Is this the end of Cocoa-geddon? Real recovery or weather speculation?

Key takeaways

- Weather and Geopolitical Risks: The return of El Niño and the blockade of the Strait of Hormuz (impacting fertilizer prices) could wipe out the current surplus and trigger another production crisis.

- Questionable Short Squeeze: While media outlets report a short squeeze, exchange data does not confirm mass panic among speculators, suggesting the rally is driven more by technicals and fear.

- Producer Crisis: Drastic farmgate price cuts in Africa (up to 57%) and falling cocoa grindings in Europe indicate a deep decoupling between production costs and actual consumer demand.

The cocoa market is most likely at another stage of change. The years 2022–2024 brought a massive rally related to cocoa shortages, followed by a sharp price retreat linked to demand destruction and an improved supply-side situation. Since the end of April, cocoa prices have already rebounded by more than a third, and some analyses indicate that this may only be a pit stop before a stronger recovery toward $6,000–$7,000. The rebound at the beginning of the second week of May is being linked to a so-called “short squeeze.” Are we actually dealing with such a situation, and can we count on a truly long-term price recovery?

Fundamental Balance: From deep deficit to cautious oversupply

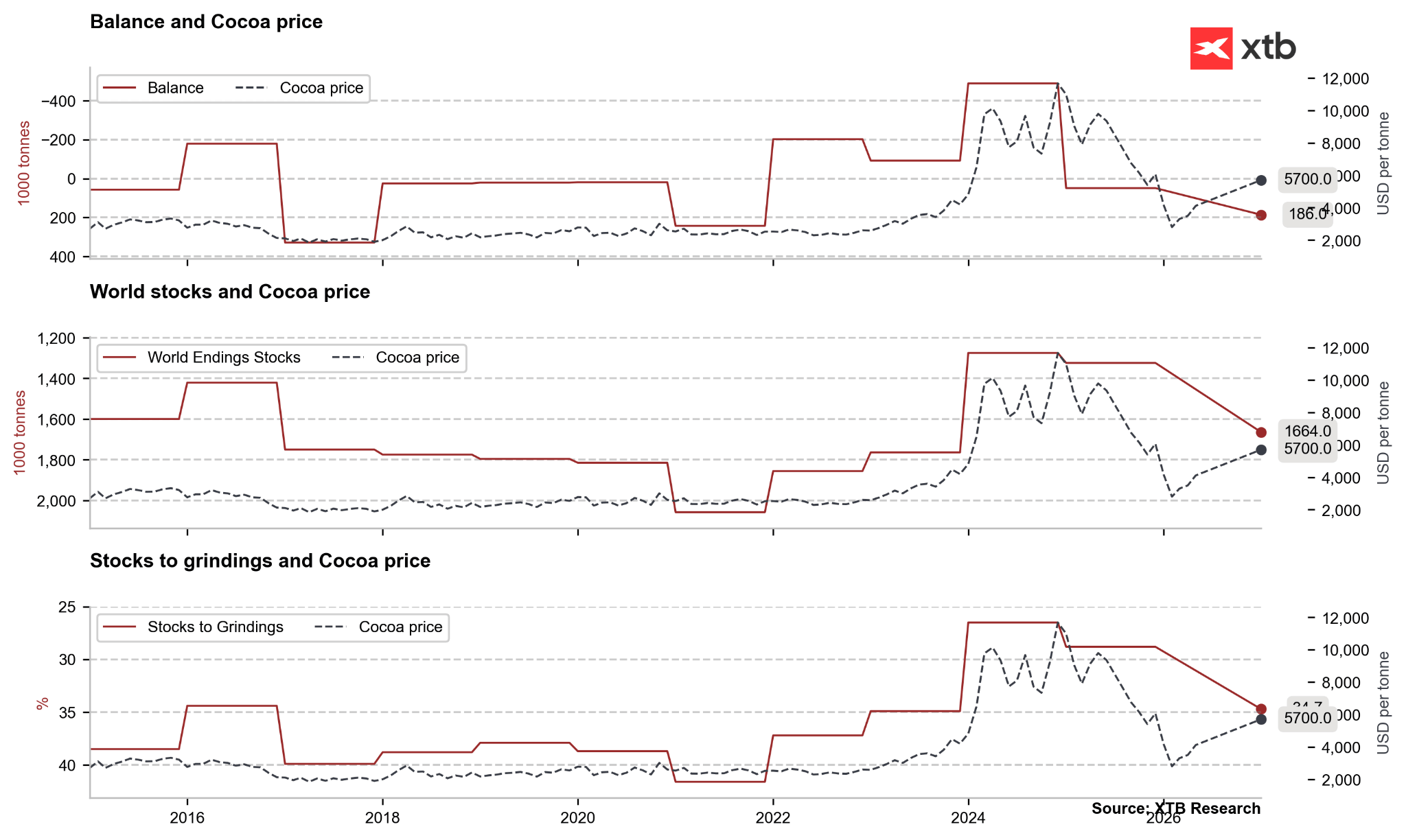

The most drastic deficits in history, which amounted to nearly 500,000 tons in the 2023/24 season. According to adjusted data from the International Cocoa Organization (ICCO) from February 2026, the 2024/25 season brought the first surplus in four years at a level of 75,000 tons, which represented a significant upward revision compared to earlier forecasts. This improvement was possible thanks to the regeneration of crops in West Africa after catastrophic weather events and plant diseases (such as swollen shoot and black pod) that decimated plantations in previous years. Analysis of forecasts for the upcoming seasons, however, shows a wide range of estimates, which heightens investment uncertainty. While StoneX forecasts a surplus of 247,000 tons in the 2025/26 season, Rabobank has cut its expectations to 250,000 tons (from a previous 328,000), citing climate risks and structural problems in supply chains.

