Cocoa rises on a wave of rebounding demand in Asia. Europe remains in retreat

The cocoa market is currently experiencing a fascinating geographical split. While the Old Continent grapples with stagnation and falling demand, Asian tigers are processing the raw material on a massive scale, reaching the highest processing levels in many years. The cocoa market is currently facing many problems, primarily the possible occurrence of the strongest El Niño in up to 70 years. On the other hand, current weather in Africa may signal better harvests in the next season. What do the data show?

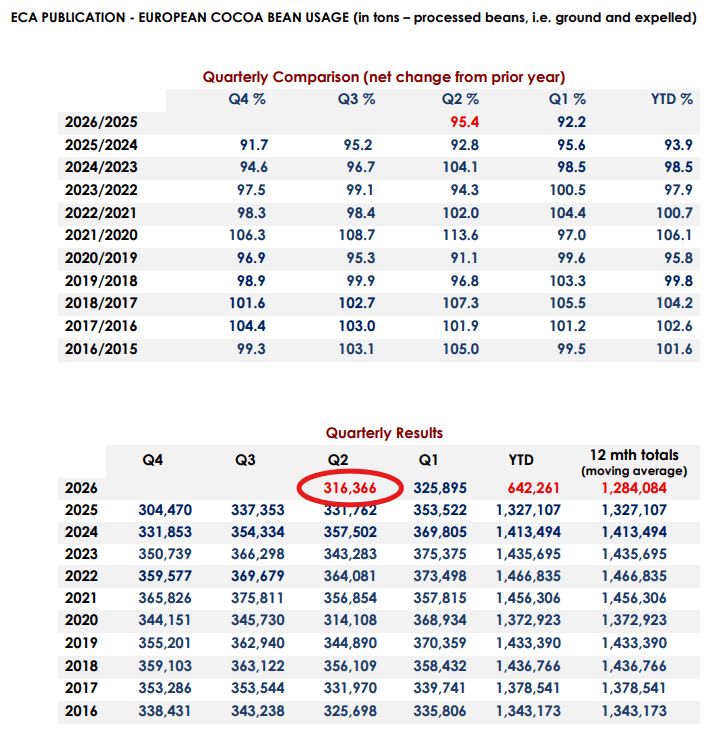

Disappointment in Europe (Q2)

European processing data, i.e., cocoa grindings, proved to be a cold shower for optimists hoping for a stabilization of Western demand.

- Data: The European Cocoa Association (ECA) reported that processing in Q2 fell by 4.6% year-on-year, reaching 316,366 tonnes (compared to 331,762 tonnes in the same period last year and compared to expectations of 325,000 tonnes).

- Below expectations: This decline is significantly deeper than analysts polled by Bloomberg had estimated, who expected a decrease of only 1.5%.

- Quarterly trend: This result is also weaker than the previous quarter (325,895 tonnes). This shows that record-high raw material prices and inflationary pressure have effectively hit the margins of European confectionery manufacturers.

This is the worst second quarter in at least 10 years. It is also worse than Q1 2026. Source:

