Market Brief – The Yen’s Bullish Rally! What Will Today’s Session Bring

Geopolitics

Tensions between the US and Iran remain in the spotlight, although the markets view the conflict as ‘under control’ after a senior US official confirmed overnight that technical talks with Tehran would continue. President Trump had earlier announced at the NATO summit in Ankara that the ceasefire with Iran was “over”, but later stated that Iran had called seeking to reach an agreement. Iran controls traffic through the Strait of Hormuz, treating it as its “golden weapon” and a priority more important than its nuclear programme – tanker traffic has fallen to 13 per day from an average of 33 last week. Qatar and Pakistan are mediating in attempts to bring Washington and Tehran back to the negotiating table.

Economy

Japan’s producer price index (PPI) for June rose by 7.1 per cent year-on-year, well above expectations (6.8 per cent) and the May reading (6.3 per cent), keeping the Bank of Japan on course for further interest rate rises. Japan’s Finance Minister Katayama announced measures to encourage the GPIF pension fund to invest significantly more in domestic financial assets, which allayed concerns about the BOJ’s independence following the sell-off in JGBs. The yield on 10-year US Treasury bonds remains stable at 4.541 per cent, although portfolio managers are warning of rising volatility in the Treasuries market as the Fed adopts a more reactive stance.

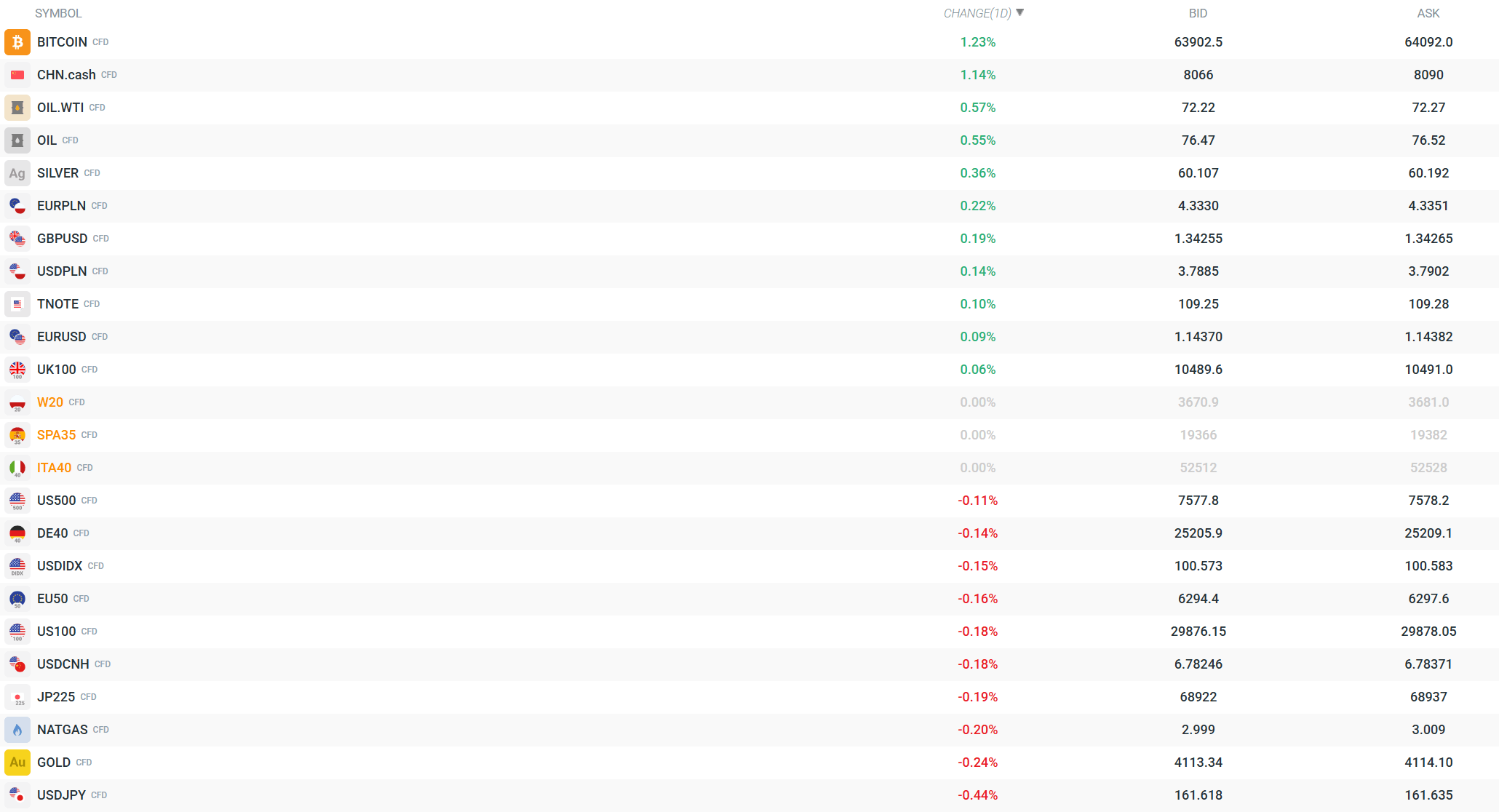

Movements in the main indices (Wall Street, Thursday’s close)

The Nasdaq Composite rose by 1.3 per cent, the S&P 500 gained 0.8 per cent, and the Dow Jones closed 0.3 per cent higher – gains driven by a rally in semiconductor stocks following the announcement of major investments by a major US memory manufacturer. Futures on US indices were down slightly on Friday morning (the S&P and Nasdaq were down by around 0.1%), whilst the Dow was flat.

Markets in Asia

Asian markets soared on Friday, driven by a rebound in the AI chip sector. The Kospi jumped by over 4% (Kosdaq +5.9%), whilst the Nikkei 225 gained around 1.5–2% and the Topix rose by nearly 0.5–0.75%. The Hang Seng rose by 0.45–1.86 per cent, and the Chinese CSI 300 gained 0.33–0.4 per cent – Morgan Stanley notes that Hong Kong and China have recently been clearly outperforming regional markets. Despite Friday’s rebound, the KOSPI remains on course for a third consecutive week of losses.

