Oil:

- Price drop below key levels: The price of Brent crude oil briefly fell below the local low from June 18 and breached the USD 77 per barrel level. WTI crude oil is also showing strong market weakness under the influence of a fading geopolitical premium.

- Breakthrough in US-Iran talks: The main factor exerting downward pressure is progress in peace negotiations aimed at ending the four-month conflict. Washington has issued an official 60-day sanction waiver, which allows Tehran to legally sell oil on the international market.

- Huge amount of crude on water: Iran is rushing to liquidate stocks accumulated on tankers. It is estimated that there are currently about 68 million barrels of Iranian oil and condensates on the water, of which as much as 80% do not have a declared destination port and could go directly to the spot market. A large amount of Iranian and Persian Gulf oil is putting downward pressure on prices at the short end of the curve.

- Restraint of Asian refineries: Despite the temporary lifting of restrictions by the US, the largest importers in Asia (India, Japan, South Korea) are in no hurry to buy Iranian crude. Refineries have secured alternative supplies until August, and the barrier is still the binding insurance restrictions from the EU and the UK.

- Contango market structure: Prices of Middle Eastern benchmark grades (e.g., Dubai and Murban) have entered a contango structure, meaning that contracts for immediate delivery are cheaper than those for later delivery, confirming a physical oversupply of the raw material in the short term.

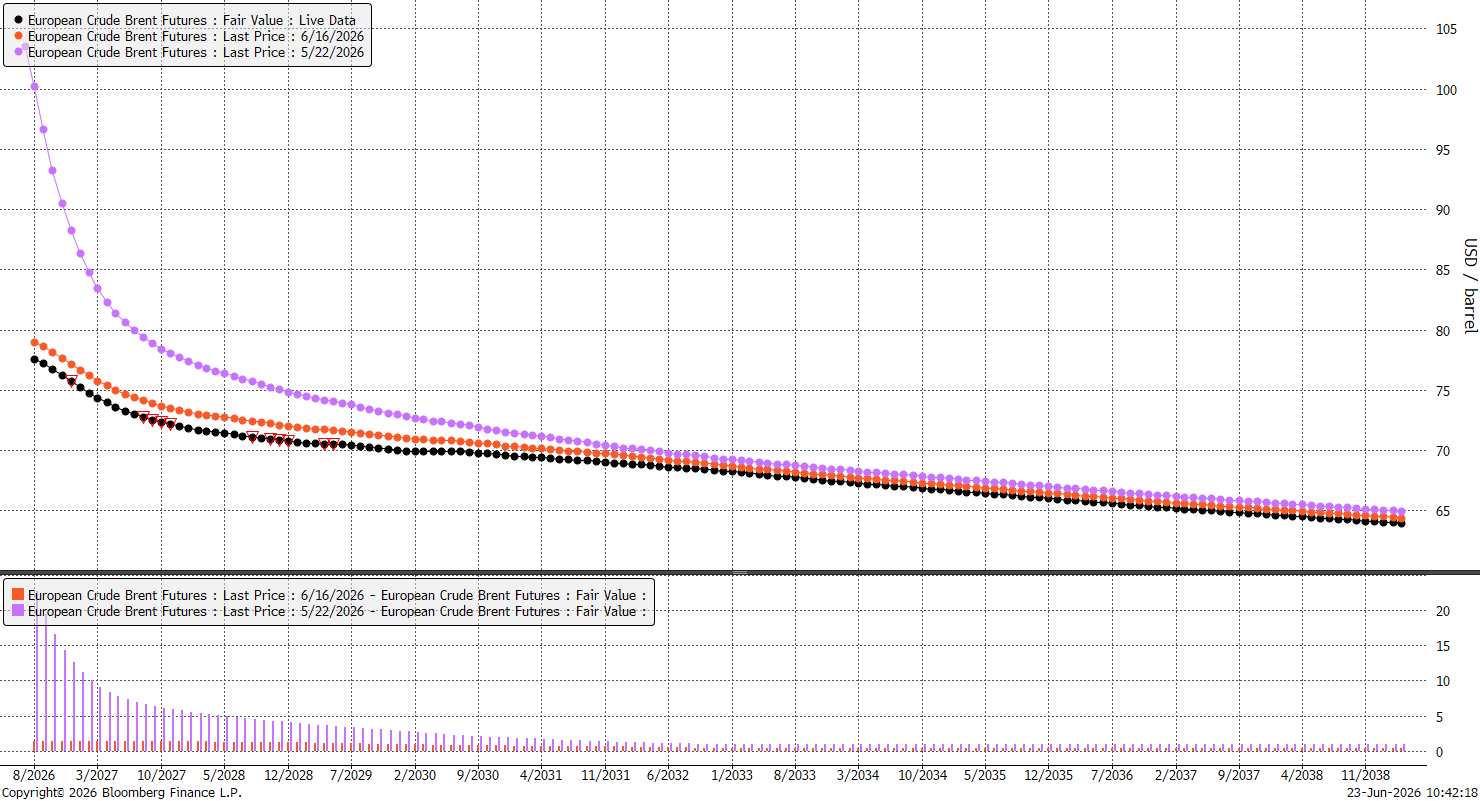

Backwardation in Brent crude is currently minimal compared to a month ago. Calendar spreads are clearly below $1 per barrel. Source: Bloomberg Finance LP, XTB