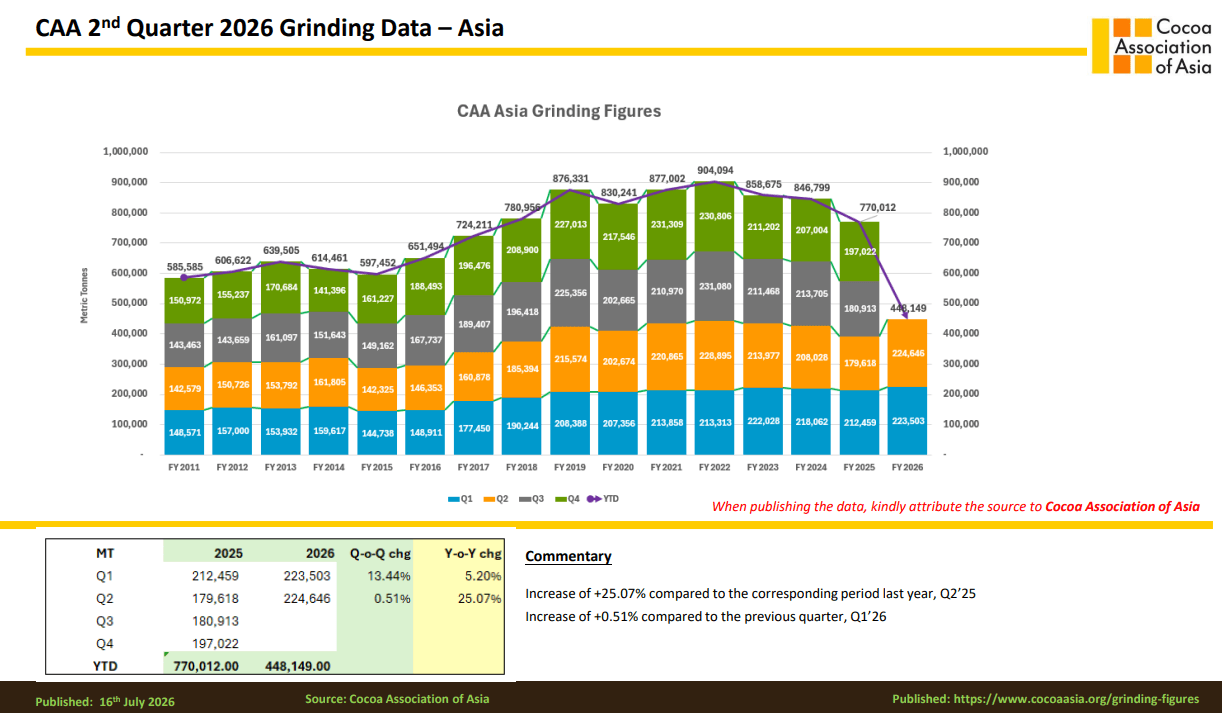

ECA Powerful rebound in Asia In total opposition to Europe, the latest Asian data point to a powerful recovery in the processing industry.

- Total Asia (CAA): Cocoa processing in Q2 grew by an incredible 25.07% year-on-year, reaching 224,646 tonnes.

- Malaysia (MCB): Data from Malaysia itself confirm this trend, where the local industry recorded a growth of as much as 29.4% year-on-year to 90,849 tonnes. In the first half of the year (1H), Malaysian processing grew by a solid 18.1%.

- Recent data from Barry Callebaut suggested a strong rebound in consumer demand in Asia and continued stagnation in the Western world.

Data from Asia show the best second quarter since at least 2011. Source: CAA Will Asia become the primary demand force? Comparing volumes in absolute terms, Europe still holds the leadership position:

- Europe (Q2): ~316 thousand tonnes

- Asia (Q2): ~225 thousand tonnes

The difference is currently about 91 thousand tonnes in Europe’s favor. Although the Old Continent still holds the quantitative palm of victory, Asia is currently the undisputed engine of global demand growth. The takeover of the leadership position by Asian markets in the medium term is highly probable for three reasons:

- Growing middle class: Consumption of chocolate and cocoa products in countries such as China, India, and ASEAN states is constantly growing, while Western markets are already saturated.

- Operating costs: Processing is moving to where energy and labor costs are lower and markets are growing dynamically.

- Structural changes among producers: Plans by leading African producers (Ivory Coast and Ghana) to limit the export of raw beans and develop local processing will hit European factories, giving an advantage to more flexible emerging markets.

It is also worth noting that processing in the largest producing country, the Ivory Coast, grew by 28% year-on-year to 158,672 tonnes. At the same time, this was a slight decrease compared to Q1, when 169 thousand tonnes of cocoa were processed.

Analysis of weather and the specter of El Niño: What awaits us?

Current weather status (mid-July):

- West Africa (Ivory Coast, Ghana): Current rainfall favors vegetation and improves the condition of cocoa trees before the upcoming main harvest. Temperatures remain within the norm.

- Southeast Asia (Indonesia, Malaysia): Rainfall is more scattered and local, which is defined as unfavorable conditions for crops.

- Brazil (Bahia): Typical seasonal dryness is noted.

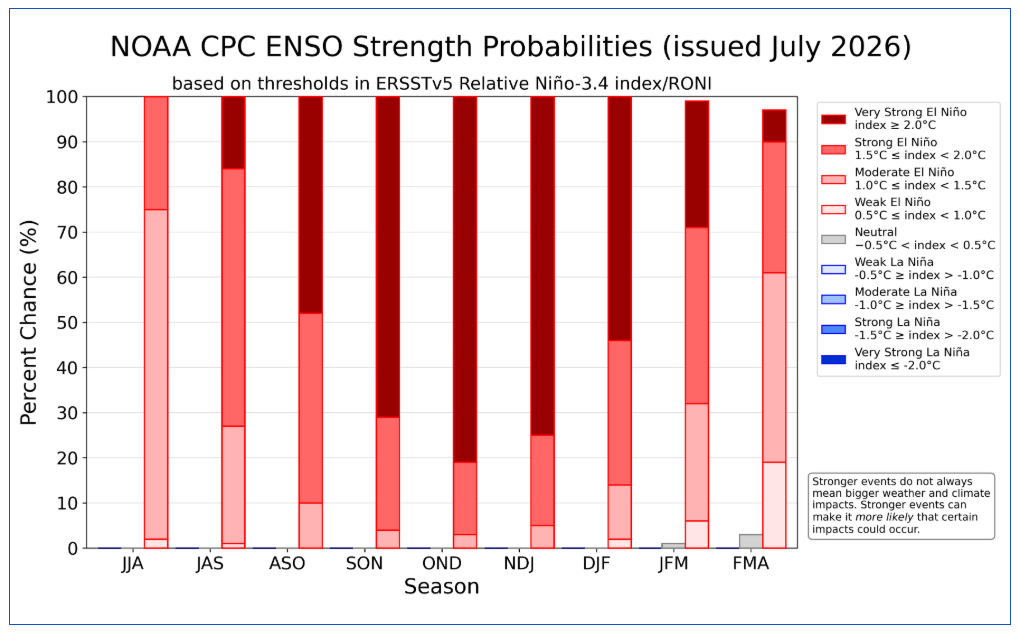

Impact and prospects of El Niño: According to current meteorological forecasts for the second half of the year, a strong El Niño phenomenon is developing in the Pacific. NOAA and WMO models indicate that water temperature anomalies have already reached high values (Niño 3.4 index above +1.5°C), which heralds one of the strongest El Niños in recent years, peaking at the turn of the year.

