In the context of SpaceX’s recent IPO and the already announced IPOs of Anthropic and OpenAI, many investors are starting to express concerns about market stability. The emergence of such large, and in many respects speculative, companies could destabilize the market and the indices. The market is already unstable today, and additional price impulses could throw it completely off balance. This association is intuitive – but is it supported by data? There is also the other side of the market, which points to many trends that do not support these fears and cites historical precedents. One such precedent is, quite ironically, the dot-com bubble. Netscape’s 1995 IPO, which in many ways brings to mind Anthropic or OpenAI, was the beginning of the dot-com bubble, not a signal of its bursting.

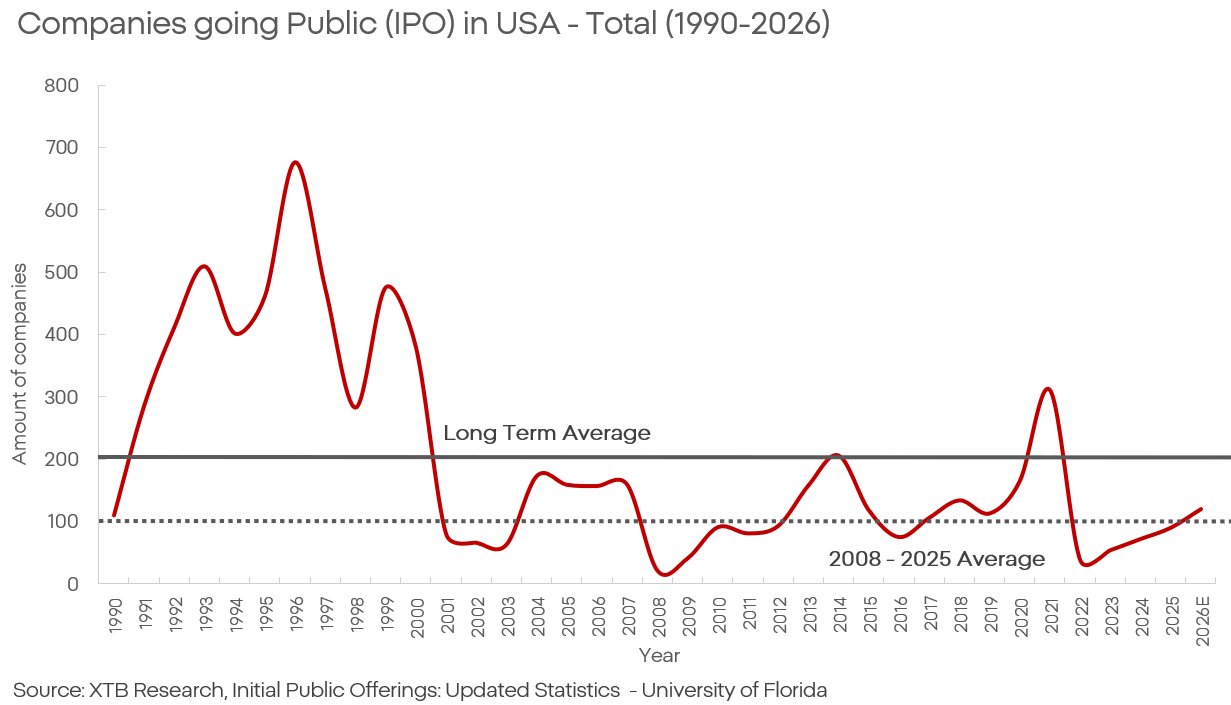

Netscape could boast a breathtaking pace of revenue growth, an enormous market capitalization relative to its business profile and market, and at the same time a lack of profit. The signal of low-quality growth was present from the very beginning; however, it took as long as 5 years for valuations to fall, during which time the NASDAQ rose by about 500% – will we see the same this time? Scale Before we look at the data more closely, it’s worth putting it in context. How large, relative to historical data, will the IPO market be in 2026? Based on the average variant of Goldman Sachs’ forecasts for 2026, IPOs in the U.S. are approximately:

- 120 new companies

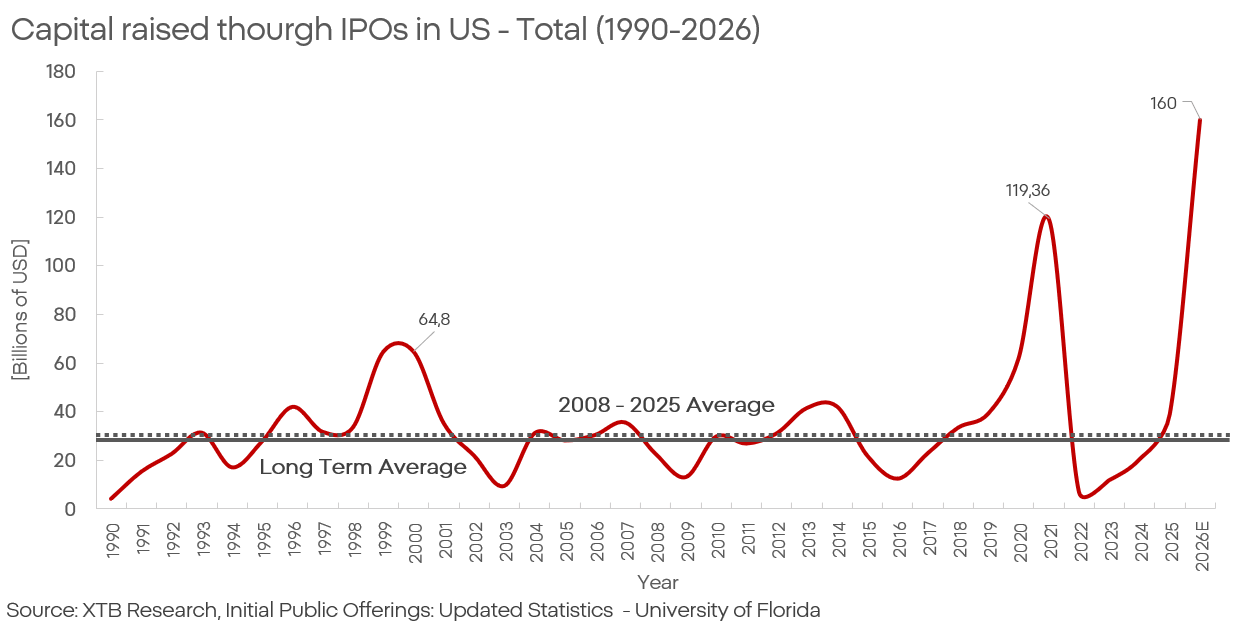

- USD 160 billion in volume (the total amount raised in offerings at the issue price)

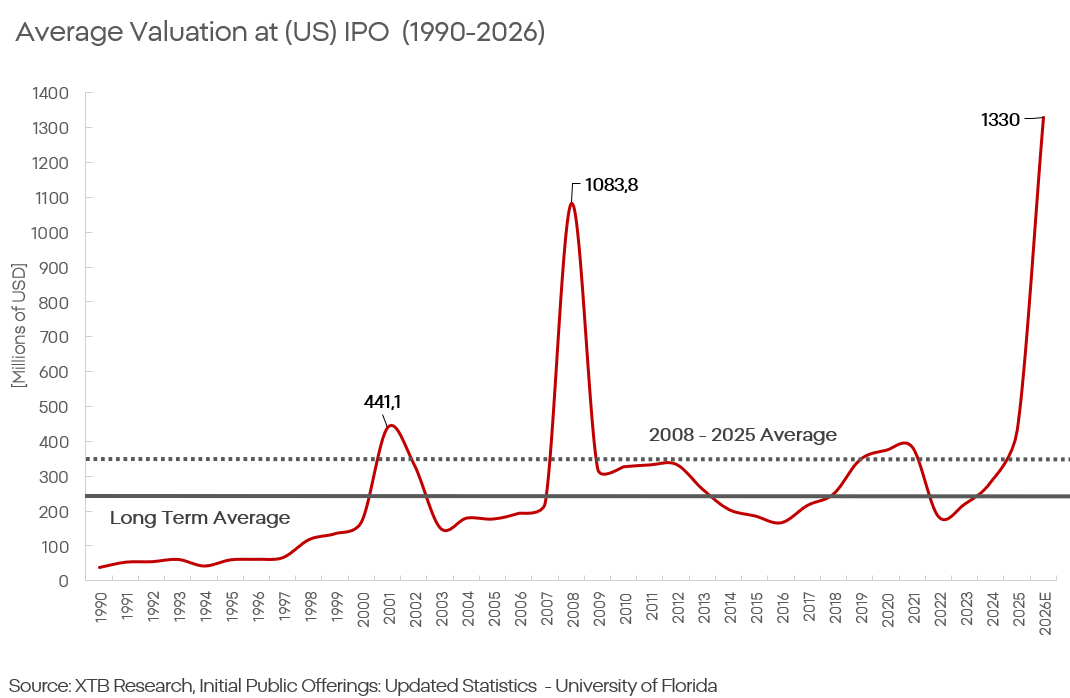

- with an average IPO company valuation of USD 1.3 billion

Many analysts already claim the scale is unprecedented. On the other hand, it’s worth looking at specific statistics to examine whether we are indeed facing the biggest IPO frenzy in years.