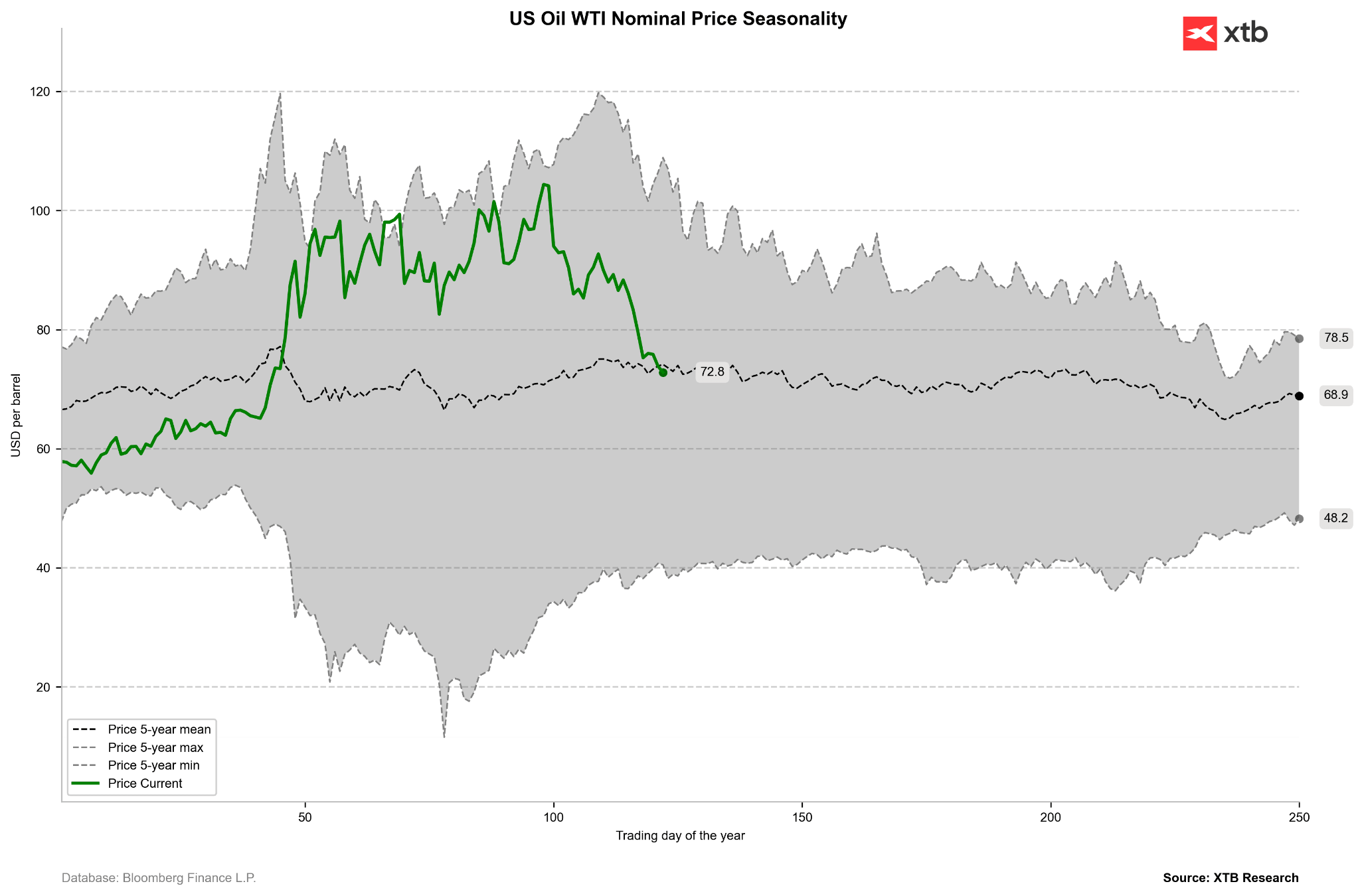

WTI crude prices have fallen to their 5-year average. Seasonality indicates slight downward pressure in the coming weeks. Source: Bloomberg Finance LP, XTB

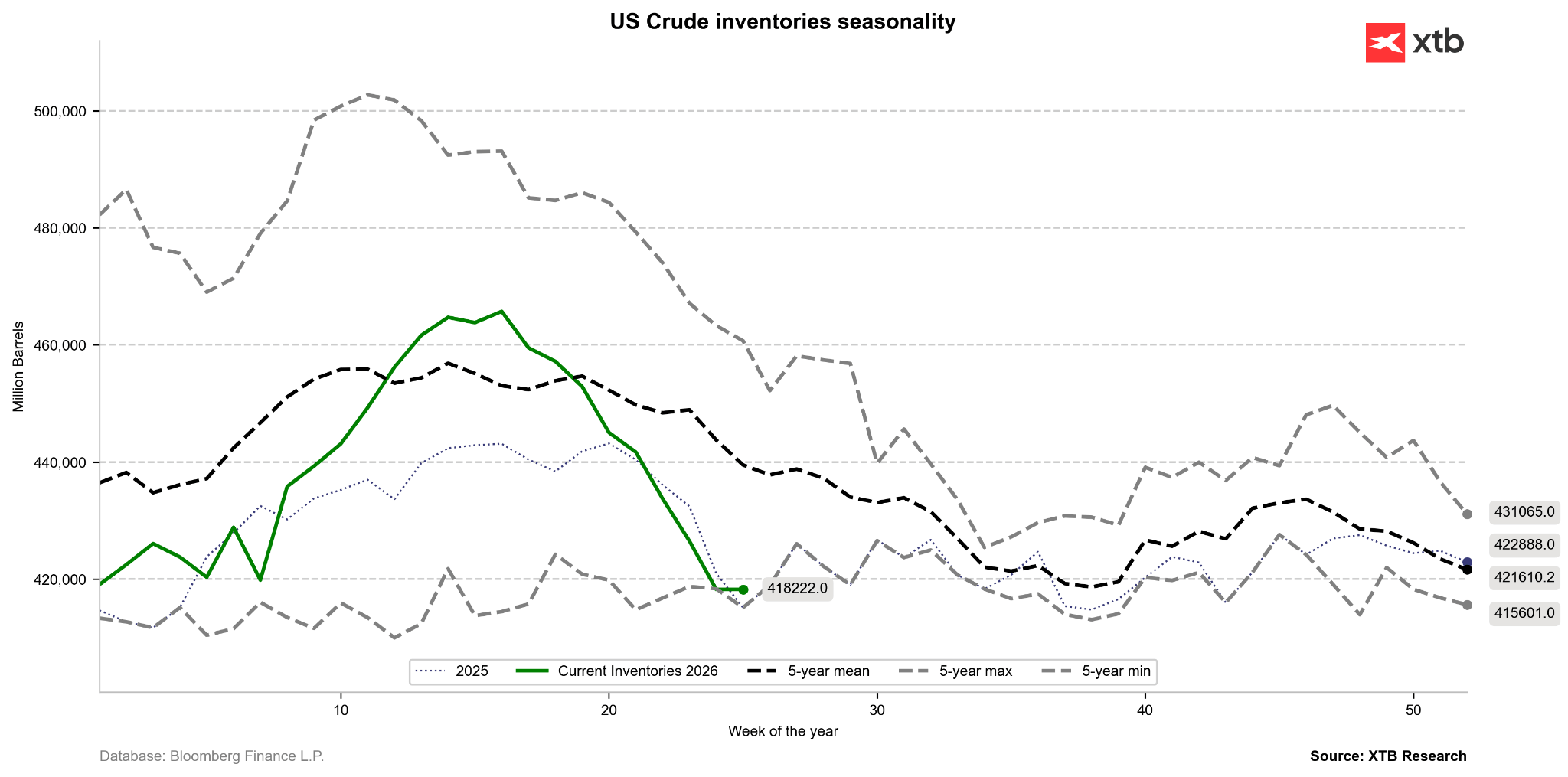

US crude oil inventories have fallen to a 5-year low. If inventories continue to fall, it could mean that the market has not returned to normal. It is worth noting, however, that seasonality indicates declines until the 39th week of the year. Source: Bloomberg Finance LP, XTB