Fundamental data in the cocoa market is quite significantly delayed, but at the same time, it is worth emphasizing that we have been dealing with oversupply for two seasons, and additionally, the 2026/2027 season should bring another advantage of supply over demand. Source: Bloomberg Finance LP, XTB

Speculative rebound? Is there actually a short squeeze in the market?

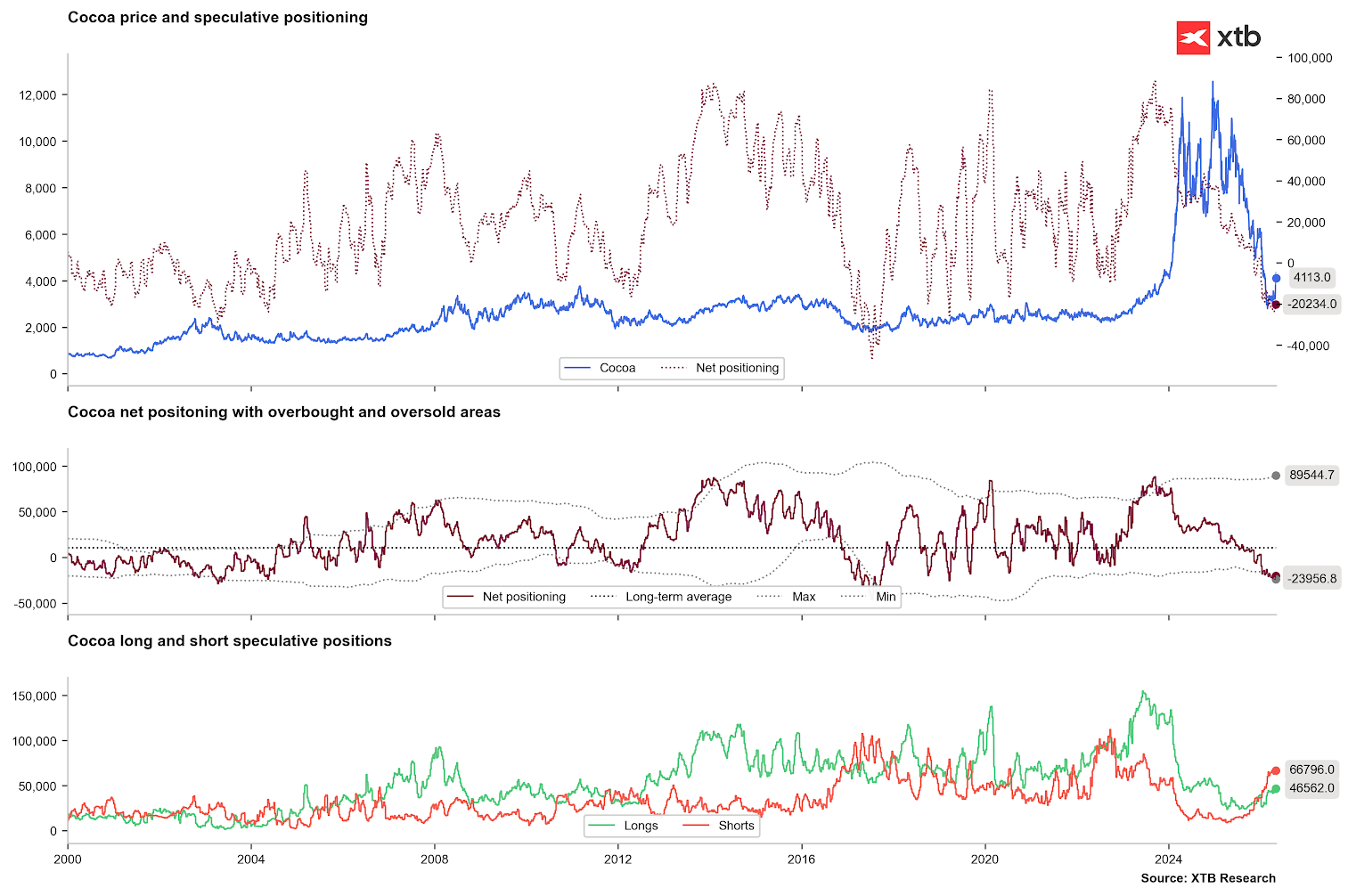

The dominant factor driving the sharp price increase in May 2026 is not fundamental changes in current supply, but rather the specific positioning of speculative capital. Parkman from Marex, quoted in a recent Wall Street Journal article, argues that the upward movement in the cocoa market over the last dozen or so days has almost nothing to do with fundamentals, but is “categorically” the result of a technical squeeze of short positions. Managed Money funds have aggressively bet on further cocoa price declines in recent months, reacting to signals of growing oversupply.