In terms of the number of IPOs, activity barely stays above the 2008–2025 average and is clearly below the average of the last 35 years. However, the trend looks completely different in terms of offer size.

IPO size by volume is expected to set an absolute record in nominal terms. At the same time, we must take inflation into account. The same dollar is worth much less now than in 2000 or even 2020.

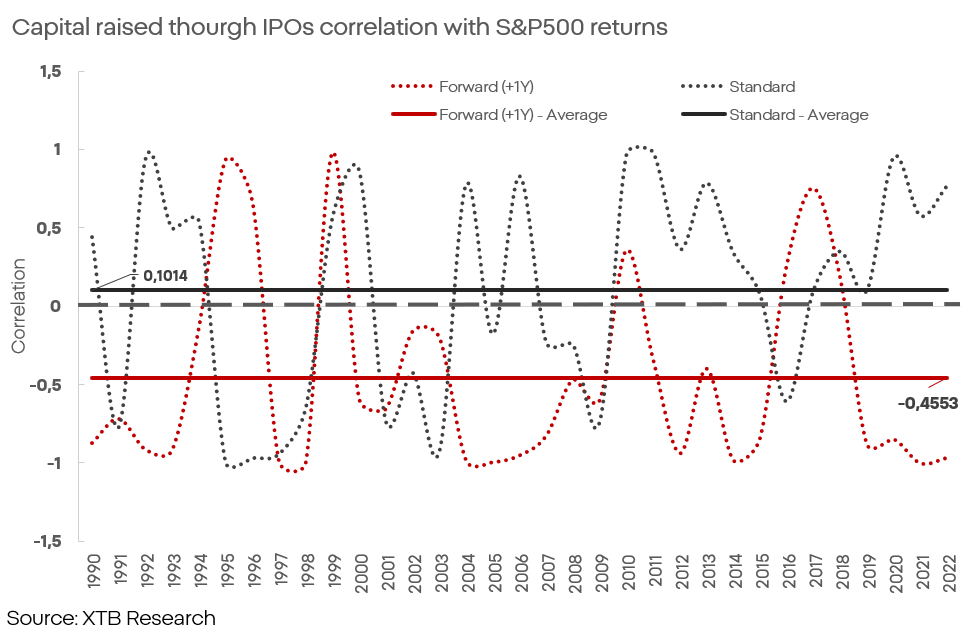

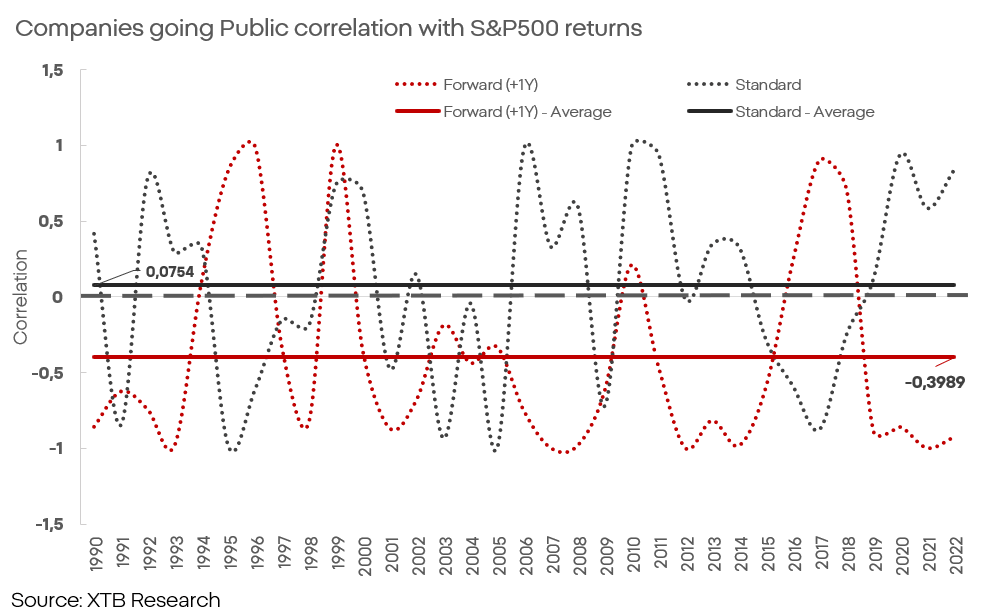

Both the total amount raised and the average valuation show not only that 2026 is expected to be an absolute record year, but even a superficial look at the chart and its dates reveals huge jumps above the average during periods historically described as turbulent for markets. Does this mean that enormous IPOs (like those expected this year) are a clear signal of an irrational market? By analyzing the correlation between returns on indices (S&P 500), we can reach an interesting conclusion. Based on data provided by Jay R. Ritter and Eugene F. Brigham of the University of Florida, we can observe that: An increase in IPO activity has an almost negligible correlation with increases or decreases in index returns over the last 35 years. On the other hand, if we modify the approach and start calculating correlations with a lead (i.e., forward-looking), the relationship becomes clearly visible across all analyzed statistical regimes.

This means that IPOs do not so much correlate with declines in indices, but one could argue they are a leading indicator of periods of weaker index returns. At the moment when the IPO market shows the largest increase in the period studied, it implies a serious correction over a horizon of about a year.

