Is SpaceX a bubble? Investors have already priced in the great future

Elon Musk’s space business continues to dominate financial headlines, and for good reason. SpaceX, which went public on Friday, June 12, is now worth more than $2.6 trillion, surpassing the market capitalization of Amazon’s publicly traded empire—a company that generated $77.7 billion in net income in 2025. By contrast, SpaceX reported a net accounting loss of more than $4 billion in 2025, while earning less than $1 billion in 2024. So is this a bubble? Or is it simply the unique valuation profile of a dominant company operating in a strategic, future-oriented industry? The two explanations are not necessarily mutually exclusive.

Valuation Is Always an Abstraction Fundamental analysis textbooks provide useful guidelines, but they do not represent an absolute set of mathematical rules governing how investors should value companies. Every investor knows the importance of having a framework and sticking to it. Yet the market repeatedly demonstrates that large groups of investors are willing to value companies in ways that diverge significantly from conventional methods. Those investors are currently willing to buy SpaceX shares at valuation multiples equivalent to 150 or even 200 times sales. Are there arguments that can justify such optimism? Let’s take a closer look. SpaceX currently possesses technology that allows rockets to be reused multiple times. This dramatically reduces launch costs and lowers the barriers to expanding beyond Earth. At this point, it hardly needs to be explained why Elon Musk’s space business is unique.

High barriers to entry, a lack of credible competitors capable of threatening its position, and the strategic importance of space as the “ocean” surrounding our planet all contribute to the investment case. There is also the long, risky, and capital-intensive journey required for any challenger to compete in this market. Every aspiring competitor faces the possibility of failures, explosions, and billions of dollars in wasted investment. Such challenges are measured not in years but potentially in decades. Jeff Bezos recently received a painful reminder of that reality following the explosion of Blue Origin’s New Glenn rocket. It is therefore not surprising that investors are assigning value to many of the factors that do not easily fit into traditional valuation multiples. These include SpaceX’s competitive moat, its NASA contracts, the trust it has earned from the US government, the strategic importance of Starlink, and many other intangible advantages.

When Vision Becomes Part of the Valuation

Once Musk’s ambitions for extraterrestrial data centers, AI expansion, and interplanetary infrastructure are added to the equation, the narrative becomes increasingly speculative. Space undoubtedly deserves a premium valuation. It is a strategically important industry with enormous long-term potential. However, assigning value today to projects involving the Moon, Mars, or orbital data centers appears to be one of the few ways to justify a company worth nearly $3 trillion. The problem is that SpaceX is not yet generating meaningful revenue from these futuristic initiatives. Much like Tesla before it, investors appear willing to treat a potential future as if it were already certain. That future may arrive in five years, fifteen years—or perhaps not at all. This creates an interesting paradox. If all these possibilities have already been reflected in the stock price today, how much room remains for positive surprises? At a market capitalization of $2.66 trillion and annual revenue of just $18.67 billion in 2025, SpaceX appears to have almost no margin for error. Investors seem to be pricing in near-perfect execution across multiple highly ambitious business lines.

Speculation Is Also Driving Demand

The enthusiasm surrounding SpaceX cannot be explained solely by long-term investment conviction. A significant portion of demand is likely driven by speculation and the desire to participate in a powerful momentum trade. When combined with a relatively small free float, demand becomes concentrated through a very narrow channel, creating the conditions for highly asymmetric price movements. The result is a stock that can move dramatically higher regardless of underlying fundamentals, simply because there are not enough shares available to satisfy investor demand.

The Signs of a Bubble

Yes, SpaceX’s valuation displays many characteristics of a speculative bubble. That does not necessarily mean it must burst tomorrow. As long as investors continue to believe in the story, the valuation can remain elevated. It could even move significantly higher if additional positive catalysts emerge. Stocks can detach from economic reality for days, months, or even quarters before eventually reconnecting with fundamentals. However, there are limits to both optimism and valuation. If surpassing Amazon is not considered a warning sign, perhaps approaching Nvidia’s valuation—which would require only another doubling in the share price—might force investors to reconsider whether they are overestimating Musk’s business genius, the size of the addressable market, or the achievable growth rate. The more investors recognize the extraordinary assumptions embedded in SpaceX’s valuation, the greater the probability of a painful encounter with a financial asteroid.

A Correction Would Not Change the Business

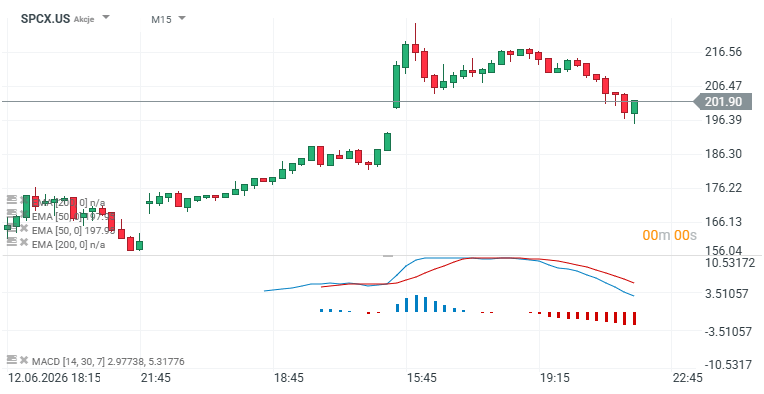

Importantly, any future decline—or even a major crash—in SpaceX shares would have little to do with the company’s operational performance. The company would still launch rockets, pursue new missions, expand Starlink, and continue investing in AI and related technologies. None of those activities require a $3 trillion valuation. Markets received a small preview of profit-taking yesterday when the stock fell from above $220 to roughly $200 by the closing bell. Yet even after that pullback, the valuation remains far removed from levels that many fundamental investors would consider reasonable. Investor optimism remains exceptionally strong. Another signal worth monitoring is the growing volume of equity and debt issuance by technology companies seeking to raise capital while market conditions remain favorable. If this trend continues for long enough, investors may eventually discover that they have exhausted their capacity to fund the next wave of speculative opportunities.

SpaceX (SPCX.US) share price chart

Source: xStation5