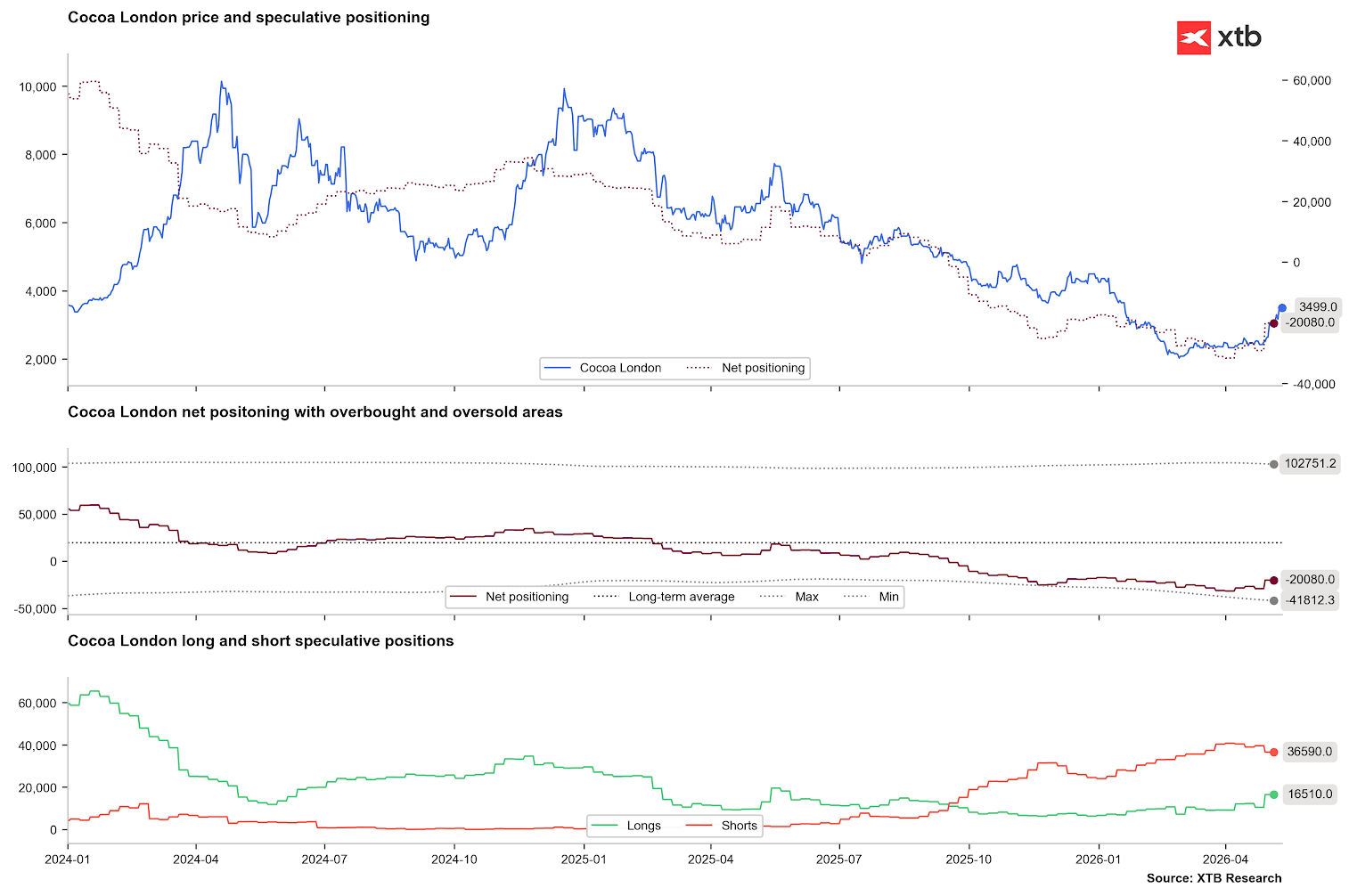

At the moment when the first worrying weather signals appeared from Ivory Coast, these funds could theoretically be forced to panic-buy contracts to close losing positions, which would trigger a domino effect and push prices even higher. However, it is worth noting that net short positions among speculators are actually low, both in the London and New York markets, and we are not observing a panic closing of short positions. Short positions fell slightly in London, but in New York, they even increased. On the other hand, it should be noted that after a significant drop in open interest after 2023, price changes in the cocoa market have become extreme.

Net positions have fallen to an extremely low level, although not as low as in 2018. Source: Bloomberg Finance LP, XTB

