China nears bear market territory – Alibaba and Tencent lead selloff

China’s main equity benchmark is approaching bear market territory, highlighting growing investor concerns over the country’s economic outlook. Pressure is concentrated in large internet and consumer companies, which account for a significant share of major offshore Chinese equity indices. The weakness in Chinese equities is not driven solely by slower economic growth. An increasingly important issue is the structure of the MSCI China Index itself, which remains heavily concentrated in internet and consumer names.

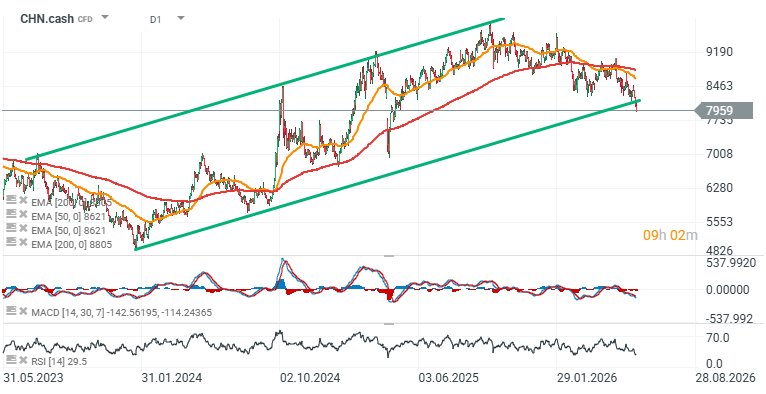

While global investors are allocating capital to semiconductor manufacturers and AI beneficiaries in South Korea and Taiwan, offshore Chinese benchmarks remain dependent on domestic consumption, the performance of Alibaba and Tencent, and sentiment surrounding the property sector. As a result, even if China’s economy stabilizes, the country may continue to lose the battle for global capital flows to other Asian markets that offer more direct exposure to the AI investment cycle. The MSCI China Index fell as much as 2.1% today and at one point traded more than 20% below its October 2 peak, putting it on the verge of a technical bear market. Alibaba and Tencent were the largest contributors to the decline, despite having long served as the cornerstone of international investors’ exposure to China’s technology sector.

What is weighing on Chinese equities?

Several headwinds are hitting the market simultaneously:

- Growing tensions with US institutions. Most recently, the Pentagon announced plans to add BYD and Alibaba to a list of companies alleged to be working with the Chinese government.

- Weakening consumer data in China.

- Retail spending contracted in May for the first time since the pandemic.

- Disappointing results from the country’s largest internet platforms.

- Intense domestic and international competition from markets such as Japan, South Korea, and Taiwan, while China continues to carry a higher geopolitical risk premium.

- Heavy AI-related investment spending that is pressuring margins in the short term.

- Capital flows shifting toward markets that benefit more directly from the global AI boom.

South Korea and Taiwan continue to benefit from strong demand for semiconductors and AI infrastructure due to their exposure to world-leading chipmakers. By contrast, MSCI China remains far more dependent on consumption trends, regulation, the property sector, banking confidence, and the earnings performance of internet platforms.

The structural problem of the MSCI China Index

MSCI China remains dominated by Hong Kong-listed internet and consumer companies. Tencent represents roughly 13% of the index, while Alibaba accounts for approximately 10%. This concentration means that weakness in just a handful of large companies can significantly drag down the entire benchmark. When Alibaba and Tencent disappoint, the index has limited ability to offset those losses through strength in other sectors. Unlike markets such as Taiwan and South Korea, offshore Chinese indices lack meaningful exposure to the pure AI hardware cycle. As a result, the global AI-driven rally has largely bypassed Chinese equities listed outside mainland China.

