational efficiency creates a solid foundation for further performance gains in the coming quarters. At the same time, higher market expectations mean that sustaining this trend will be critical for future stock performance.

Source: xStation5