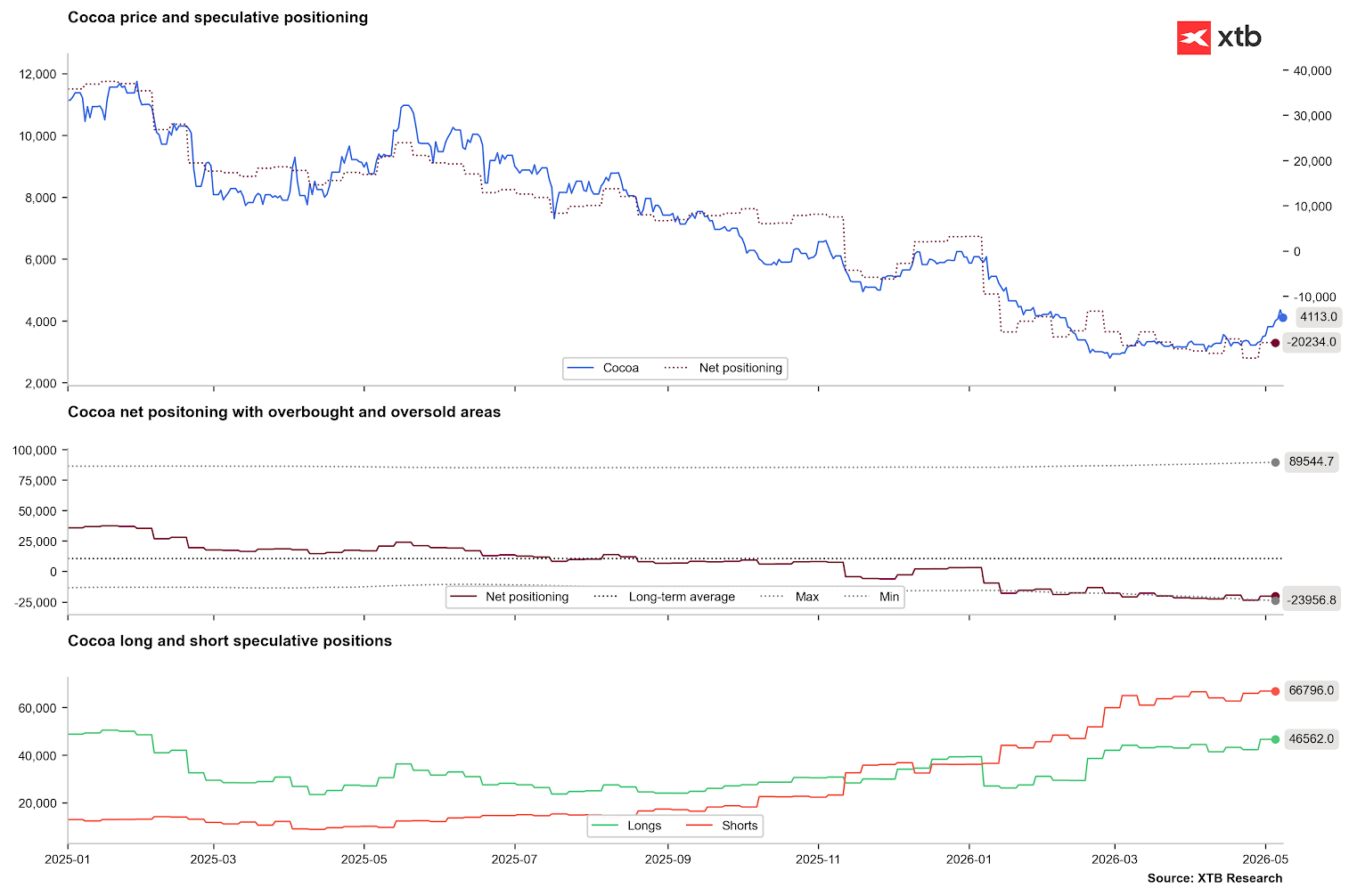

Looking from 2025, a strong acceleration of the selling side was visible first from September 2025, and then from January 2026. In the last week, long positions rebounded slightly. Source: Bloomberg Finance LP, XTB

Short covering may be visible in the London market. On one hand, short positions are being closed, and on the other, long positions are being opened. At the same time, these are not very large changes. Source: Bloomberg Finance LP, XTB

Climate threats as a flashpoint: El Niño and drought in West Africa

It is difficult to pinpoint whether these small changes on the part of speculators led to such a large increase, but it is worth emphasizing that the initial spark was the deteriorating weather forecasts for key growing regions.

The U.S. National Oceanic and Atmospheric Administration (NOAA) estimated the probability of an El Niño event in the second half of 2026 at 61%, with a significant chance of a “Super El Niño” scenario. Historically, El Niño brings warmer and drier conditions to West Africa, which directly hits the formation of cocoa pods and degrades the yields of the main season, which takes place from October to April. The current weather situation in Ivory Coast partially confirms these concerns. In the regions of Soubre, Daloa, and Agboville, farmers are reporting rainfall drastically below the five-year average. On the other hand, cocoa deliveries during the so-called mid-season were at a fairly high level, while the problem for producing countries was actually the sale of the beans.