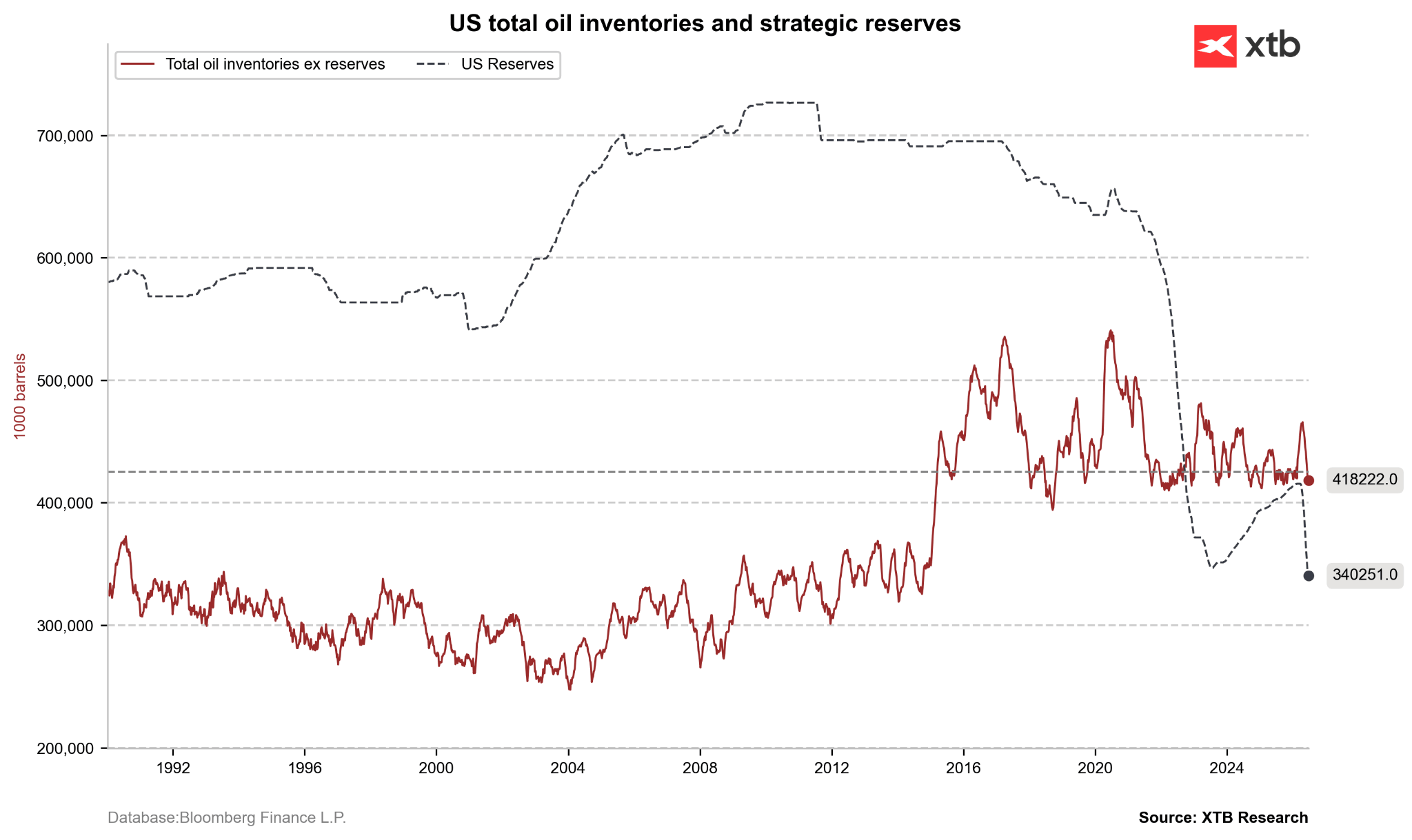

Strategic reserves in the US have fallen to their lowest level since the 1980s. Source: Bloomberg Finance LP, XTB

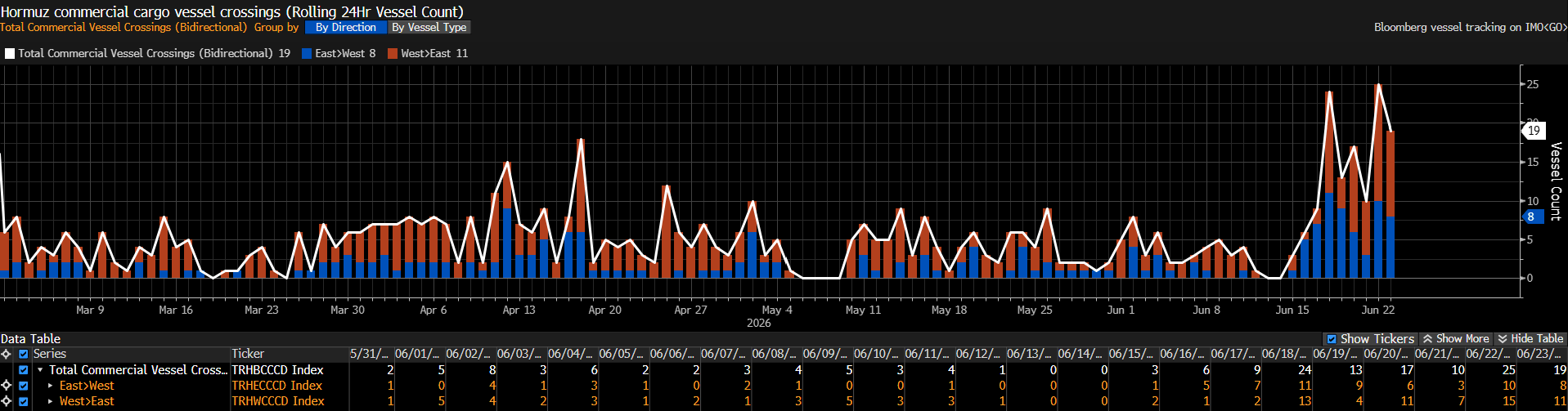

The number of ships passing through the Strait of Hormuz has increased, but it remains clearly below the pre-war average of around 120-140 ships. Source: Bloomberg Finance LP

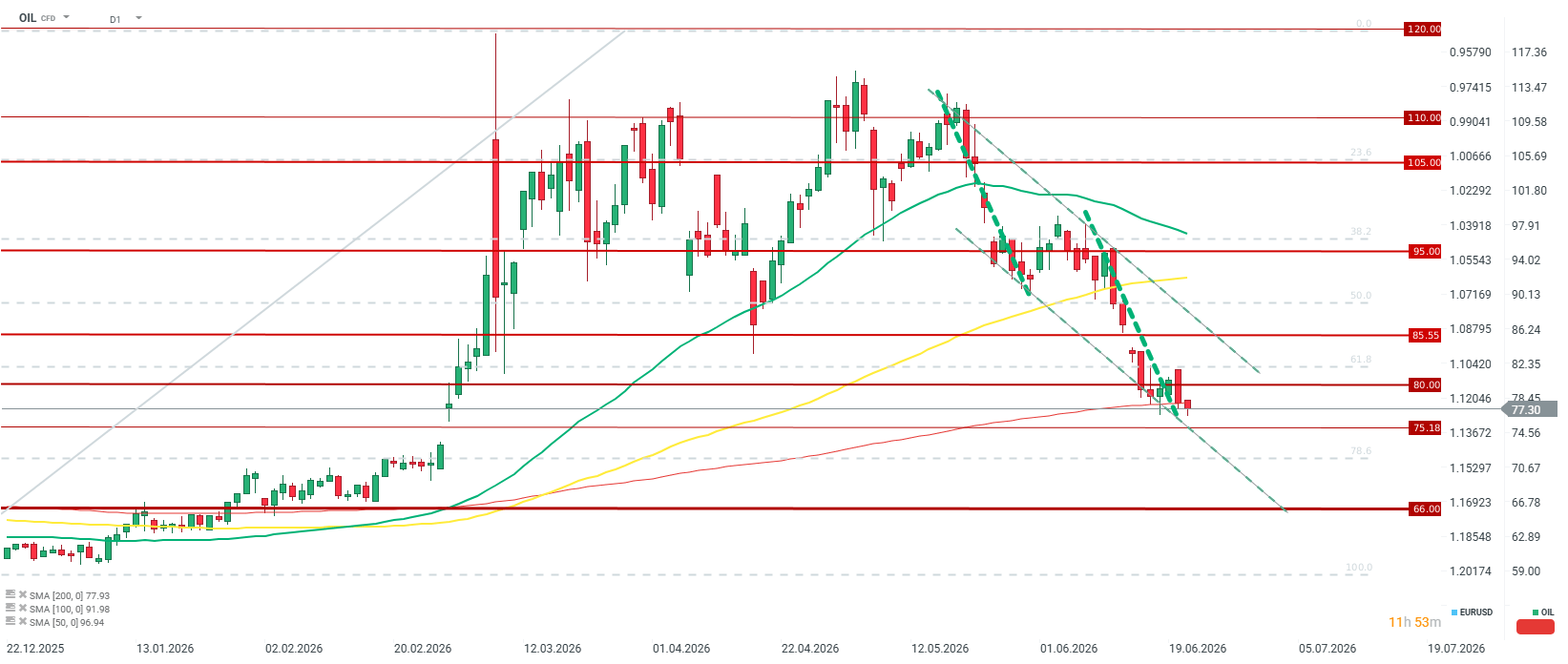

Oil is breaching last week’s local lows and testing the area of the opening price from the first session after the war in Iran. At the same time, we are observing tests of the 200-session average. Source: xStation5 Gold:

- Sell-off and technical collapse: The spot gold price plummeted by nearly 2% during the second session of the year, testing the USD 4100 per ounce level. The price is already clearly below the 200-period average, and short-term resistance is the 25-session average, which converges with the downward trend line.