The NOAA model indicates an over 80% probability of a Super El Niño occurrence in the October-November-December period and 100% for the occurrence of the general phenomenon. Already, the temperature in the El Niño 3.4 region exceeds norms and currently indicates the occurrence of a moderate El Niño. Source: NOAA How will this affect the cocoa market?

- Drought in Southeast Asia: El Niño traditionally brings a deficit of rainfall and high temperatures in Indonesia and Malaysia. Current unfavorable and scattered rains in that region are a direct symptom of the coming drought. This may severely limit local harvests and force Asian processing plants to import more expensive beans from other parts of the world.

- Risk for West Africa: Although July rains provide a temporary respite to the Ivory Coast and Ghana, a strong El Niño at the end of the year usually brings a dry, desert Harmattan wind of increased strength and an acute lack of rainfall. This means that the current improvement in weather may be just the calm before the storm. If El Niño hits with the predicted strength, markets may collide with another deep supply crisis at the end of the year.

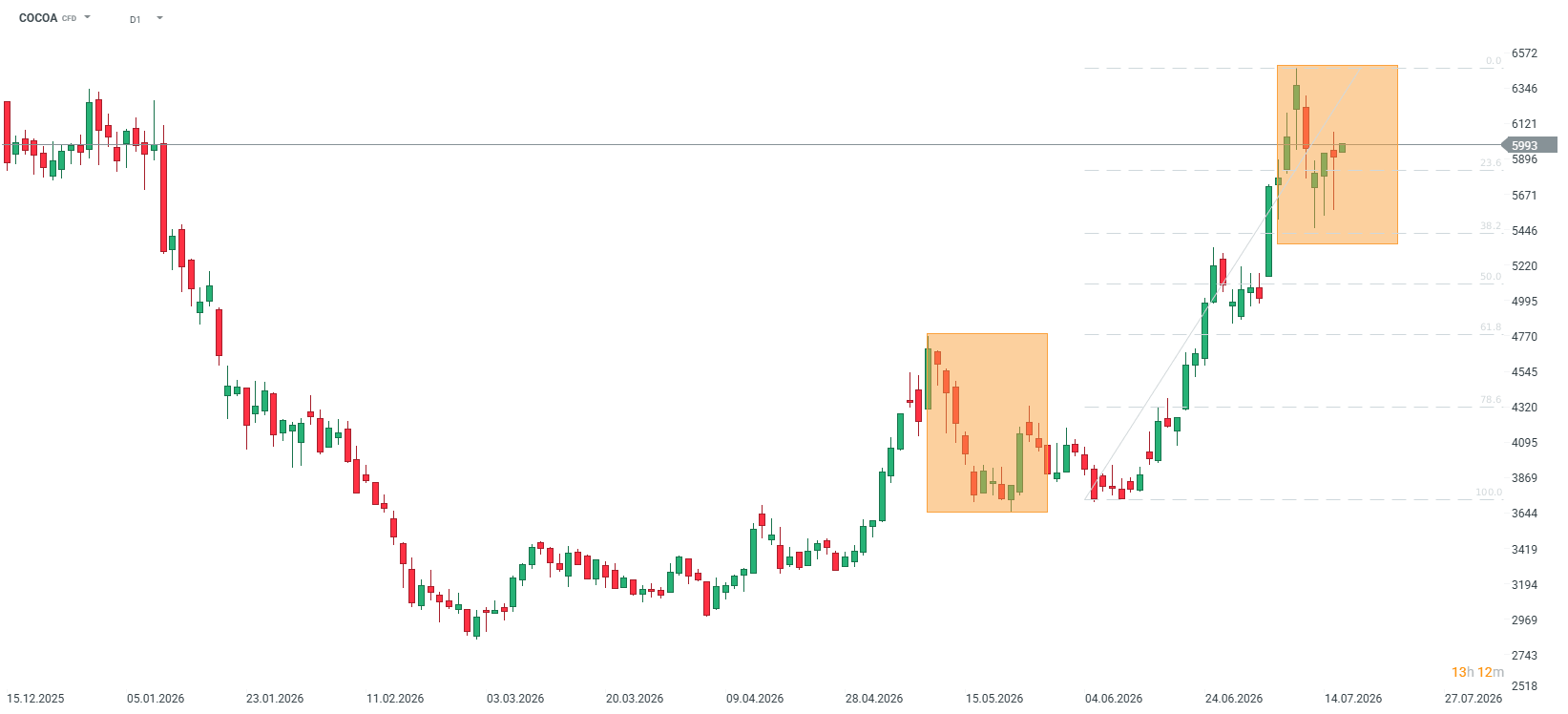

The price starts today’s session by continuing its recovery. It can be seen that the three previous sessions showed clear demand above 5500 USD per tonne. Source: xStation5