Markets rebound following Trump’s declarations

Following Friday’s declines in the US markets, a correction has hit Europe and Asia. The sell-off was fueled not only by growing expectations of FOMC monetary policy tightening after the release of stellar NFP data, but also by higher energy commodity prices. The downturn was halted by announcements from President Trump, who declared a temporary ceasefire between Iran and Israel.

Geopolitics

Overnight from Saturday to Sunday, Israel carried out an attack on military targets in Iran—the first since the ceasefire agreed upon on April 8th. The Israeli Air Force struck several targets in a petrochemical complex in the Mahshahr region of southwestern Iran. This morning, Iran launched a retaliatory action. Renewed shelling was also recorded from the Israeli side. Around noon, President Trump announced a temporary ceasefire between the parties. However, the Iranian armed forces have stated that it will be broken in the event of another Israeli attack on Lebanon.

Commodities

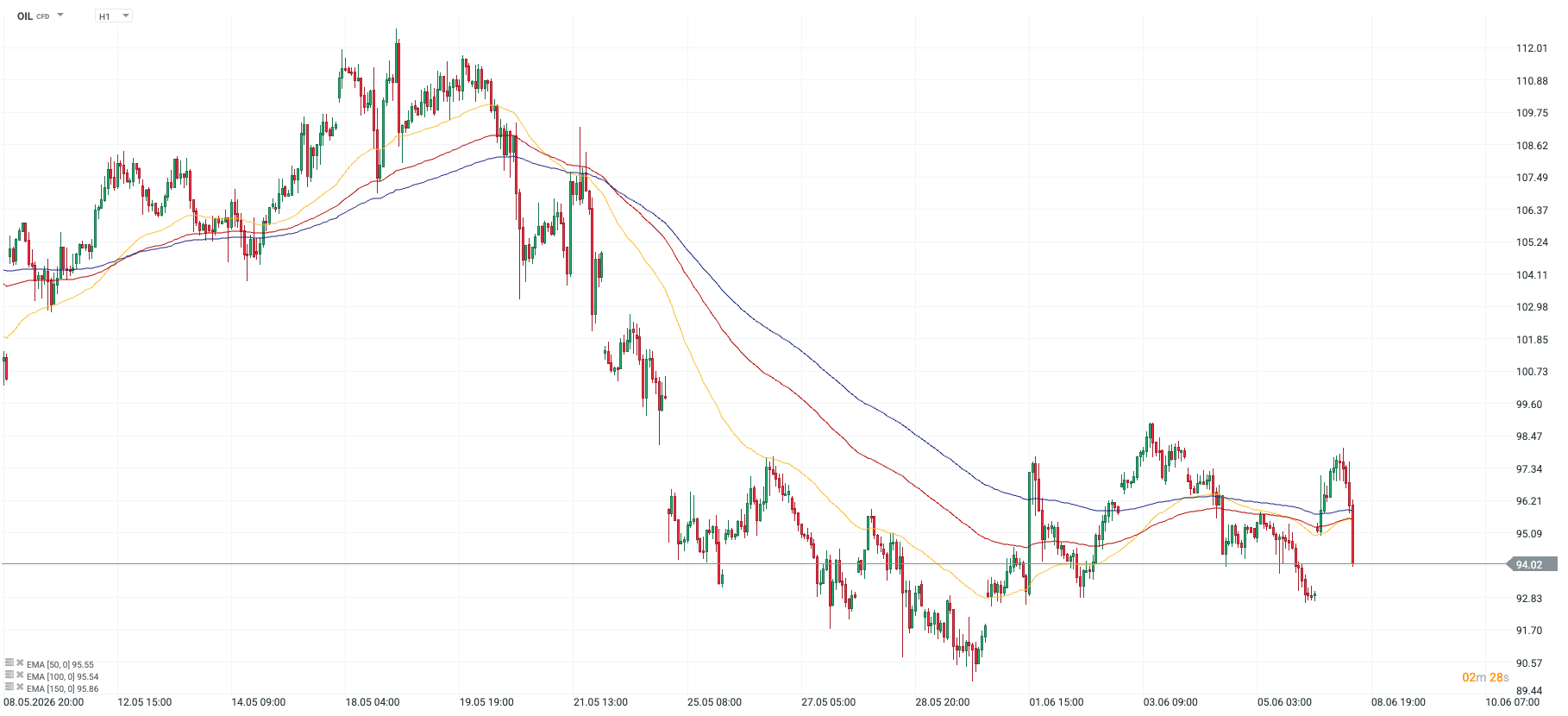

Today’s announcements from the White House significantly capped the substantial gains in crude oil prices, with Brent currently up +1% and WTI up +0.9%. Upon the opening of the European markets, the scale of these increases had reached over 4%. Chart 1: OIL (08.05 – 08.06)

Source: xStation, 08.05.2026

Indices

In the European market, the weakness of the German DAX stands out (-0.4%), though the French CAC 40 (-0.1%), Swiss SMI (-0.2%), and Polish WIG20 (-0.1%) are also trading in the red. On the winning side, the Italian FTSE MIB is gaining (+0.5%), along with the Spanish IBEX 35 (+0.1%).