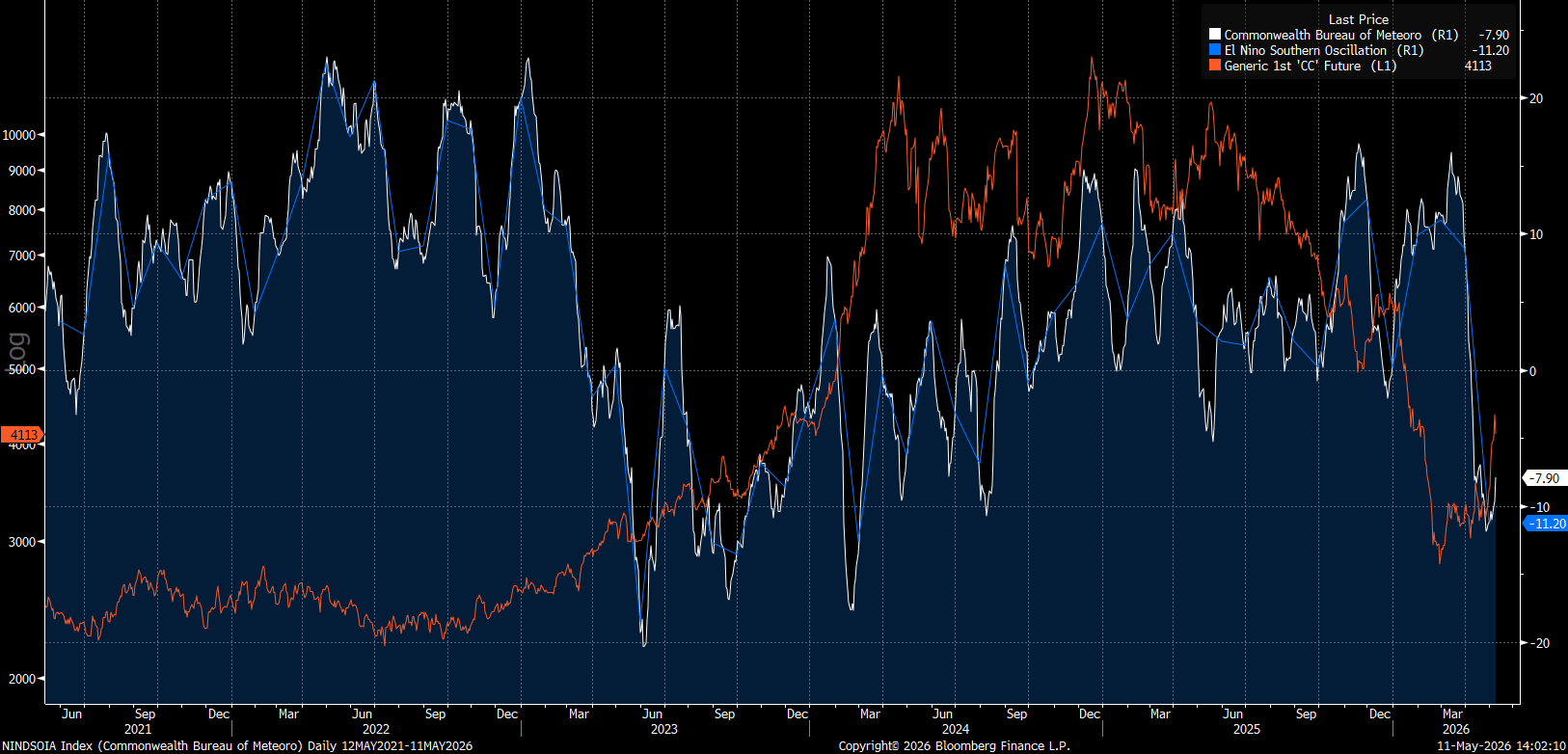

Although El Niño is of great importance for the weather in Africa, it is difficult to find a significant correlation between the El Niño oscillator and price changes. At this moment, the oscillator still indicates a La Niña phenomenon. Source: Bloomberg Finance LP

Geopolitical crisis and its impact on production costs: The Strait of Hormuz

An unexpected pro-growth factor in 2026 has become the escalation of the conflict in the Middle East, which led to the closure of the Strait of Hormuz as part of the “Epic Fury” operation. Although this region is not a direct producer of cocoa, its importance for the agricultural commodities market is critical due to the export of fertilizer components. The blockade of Hormuz caused the following repercussions:

- Fertilizer shock: The Middle East accounts for nearly 20% of global marine fertilizer exports, including as much as 46% of the urea trade. A similar crisis in 2022 initiated production problems in the cocoa market in 2023 and 2024. Urea futures contracts have already exceeded $800 per ton and approached 2022 levels.

- Raw material shortages: The interruption of sulfur supplies, a byproduct of oil refining in the Gulf region, hit the production of sulfuric acid and phosphate fertilizers, whose prices also rose to levels of $700–$800 USD per ton.

- Logistical costs: The closure of a key route forced the re-routing of ships, which raised freight rates, fuel costs, and insurance, directly increasing the cost of importing beans for processors in Europe and North America.

For farmers in West Africa, this means lower availability and higher prices for production inputs at a critical moment in the vegetation cycle. The lack of proper fertilization combined with drought could permanently lower the production potential of cocoa trees for the years 2026–2027.

Demand destruction and consumption barriers

While the supply side struggles with external shocks, the demand side is still feeling the effects of “chocolate dearness.” Cocoa processing (grindings) in Europe fell in the fourth quarter of 2025 by as much as 8.3% year-on-year, which was a significantly worse result than market expectations (-2.9%). In the first quarter of 2026, this decline continued at a level of 7.8%, which is the lowest result for this period in 17 years. It is worth noting that cocoa stocks continue to grow. At this point, we are not dealing with a change in fundamentals, but only with fears of a renewed deterioration of the supply situation. Potentially, we should see an improvement on the demand side in the second half of this year, although a return of prices to the $6,000–$7,000 range may once again lead to a reduction in buying pressure.

Drastic price cuts for farmers:

A threat to sector stability

In response to the fall in world prices at the turn of 2025 and 2026, the governments of Ghana and Ivory Coast made controversial decisions to reduce the farmgate prices paid to farmers. Ghana reduced the price by 28.6%, while Ivory Coast announced a reduction of as much as 57% for the mid-season. These decisions, while economically justified from the perspective of regulators (such as COCOBOD), strike at the foundations of the existence of over 800,000 households.