- Hawkish pivot of the Federal Reserve: Pressure for price declines stems directly from a revision of expectations for US interest rates in the face of resilient macroeconomic data.

- The new Fed chief, Kevin Warsh, and committee members (e.g., Austan Goolsbee) have declared a hard fight against inflation, which is moving in the “wrong direction,” which cancels out the chances of interest rate cuts and creates a risk of further hikes. This trend is reinforced by the rising dollar.

- The market currently prices in chances for a hike as early as December and nearly 2 hikes in the entire cycle.

- Deutsche Bank lowered its gold price forecasts by as much as 22%, setting a target of USD 4300 in Q3 and USD 4800 in Q4. Analysts warn that another 3-4 Fed rate hikes could push the metal even to 3800 USD. It is worth emphasizing, however, that the market is currently pricing in less than 2 hikes.

- Goldman Sachs ściął prognozę na koniec roku o $500 do poziomu 4900 USD, rezygnując z oczekiwań na jakikolwiek ruch obniżkowy stóp w 2026 roku.

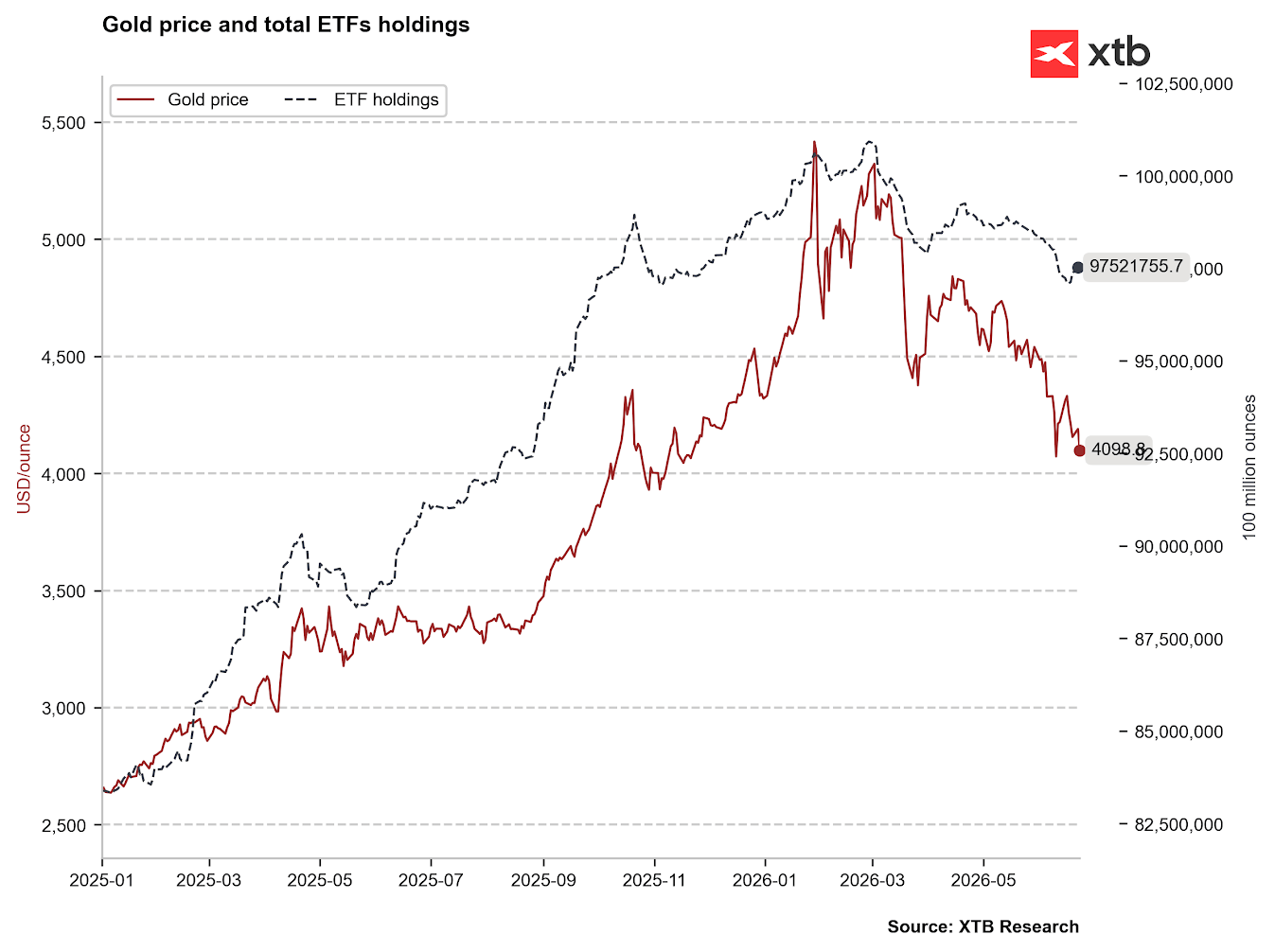

- Fading investment demand: Gold-backed ETFs have clearly reduced the amount of gold in their vaults to the lowest levels since November 2025. On the other hand, despite current downward pressure, ETFs have started to buy back gold slightly on the market.

- Demand in China is also weakening, as indicated by the discount of local prices relative to the Comex exchange.

- The only stable element of market support remains regular purchases by central banks. It is estimated that purchases in 2026 could exceed 1000 tons.

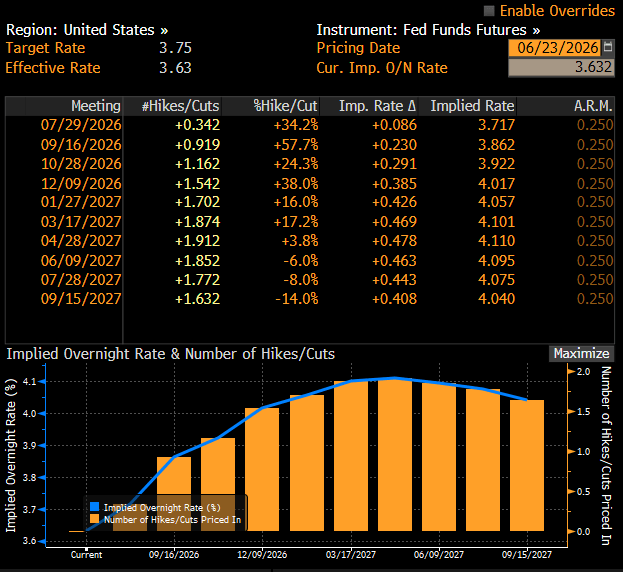

The market indicates a potential rate hike by the Fed as early as September. Source: Bloomberg Finance LP

