AI bull market is safe. TSMC reports “stellar” quarterly print

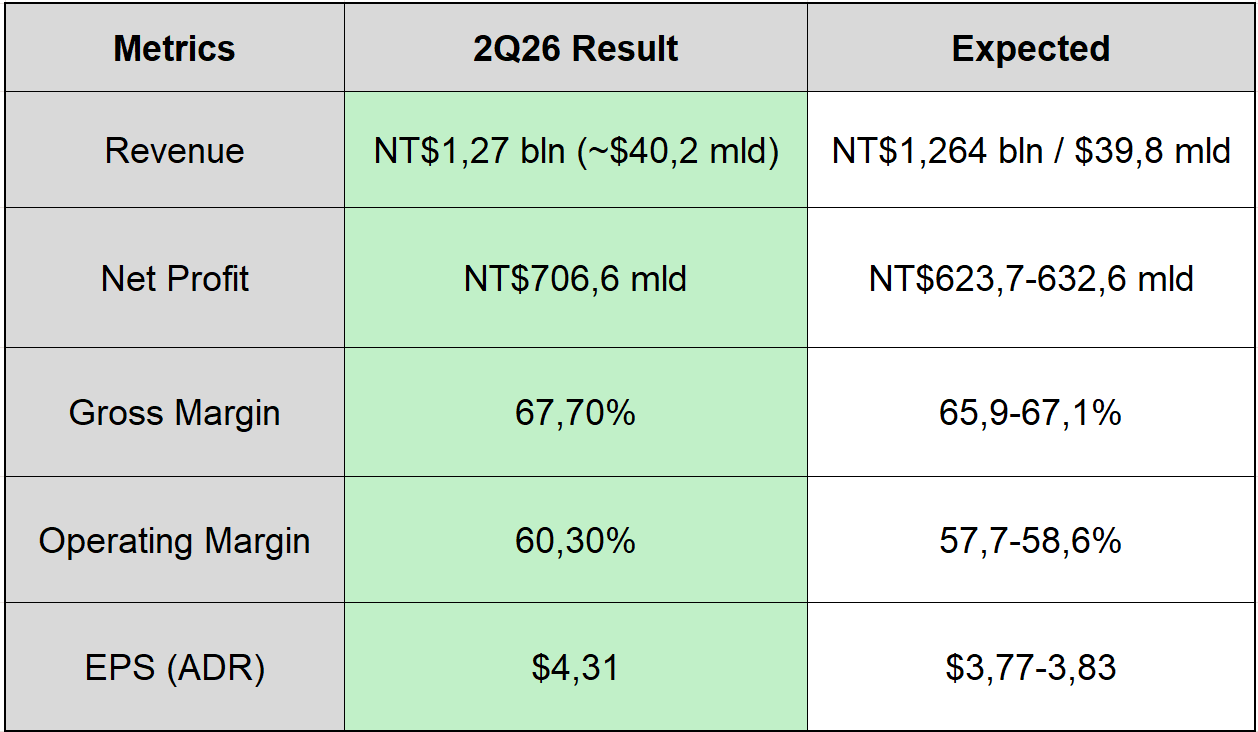

Taiwan Semiconductor Manufacturing Company (TSM.US) published its results for the second quarter of 2026 on Thursday, which significantly exceeded market expectations and confirmed that the boom in AI chips shows no signs of abating. Net profit jumped by 77.4 per cent year-on-year to NT$706.56 billion, with revenue of NT$1.27 trillion (approx. US$39.6–40.2 billion), representing a 36 per cent year-on-year increase.

Key figures for the quarter

The company exceeded analysts’ consensus forecasts across all key metrics – in terms of revenue, margins and operating profit.

A gross margin of 67.7% is particularly significant – TSMC not only exceeded its own forecasts, but did so thanks to cost improvements and higher capacity utilisation, rather than simply through volume. Source: XTB

Where does the company perform best?

The High Performance Computing segment (i.e. AI accelerators and server processors) is the clear driver of growth – its share of revenue rose to 66 per cent from 60 per cent a year earlier, whilst the share of smartphones fell to 22 per cent. Geographically, North America increased its share to 78% of revenue, reflecting the scale of orders from Nvidia, Apple and Broadcom for the most advanced nodes.

- 7nm and below technologies (advanced technologies) accounted for 77% of wafer revenue, compared with 74% in Q1

- The 3nm node already accounts for 30 per cent of revenue from wafers, whilst the 2nm node is only just getting started at 3 per cent, but is growing rapidly

- Waffle deliveries rose to 4.34 million units from 4.17 million in Q1

- Cash and securities rose by NT$134.4 billion to NT$3.52 trillion

It is worth noting that inventory rose by 7 days to 87 days due to the N2 ramp-up (2nm) – this is a natural consequence of preparations for next-generation production, not a sign of sales problems.

Forecasts for Q3 and the whole of 2026 The management board has significantly raised its expectations, which is the most important message for investors in this report.