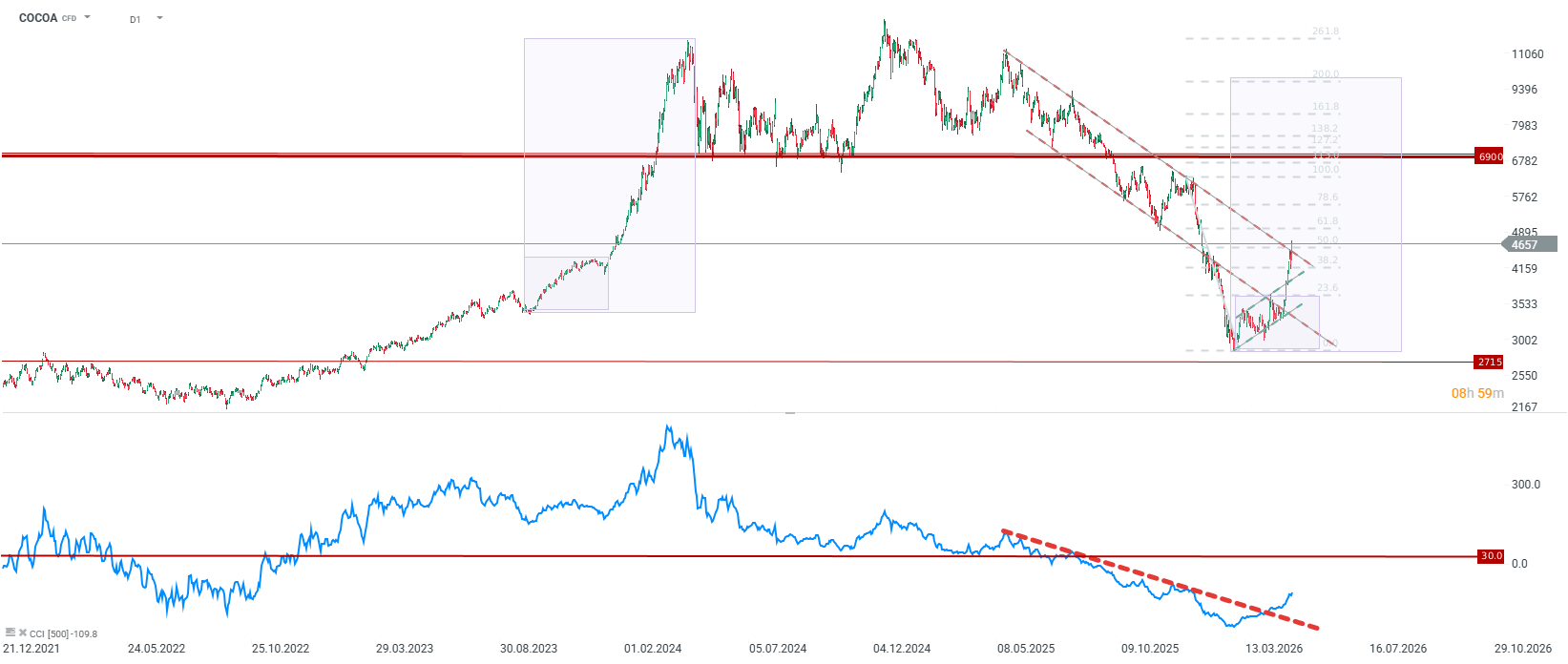

Technical analysis and price perspectives: The “New Normal”