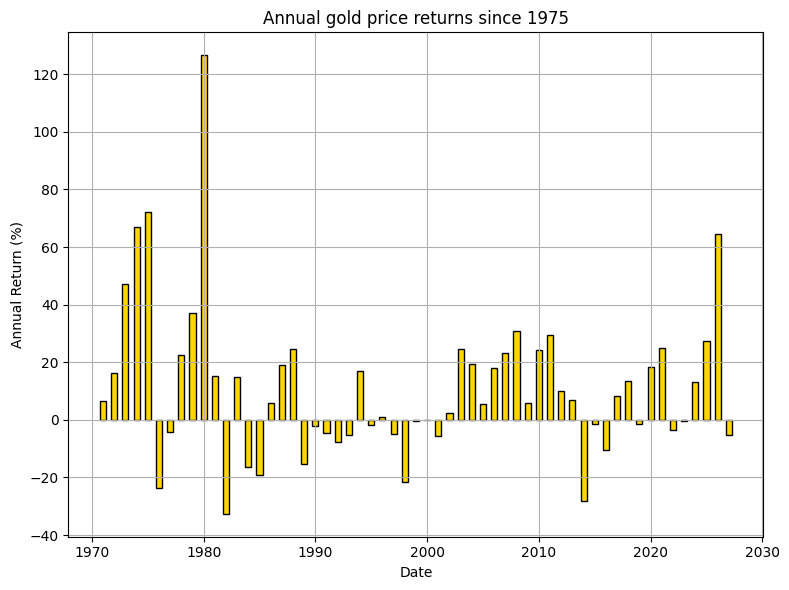

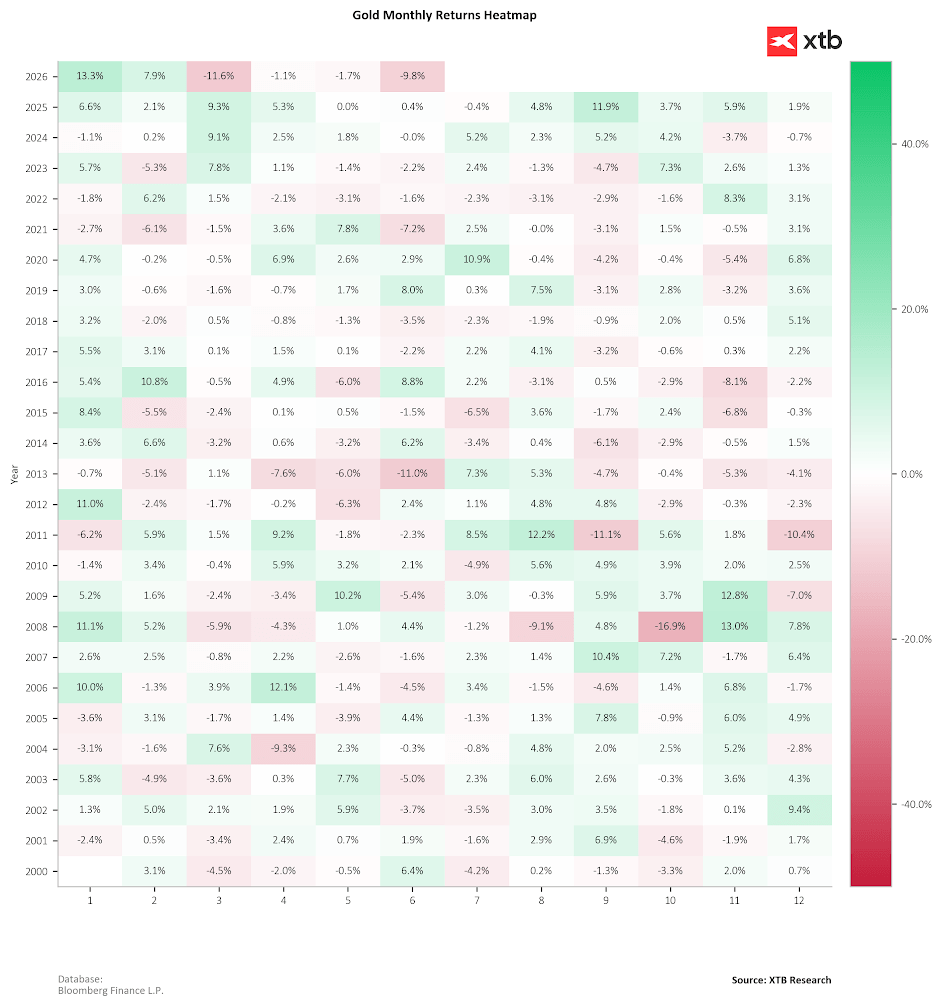

We are currently observing a year-on-year price decline. In history, we have only had a few periods in which gold lost value for several years in a row. The situation in the last decade of the 20th century looks the worst. Source: Bloomberg Finance LP, XTB

June declines are among the largest in the last several years, excluding the March sell-off. Gold has been losing for 4 months in a row. Recently, such a situation occurred in 2022. Source: Bloomberg Finance LP, XTB

Gold is under pressure, while ETFs have stopped further gold sell-offs. Source: Bloomberg Finance LP, XTB

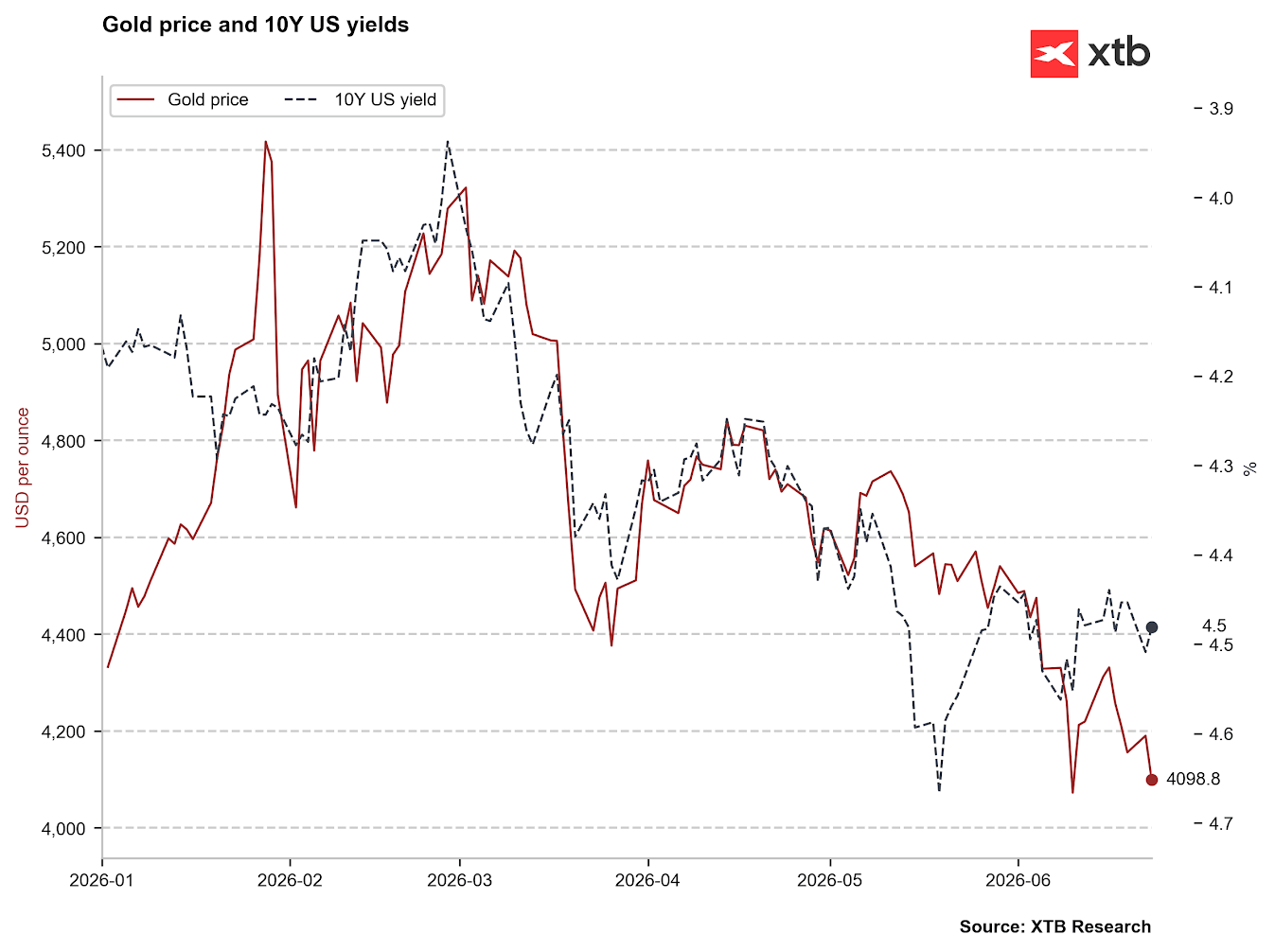

However, gold may be excessively oversold, looking at bond yields, which have fallen from recent highs above 4.6%. Source: Bloomberg Finance LP, XTB