Currencies

The yen has strengthened significantly following Katayama’s comments regarding the GPIF. Analysts emphasise that the structural flow of capital from pension funds (currently 50 per cent of foreign assets) may provide more lasting support for the yen than currency interventions. The dollar is performing poorly, but the Polish zloty is faring even worse, hitting its lowest levels in a year against both the euro and the dollar.

Commodities

Oil prices remain stable within narrow ranges – Brent is trading at around USD 76.40–76.57 per barrel and WTI at USD 72.22–72.34 per barrel, following a easing of concerns over energy infrastructure. Citi maintains its base-case scenario for Brent at US$75 in the third quarter, assuming a US-Iran agreement and the reopening of the Strait of Hormuz. Gold is down slightly (-0.21%, trading at around US$4,114–4,116), silver is up 0.58% (60.24–60.32), whilst natural gas is up by 0.17%.

Companies

SK Hynix is set to make its debut on the Nasdaq on Friday via ADRs priced at US$149 per share, with the IPO oversubscribed and the company raising approximately US$26.5 billion in capital. The company is trading at 4.8x forward earnings compared with an industry median of 29.84x, raising questions about a narrowing of the so-called “Korean discount”. SoftBank Group rose by over 11%, whilst Samsung Electronics gained 4.3% in response to the rally in AI chips; meanwhile, the aviation market’s attention will be focused on Delta Air Lines’ quarterly results on Friday morning.

Cryptocurrencies and a summary of the trading session

Bitcoin is trading up 1.14%, within the range of US$63,851–64,041, continuing the positive market sentiment. Today’s European session is likely to be driven primarily by SK Hynix’s debut on the Nasdaq, Delta Air Lines’ results, and further developments regarding US-Iran talks and capital flows from Japanese pension funds.

Volatility currently observed across the key instruments. Source: xStation