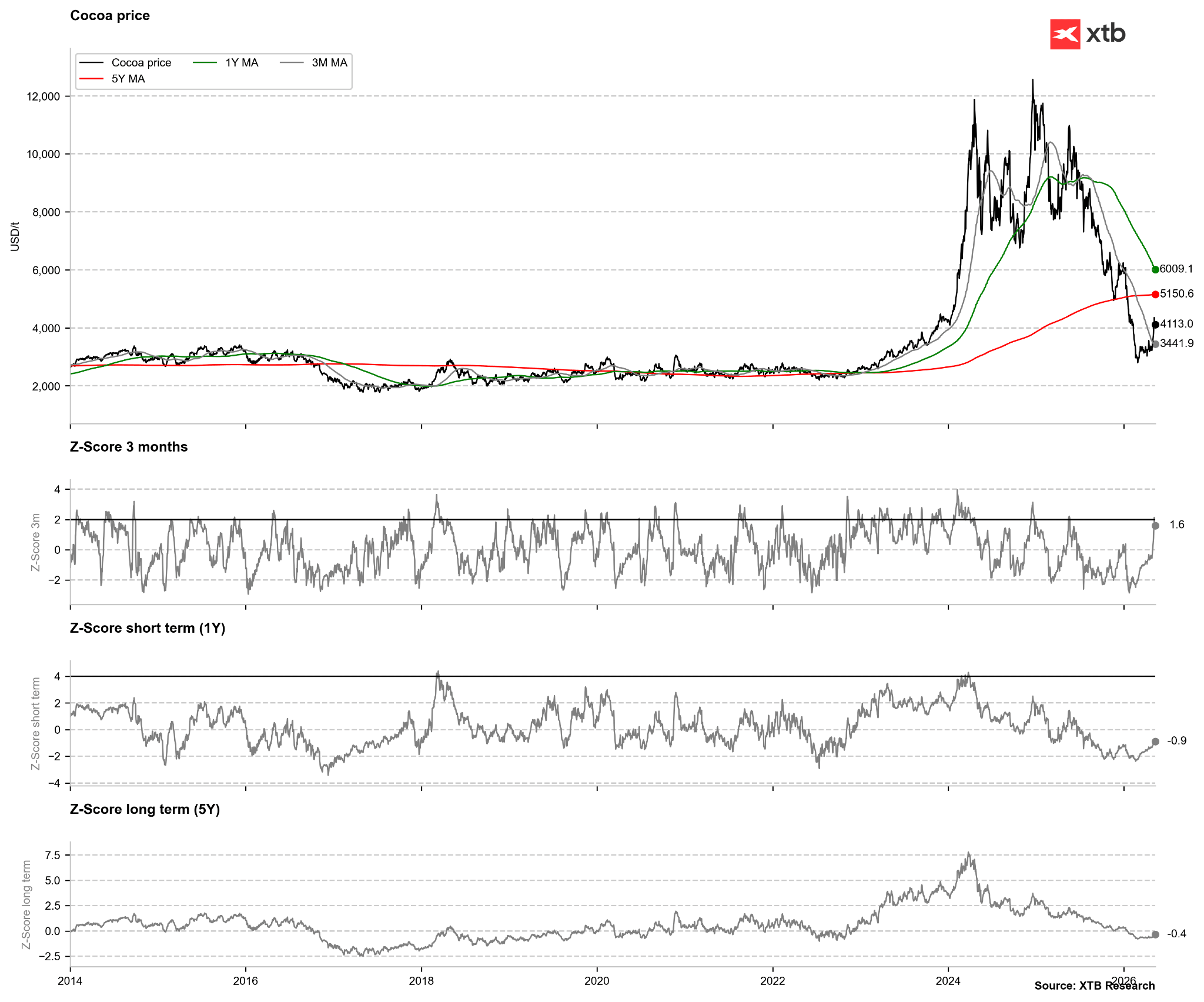

From a technical point of view, the cocoa market in May 2026 shows signs of forming a permanent bottom. After a 75% drop from the peaks, quotations entered a phase of returning to the averages. Interestingly, the deviation from the 3-month average actually gave an oversold signal at the beginning of this year, similar to the deviation from the 1-year average. On the other hand, the deviation from the 3-month average has returned to indicating overbought, though not yet sharply. The deviation from the 5-year average basically generates no strong signals. Source: Bloomberg Finance LP, XTB

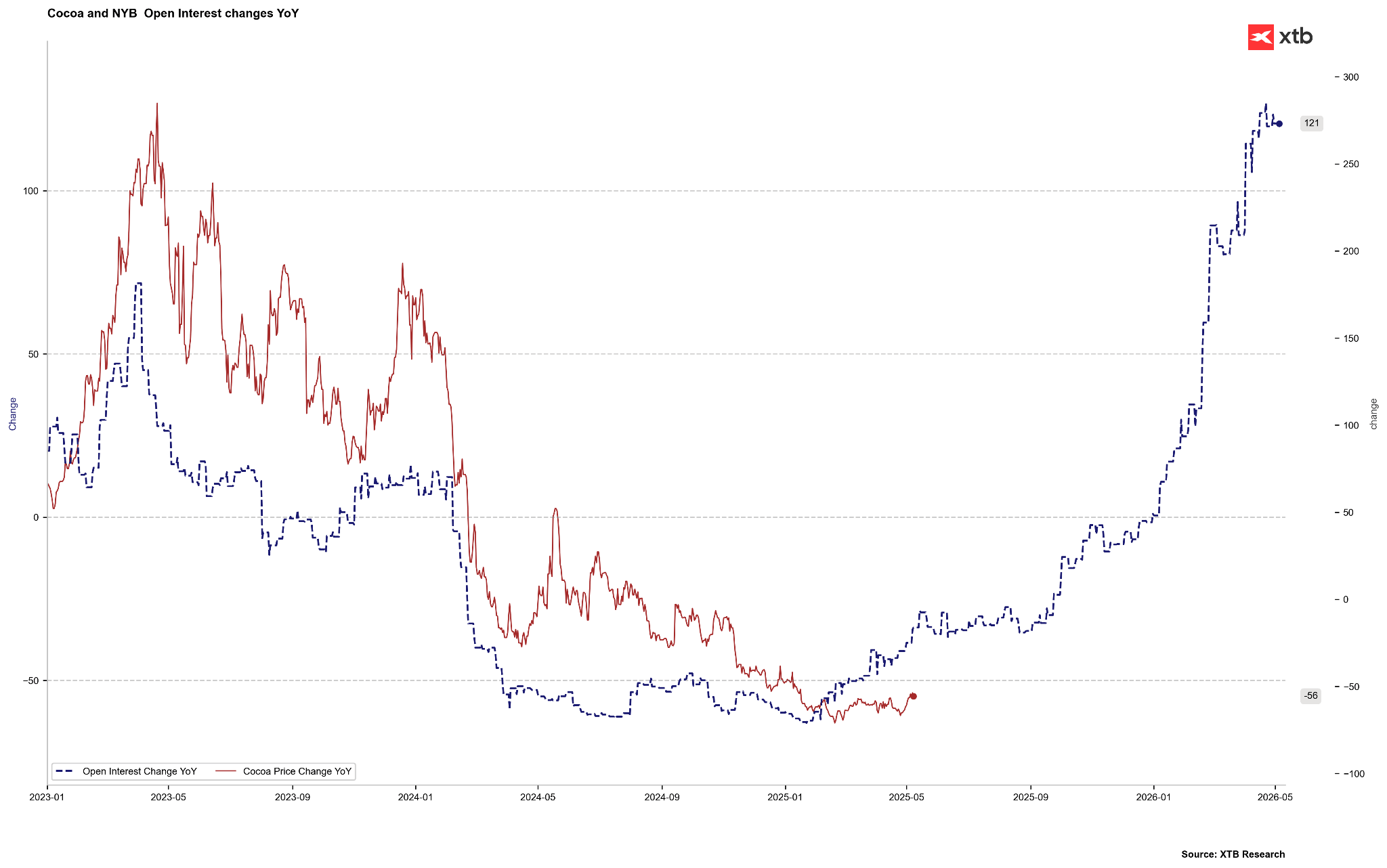

Since 2023, a correlation can be observed between the year-on-year price change and the year-on-year change for open interest, which is shifted forward by one year. Although these are far-reaching assumptions, further following this indicator could suggest a zero annual price change around September, which would give us a price in the vicinity of $6,000–$7,000 USD per ton. Source: Bloomberg Finance LP