Sectors

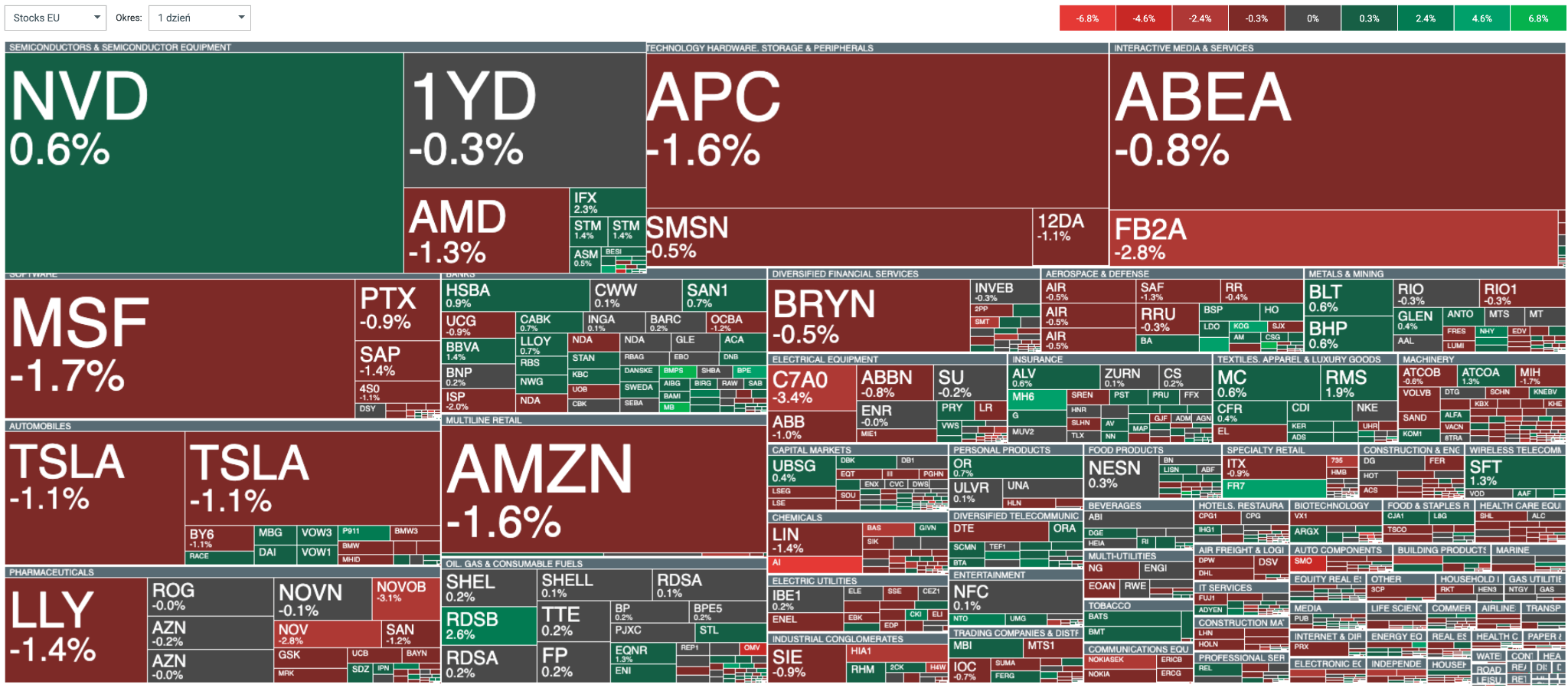

During Asian trading hours, declines were recorded across most sectors. Previous leaders – AI ecosystem companies and semiconductor manufacturers – performed particularly poorly, weighed down by positioning in the options markets. This was highly visible in South Korea, which witnessed a more than 10% drop in Samsung and a nearly 8% loss for SK Hynix today – companies that together account for approximately 50% of the KOSPI index. Currently, the situation is stabilizing slightly. Chart 2: Heatmap for the European market (08.06.2026)

Source: xStation 08.06.2026

Companies

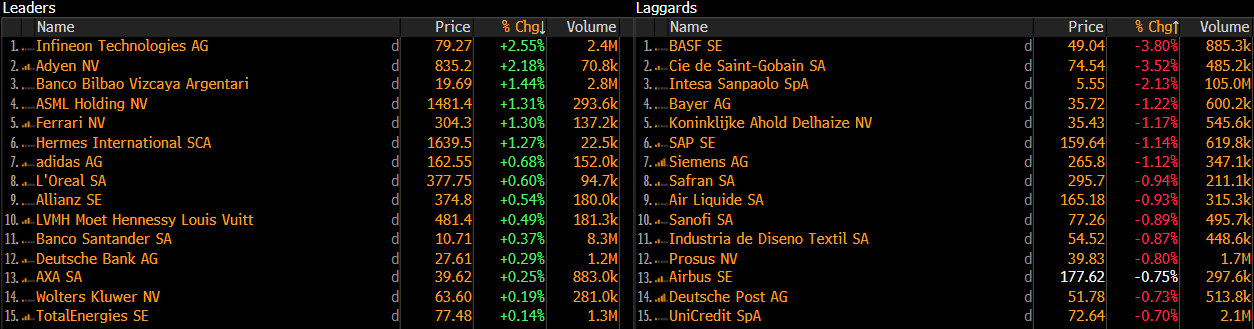

At the bottom of the Stoxx 50 ranking, we find BASF (-3.8%) – the German chemical giant, Cie de Saint Gobain (-3.5%) – the French industrial conglomerate, and Intesa Sanpaolo (-2.1%) – the Italian banking sector powerhouse. The case of Intesa seems particularly interesting – the shares fell after the company announced a €30.6 billion takeover bid for the world’s oldest bank (Banca Monte dei Paschi di Siena). Chart 3: Gainers and Losers in the Euro Stoxx 50 (08.06.2026)

Source: Bloomberg, 08.06.2026