- Q3 2026 revenue: $44.6–45.8 billion, representing a +12% quarter-on-quarter increase and a +37% year-on-year increase at the midpoint of the range

- Q3 gross margin: 65–67 per cent, operating margin: 56–58 per cent

- Full year 2026: revenue growth of “slightly over 40 per cent” year-on-year in US dollars, revised upwards from the previous “>30 per cent”

- Capex 2026: raised to $60–64 billion from $52–56 billion – a historic surge in investment

CEO C.C. Wei emphasised that “the AI megatrend is driving growing computational needs, which is increasing demand for the most advanced silicon”, and that the company will not be able to meet US demand for years to come, despite expanding its capacity in the US. Expansion in the US and new technology hubs

TSMC has announced an additional investment of $100 billion in Arizona (bringing the total to around $265 billion for the campus), comprising new factories and advanced packaging facilities, which is in line with the Trump administration’s policy on reshoring manufacturing. In addition, the company is building three new 3nm fabs – in Taiwan, Arizona and Japan – and the next-generation A14 technology is set to enter mass production in 2028, having already attracted strong interest from customers in the smartphone and HPC sectors.

Lessons for the future

TSMC’s results and revised forecasts send a clear signal that demand for AI infrastructure still outstrips supply, rather than the other way round – which allays concerns about a ‘bubble’ in spending by hyperscalers such as Meta. At the same time, the CFO indicated that capital expenditure over the next three years will be “significantly higher” than in the past three years, which implies further pressure on free cash flow, but also confirms the long-term nature of the AI investment cycle. For TSM shares (already up 40% this year), the key risks remain valuation and the pace of the 2nm ramp-up, whilst fundamentally the company is strengthening its near-monopolistic position in the production of the most advanced chips.

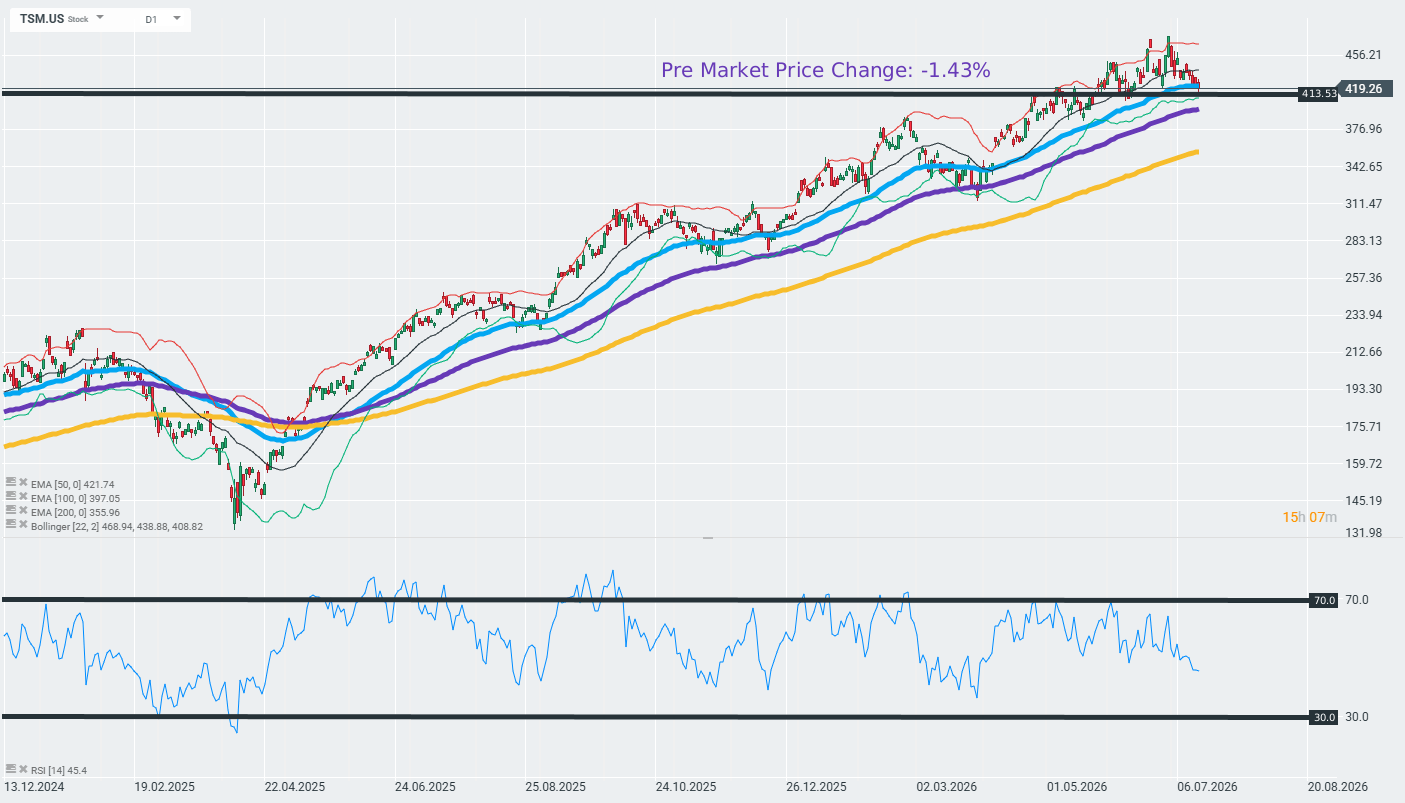

The daily chart for TSM shares shows a strong upward trend from April 2025 (low of around USD 135) to July 2026, with the price currently in the USD 413–419 range, shortly after the publication of record results for Q2 2026. The share price is trading above all key EMAs (50, 100, 200), which confirms the ongoing uptrend, although the RSI at 45.4 indicates a temporary cooling of momentum following the recent peak around $456. There is also pre-market movement of -1.43%, suggesting short-term profit-taking following a series of new highs and the publication of quarterly results, although the fundamental momentum from the results remains positive. Source: xStation