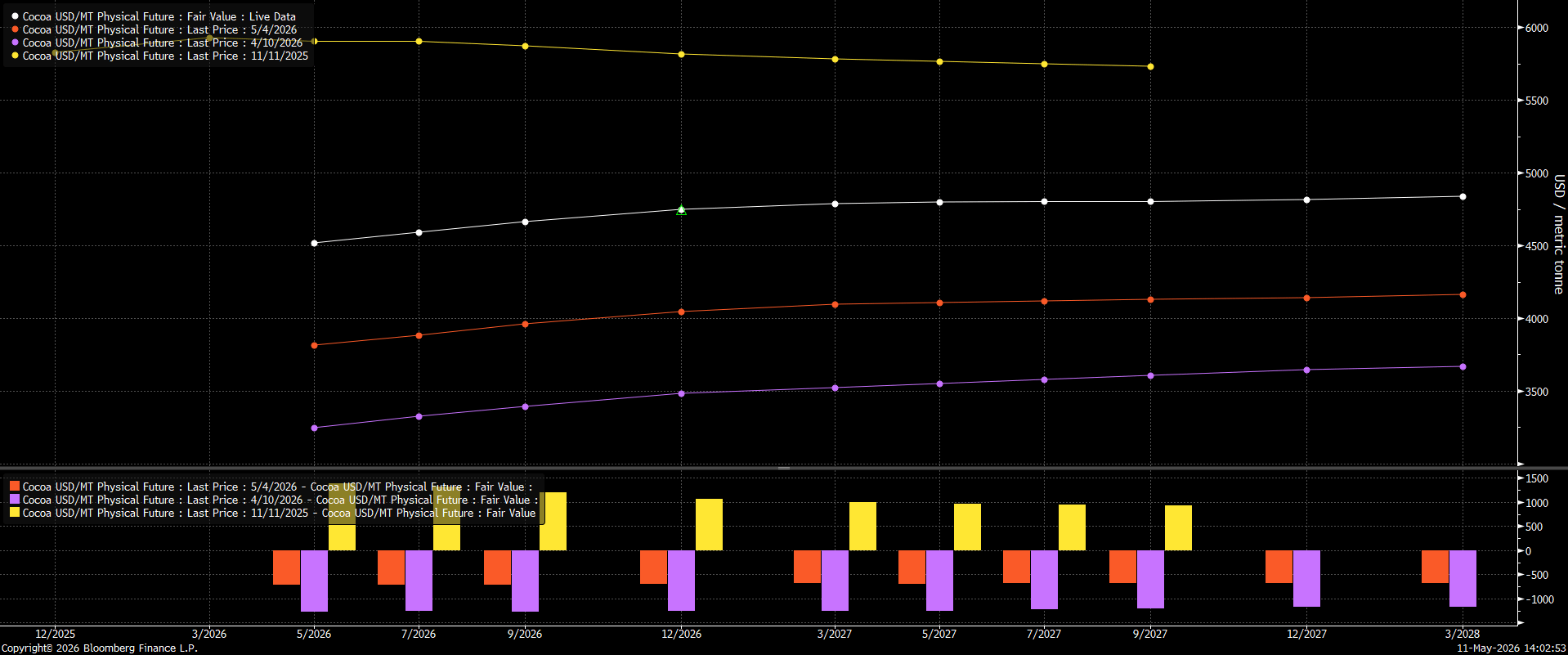

It is worth noting, however, that the forward curves are not changing significantly in terms of shape, and the movements are taking place across the entire curve. The market remains in a slight contango, and we are not observing major movements in calendar spreads. Source: Bloomberg Finance LP

Summary and conclusions: Is this the end of low prices?

The current situation in the cocoa market suggests that the phase of the lowest prices in this cycle was likely reached in the first quarter of 2026. Although the projected supply surplus in the 2024/25 and 2025/26 seasons should theoretically favor the bears, a number of factors are beginning to indicate that the worst is already behind us. On the other hand, the current rebound may seem premature and is based on weather speculation rather than real changes in fundamentals. It is worth noting that we are not observing the “short squeeze” being announced by the media. However, if the price breaks the $4,900–$5,000 level, we may again deal with a change in the perception of the fundamental situation in the cocoa market, similar to what happened in 2024.

The price rose by over 10% today, which has happened extremely rarely in this market recently. Bearish candles from the two previous sessions were negated. Currently, an important technical spot is being tested in the form of the 50.0 retracement of the last large downward impulse and the upper limit of the downward trend channel. A close above will open the way to testing the vicinity of $5,000, which is currently a key resistance related to the 61.8 retracement and local resistance linked to the local lows of November 2025.