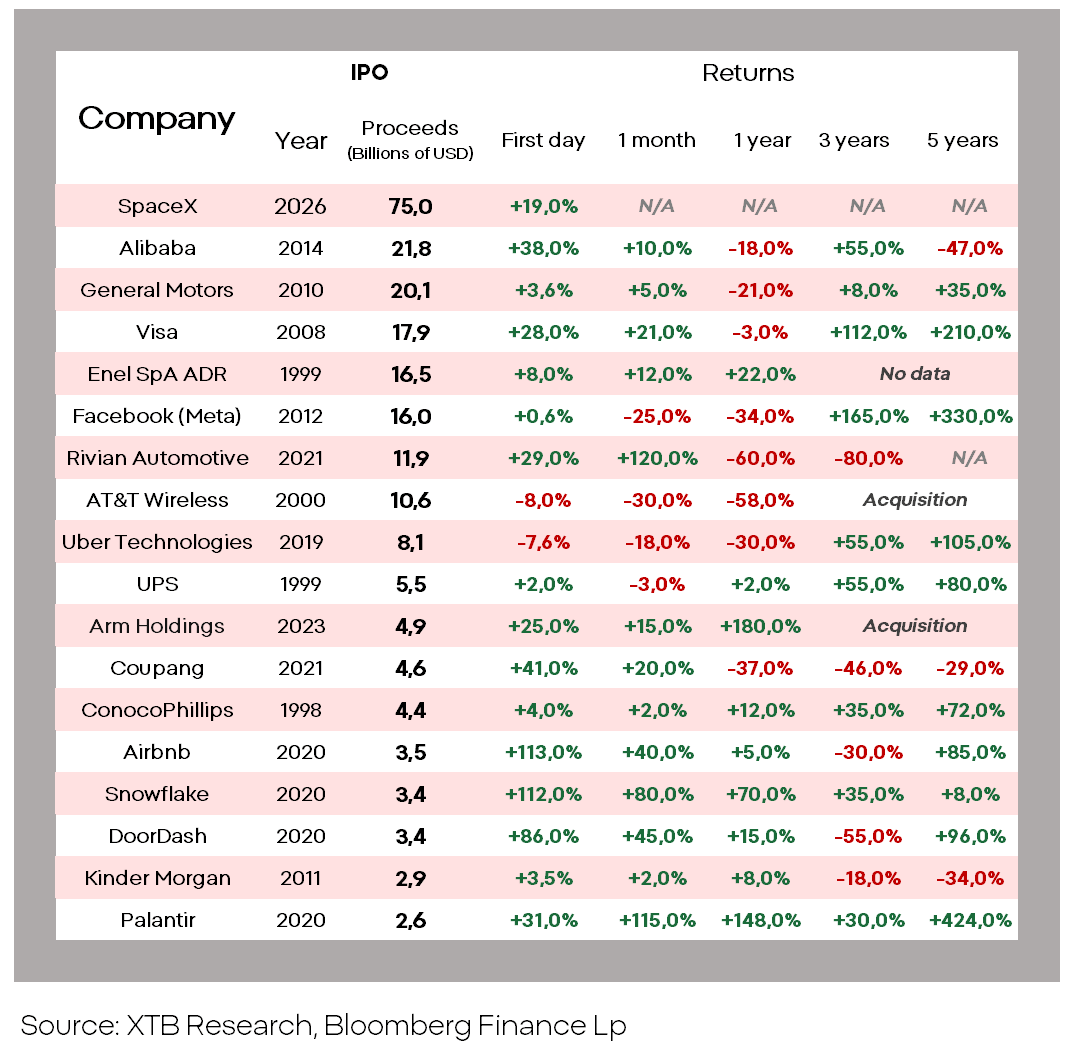

Analyzing the largest U.S. IPOs from recent decades, one can observe that valuation declines on the first day of trading almost never happen, and double-digit increases are more common; sentiment remains clearly positive during the first month of trading. The proportions reverse only after about a year, when most companies suffer significant declines. In the analyzed set, out of 18 companies only 4 avoided major losses over a 1–5 year horizon and at the same time remained public.

Why does this happen?

A large increase in the number of IPOs is a valuable signal of the market cycle. A company deciding to go public – regardless of whether its goal is to provide an exit opportunity for early shareholders or to raise capital for growth – will strive to do so in a market environment that supports the highest possible valuations. The “exit from the investment” angle is particularly important here. If a private company built by venture capital enters the public market, it does so primarily so that the original investors can liquidate their stakes at the highest possible price. And if those investors decide to cash out, they probably do not expect the shares to continue rising in value. Research provided by the aforementioned analysts, Ritter and Brigham, clearly shows the assumptions and consequences of this strategy:

- The average return 3 years after IPO for VC-backed companies is -15%, versus about -1% for companies seeking growth capital.

- Even more interestingly, on the first trading day VC-backed companies post a return of about 28%, versus only 15% for growth-capital companies.

What does this mean in the context of OpenAI and Anthropic IPOs?

Like SpaceX, OpenAI and Anthropic cannot by any means be described as companies seeking growth capital in the public market. These are entities valued at enormous sums that grew to their current size by financing themselves with private capital. If these companies intend to conduct an IPO – as we already know from SEC publications (though without details yet) – it means that:

- private-market capital has been exhausted or is unwilling to continue financing the entity’s investments;

or/and

- the company’s owners may be expecting the peak of the market cycle and are looking for “exit liquidity” for their investments. It is also worth noting that private equity (PE) firms have lock-up periods after which they are obliged to liquidate investments to pay money back to investors. This is significant in light of increased activity from such entities.

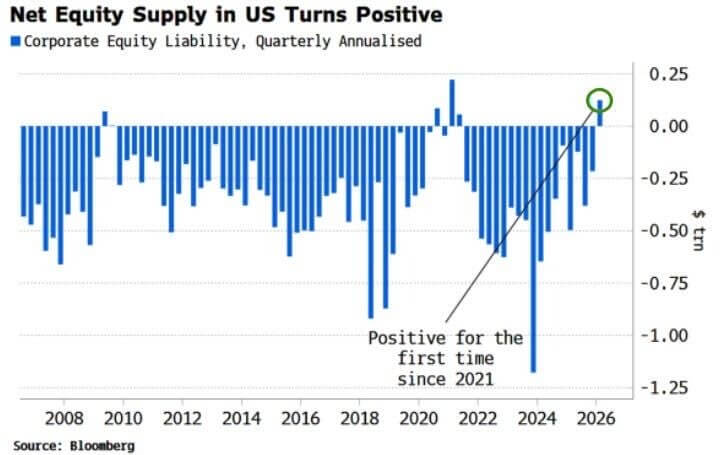

Source: Bloomberg Finance Lp. Given the coincidence of large IPOs and a significant drop in buybacks, this means net supply in the market will rise. If net supply rises, the price falls – this relationship is so basic it is hard to argue with. As the data show, periods of heightened activity in the IPO market signal approaching valuation peaks. By analyzing historical trends and precedents, one can conclude that:

- SpaceX filed for a confidential IPO on April 1; after 49 days their S-1 document was published, and 23 days later trading began. That gives 72 days from the start of the regulatory process to the public debut – an extremely fast pace for a company of that size. Rounding up, under more conservative assumptions one could expect Anthropic and OpenAI IPOs within about 90 days from filing a confidential submission to the SEC. This means these companies could enter the market as early as around September this year.

- At the same time, SpaceX’s investor lock-up period is approximately 180 days from going public. This means SpaceX’s original investors could begin exiting between September and December.

- Meanwhile, historical data indicate that during periods of major IPOs, valuations almost universally rise (regardless of whether there is a good reason). In this situation, if an extended correction were to occur, it would be reasonable to expect it at the earliest at the end of 2026 or the beginning of 2027. Before that happens, one can expect rises in average valuations.