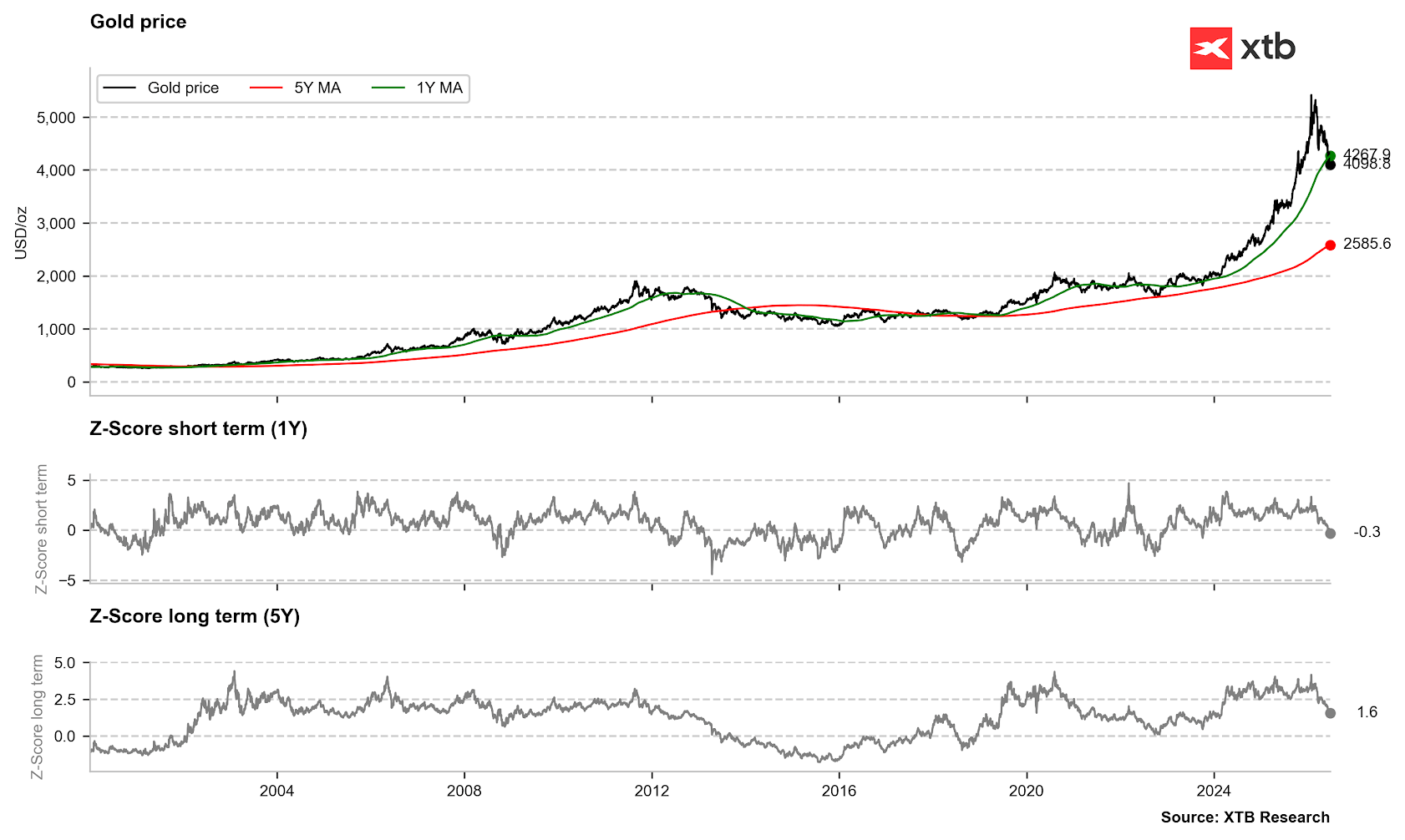

Gold is falling below the 250-session average. Recently, such a situation occurred at the end of 2023. Source: Bloomberg Finance LP, XTB

The gold sell-off is already reaching the area of the 5-year worst price performance. The 5-year average indicates that we should be around a local low. Source: Bloomberg Finance LP Natgas:

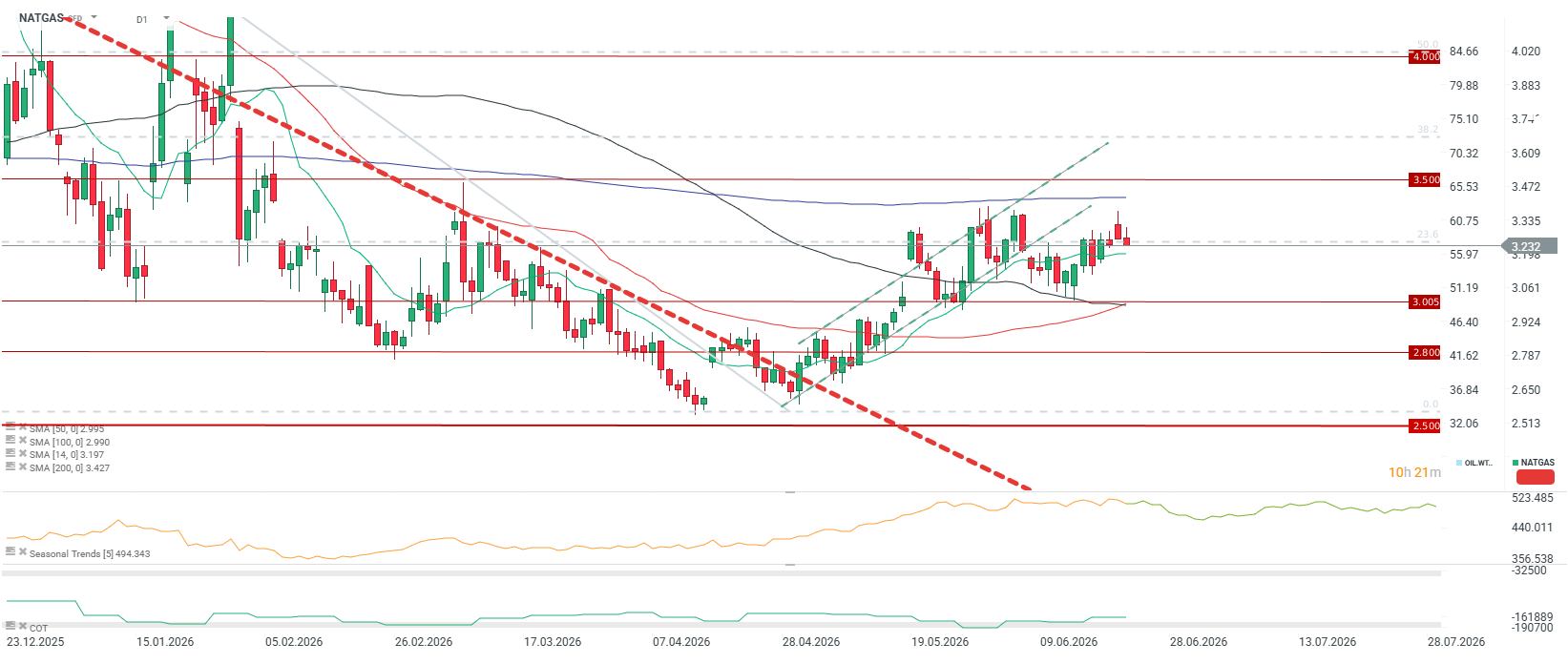

- Strong heat wave in the US: Natural gas contracts on the NYMEX exchange rose above the USD 3.3/MMBTU level, but ultimately closed at 3.26 USD, and currently the price continues to fall below important support, but at the same time staying above the 14-period average.