China’s technology sector is not a single story

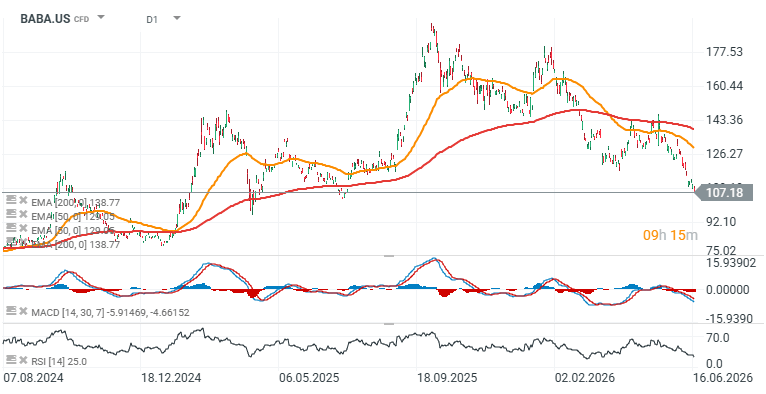

The weakness is concentrated primarily in internet and e-commerce companies. Alibaba and Tencent both reported March-quarter revenue below analyst expectations, raising concerns that massive AI-related investments may take longer than expected to translate into stronger profitability. At the same time, domestic Chinese technology indices are performing considerably better. The Star 50 Index, which includes semiconductor manufacturers and advanced technology firms, climbed to a record high today. This highlights an important distinction: investors are not abandoning Chinese technology altogether. Instead, they are becoming increasingly selective, favoring companies linked to semiconductors, advanced manufacturing, and China’s domestic AI supply chain.

Hang Seng China Enterprises Index remains under pressure

The pressure is also visible in the Hang Seng China Enterprises Index, which fell more than 2% today. The benchmark is currently one of the weakest-performing major equity indices globally this year among more than 90 indexes tracked by Bloomberg. Meanwhile, the Hang Seng Tech Index entered a bear market earlier this year, suggesting that weakness in Chinese technology stocks is not merely a short-term correction but part of a broader loss of confidence in large internet platforms.

Why are China’s markets disappointing investors?

Chinese equities remain under pressure because investors still do not see a clear catalyst for a structural recovery. The challenge extends beyond weak sentiment and includes the composition of the indices themselves, which remain heavily dependent on consumption, internet platforms, and the earnings of a small number of mega-cap technology companies. Until consumer spending begins to recover and companies such as Alibaba and Tencent deliver a more convincing improvement in earnings, MSCI China is likely to remain vulnerable to further downside pressure. At the same time, the relative strength of China’s domestic semiconductor benchmarks suggests that investors continue to seek exposure to China, but increasingly in a selective manner and primarily through companies directly tied to the AI investment cycle.

Are Chinese technology companies losing the AI race to South Korea and Taiwan?

One of the main reasons behind MSCI China’s underperformance is its limited participation in the global AI-driven rally. While South Korean and Taiwanese markets continue to benefit from record demand for semiconductors and AI infrastructure, offshore Chinese indices remain dominated by internet platforms and consumer businesses. According to Vey-Sern Ling of Union Bancaire Privée, Chinese technology companies have effectively become “victims of the success of their North Asian neighbors.” Investors are increasingly choosing semiconductor manufacturers that are direct beneficiaries of AI investment rather than internet platforms such as Alibaba and Tencent. This has significantly increased the opportunity cost of holding Chinese technology stocks. Global capital is naturally flowing toward markets where earnings growth is more visible, particularly South Korea and Taiwan. Just a few years ago, Alibaba, Tencent, and other internet platforms were the primary investment case for offshore Chinese equities. Today, that narrative is gradually losing momentum. First-quarter results showed that both Alibaba and Tencent missed revenue expectations. Profitability is being pressured by three major factors:

- Rising investment spending on artificial intelligence.

- Extremely intense domestic competition.

- Continued weakness in Chinese consumer demand.

For investors, this represents a meaningful shift in the narrative surrounding China’s technology sector. Internet platforms continue to generate substantial cash flows, but they are no longer viewed as the unquestioned growth engine of the Chinese equity market as they were before the pandemic and before the regulatory crackdown on the sector.

CHN.cash Index and BABA.US Shares (D1 timeframe)

Source: xStation5

Source: xStation5