- Hot forecasts for early July: Weekend models from Commodity Weather Group have tightened significantly. On July 2–6, extreme temperatures will cover most of the US territory, drastically boosting demand for electricity to power air conditioners. Liczba stopniodni chłodniczych rośnie powyżej 5 letniej średniej

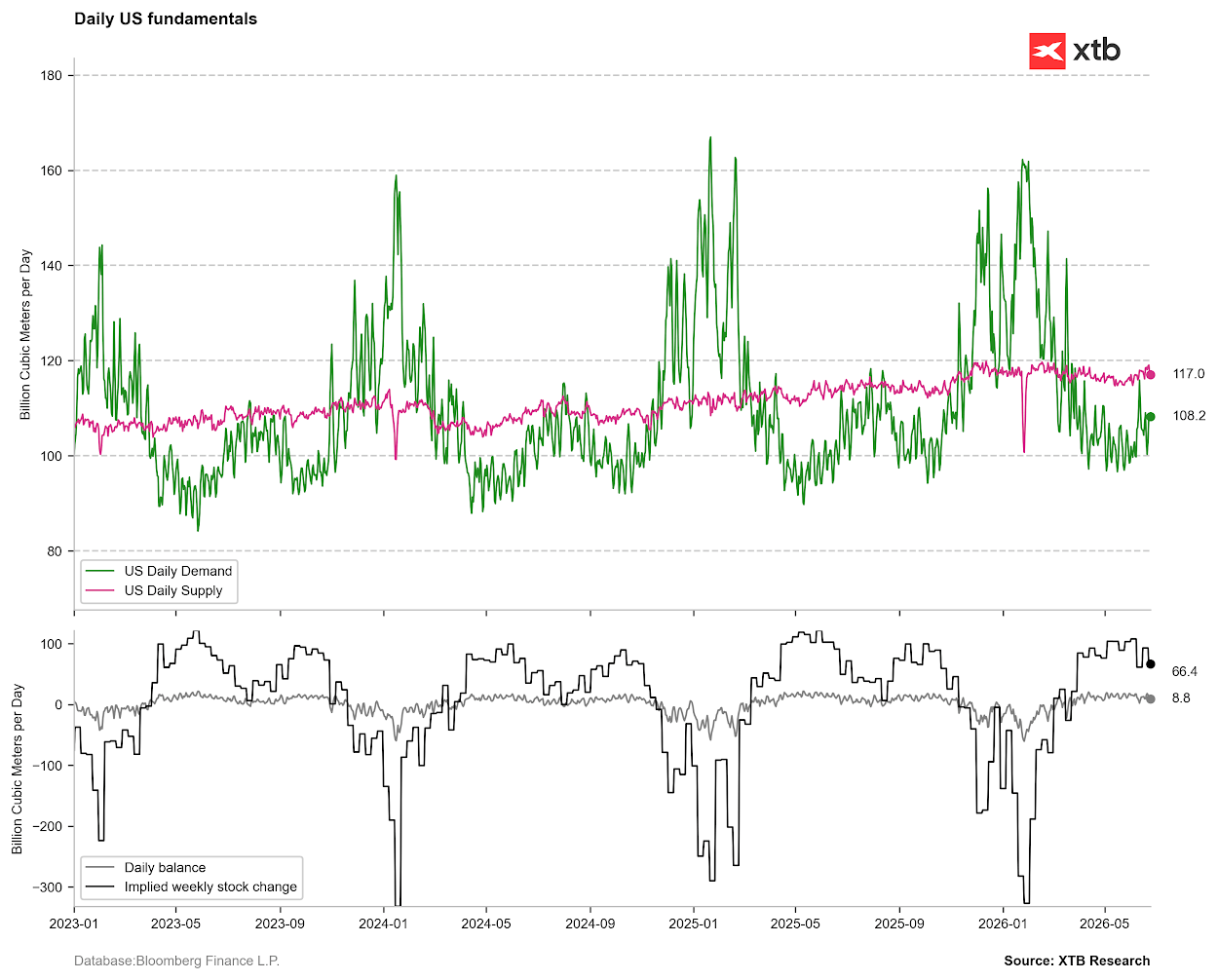

- US LNG exports are accelerating: According to the latest data, domestic dry gas production is approx. 109.6–112.1 bcf/day. At the same time, the flow of raw material to LNG export terminals increased by nearly 1% week-on-week (to the level of 19.2–19.3 bcf/day), depleting domestic stocks.

- Slight pullback in Europe due to geopolitics: European benchmark (Dutch front-month) recorded a cosmetic decline to around 41.85 EUR/MWh. The decline is driven by hope for the resumption of normal supplies through the Strait of Hormuz, which would facilitate Europe (mainly Germany) filling warehouses before winter.

- European heat dome limits declines: Room for further reductions on the old continent is blocked by a giant heat wave. Weather models indicate that Paris may break the June temperature record, reaching 41°C, London will record 36°C, and Madrid will maintain a murderous 39–40°C.

The number of cooling degree days in the US is breaking out above the 5-year range, which changes the demand outlook for the coming days. Source: Bloomberg Finance LP

Gas production is returning to historical highs despite the drop in the number of drilling rigs. Source: Bloomberg Finance LP, XTB

Projected inventory changes are currently slightly lower than a year ago. The upcoming heat wave may cause temporary higher demand than supply. Source: Bloomberg Finance LP, XTB

The price continues to fall despite yesterday’s strong start to the week. A drop below the 14-period average may be negatively perceived by markets, but at the same time a large short-term fundamental change related to the acceleration of demand is preparing. Source: xStation Cocoa:

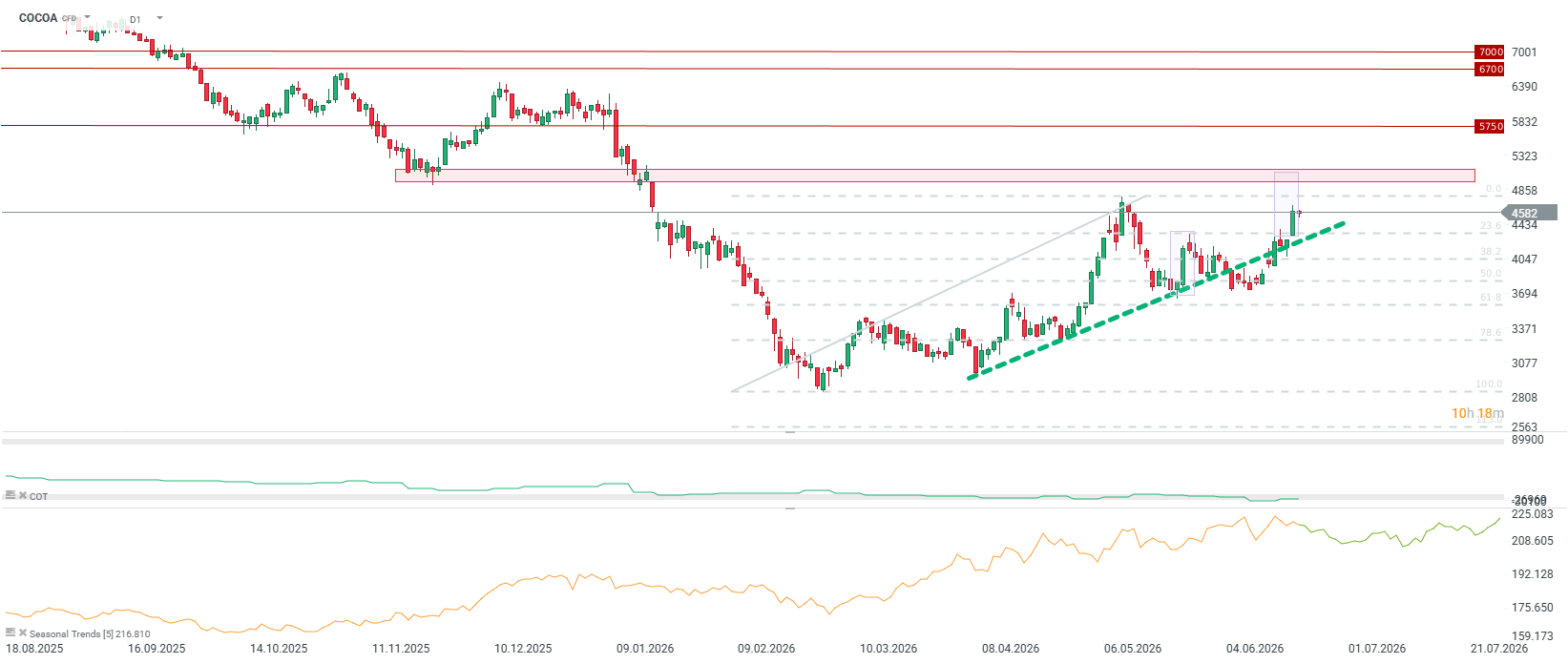

- Jump in prices on markets: Prices rose by nearly 300 dollars per ton, reaching the highest levels since May 12 due to the weather situation in Africa, which may change the outlook for the next season

- Heavy rains paralyze Ivory Coast and Cameroon: Excessive rainfall has led to flooding and complete washout of access roads, cutting off farmers from plantations and blocking the transport of raw materials to ports.

- Humidity drastically increases the risk of spreading a dangerous fungal disease: black pod rot, which destroys trees and dramatically reduces harvest quality. Additionally, in Cameroon, rains wash away expensive and hard-to-access pesticides from trees.

- Mixed picture in Ghana and Nigeria: In contrast, in Ghana, heavy rains accelerate the development of cocoa pods, although farmers struggle with a lack of buyers for the harvested beans. In Nigeria, plantations are reviving, and harvests from new flowers are planned for August and September.

- Nigeria’s restrictive export policy: The Nigerian government has announced a strategic plan to restrict the export of unprocessed, raw cocoa beans. The country intends to follow the path of Ghana and the Ivory Coast, investing in local processing plants to keep the industrial margin within its own economy. In July 2026, a special summit will be held dedicated to building Nigerian cocoa processing brands.

- Zagrożenie długoterminowe (Super El Niño): Meteorologists have confirmed the official formation of the El Niño phenomenon in the Pacific. NOAA szacuje prawdopodobieństwo wystąpienia “Super El Niño” na 67%, co zapowiada drastyczną zmianę pogody w Afryce Zachodniej w kolejnych miesiącach na skrajnie suchą i gorącą, grożąc redukcją przyszłorocznych plonów.

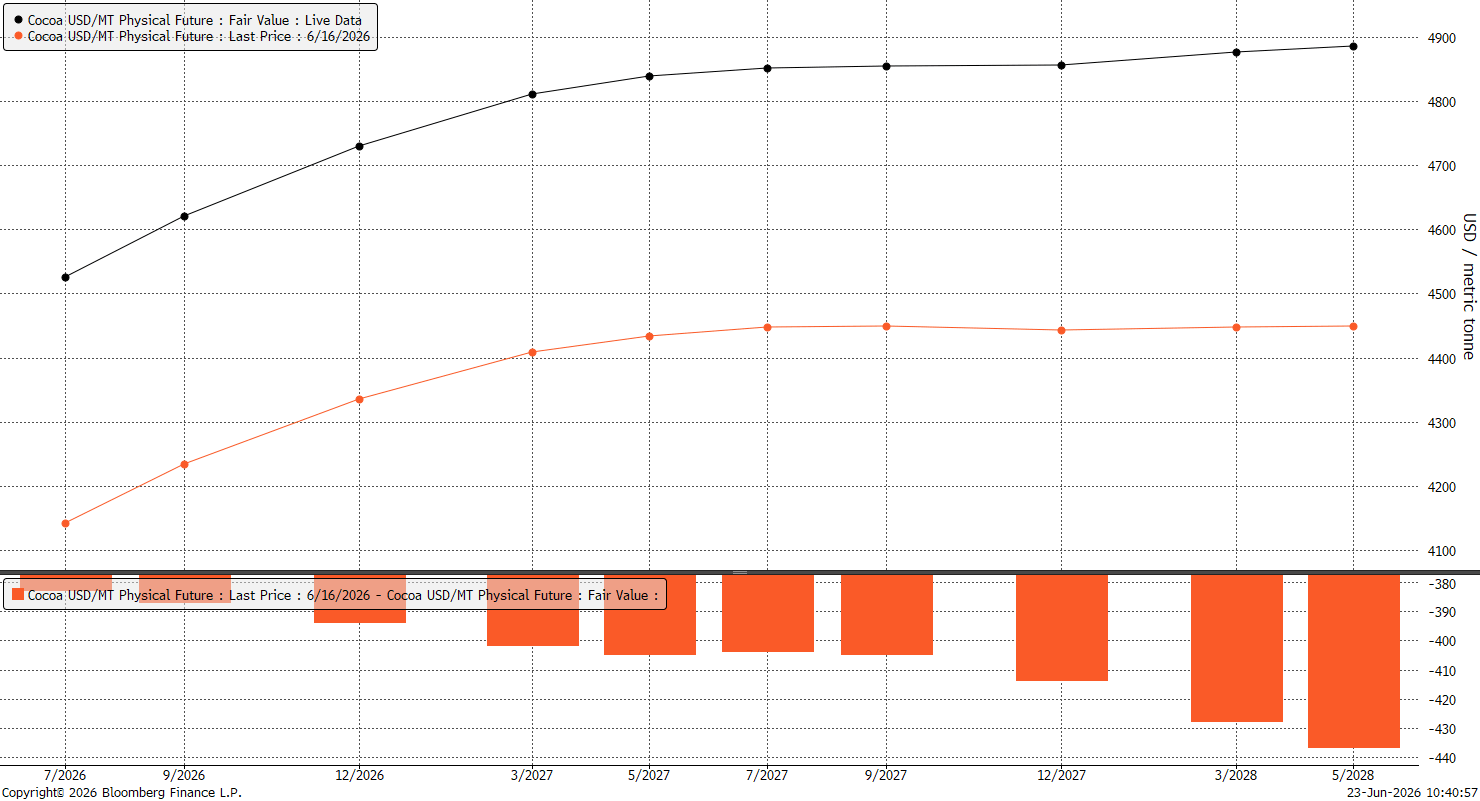

Cocoa prices have clearly risen from the perspective of the last week on the entire futures curve. It is worth emphasizing, however, that the problem is not access to beans now, but potentially in the future. The entire curve remains below the 5000 USD level, although Citi in its latest forecast points to this price level in the perspective of the next 3 months. Source: Bloomberg Finance LP

The price is clearly breaking upwards at the beginning of this week. If concerns about the weather prevail, a breakout to around 5000-5100 USD is possible, where the range resulting from the double bottom and local lows from November is located. Source: xStation5