Key takeaways

- European earnings boost from energy sector

- How long can energy prop up earnings growth?

- Analysts upbeat ahead of US earnings season

- The US: a victim of its own success

- The test for tech: can it continue to prop up US earnings growth?

- The US holds the upper hand for now

- The stock market outlook

Earnings preview: can Europe narrow the gap with the US? Europe is poised for another strong quarter of earnings growth. After posting its strongest quarter of earnings growth for 3 years in Q1, analysts are expecting big things for Q2. Earnings growth is poised to grow by 12% year-on-year, suggesting that upward momentum for earnings will be maintained. Some analysts also think that there is the potential for an upside surprise, since earnings expectations have been revised higher in recent weeks.

European earnings boost from energy sector

Expectations are also high as we move into this reporting season. Digging a bit deeper, growth is expected to be dominated by monster revenues and profits for the oil and gas majors where earnings growth is expected to rise by 84% YoY. If you exclude this sector, then earnings growth in Europe is a much more modest 3%. Energy is Europe’s version of tech, and it is likely to dominate this reporting season. Aside from energy, the chemicals and industrials sectors are expected to report solid earnings growth, along with Europe’s banking sector. There may also be strong results from Europe’s tech sector, which is closely linked to the AI trade. However, consumer-facing sectors are expected to remain under pressure, with autos and consumer discretionary stocks unlikely to keep pace with earnings growth elsewhere.

How long can energy prop up earnings growth?

The question is, can energy earnings continue to prop up the European markets, and is this the high point for earnings growth? Earnings from the energy sector are highly sensitive to events in the Middle East, and although the Brent crude oil price has declined by nearly a quarter in the past month, it remains a fluid situation. Thus, the outlook for energy earnings, and European earnings more broadly, is nuanced until we assess corporate forward guidance in the coming weeks.

Analysts upbeat ahead of US earnings season

Looking across the Atlantic, analysts are unusually upbeat this earnings season. As we move to the start of earnings season later this week, analysts are expecting the S&P 500 to deliver earnings growth of 23% for last quarter, the second consecutive quarter where earnings growth could be above 20%. Analysts are not plucking growth estimates out of thin air, instead they have been guided by the companies themselves. According to Factset, the number of companies listed on the S&P 500 that have issued positive earnings guidance for Q2 is 111, double both the 5 and 10-year averages.

The US: a victim of its own success

Investors are getting used to strong earnings growth and earnings upgrades from the US. For seven straight quarters, the S&P 500 has beaten earnings estimates. At the same time as earnings have beaten expectations, the S&P 500 has risen by more than 45%. However, there is a downside to this, if earnings don’t deliver for Q2, then investor sentiment could fade. Turning back to Q2, the energy and the IT sectors are the shining stars. US tech has seen earnings estimates upgraded by more than 8% for Q2. Like Europe, it is the energy sector that has seen the biggest surge in earnings upgrades for last quarter, with a 61% increase. This is likely to be a temporary boost driven by the war in the Middle East, and if energy majors point to weaker growth in Q3 it could dent the market mood in Europe and the US.

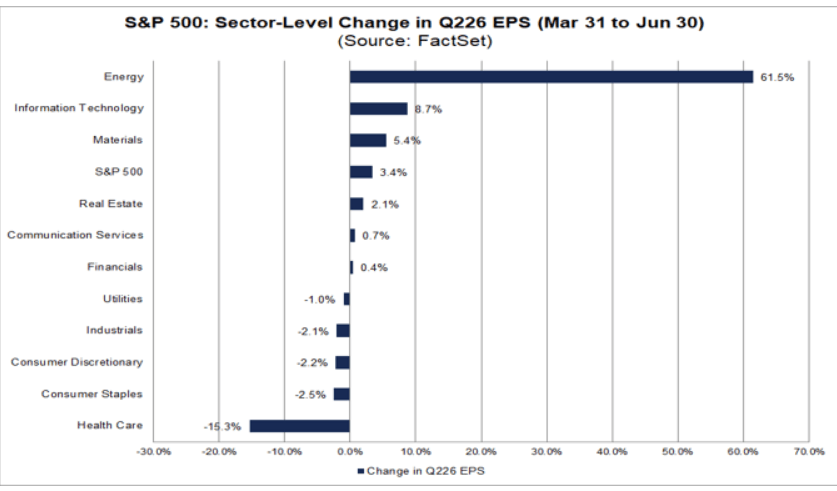

Strong fundamentals

Interestingly, every sector of the S&P 500 has seen revenue forecast upgrades as we lead up to this earnings season. Seven out of 12 sectors on the S&P 500 have seen an increase in earnings estimates, while healthcare has seen the largest decrease in expectations. Even though parts of the tech sector have seen their stock prices struggle this year, including the hyperscalers, these are the companies that are expected to be a major contributor to the S&P 500’s earnings growth for Q2.

Chart 1: US earnings upgrades by sector

Source: FactSet

The test for tech: can it continue to prop up US earnings growth?

The question is, what happens if tech can’t deliver? We don’t think Q2 will be the issue. Analysts are bullish for a reason and, in general, tech stock fundamentals remain strong. The bigger issue is what they signal regarding future revenue growth and capex expectations. For now, the US continues to outpace Europe when it comes to Q2 earnings season. But, beyond that, the outlook is less clear. Samsung earnings could be a warning sign to the US. Although the South Korean company delivered a 19-fold increase in Q2 profit YoY, the stock sunk nearly 7% as investors get nervous about the sustainability of chip stock earnings power.

The US holds the upper hand for now

There are already concerns that we may have reached peak AI investment, after Meta announced that it may start to sell off some of its unused AI compute last week. There are also concerns about the rocketing costs of building AI infrastructure, Apple has already had to raise prices due to surging memory costs, while Nvidia’s first AI gigawatt factory has seen costs soar to $100bn. Down the line, cracks in the AI narrative could allow the tech-lite European sector to outperform the US in future earnings seasons, although the US holds the upper hand for now.

The stock market outlook

From a stock market perspective, the US had a stunning Q2, while headline European indices were laggards. The Nasdaq had its best quarter in more than 5 years, while the Dow Jones Industrial Average rose to a fresh record. The average performance for US indices was 14% in the last 3 months, this compares to a 6.8% gain for France, an 8.2% gain for Germany and a 3.18% gain for the UK. However, other parts of Europe outperformed the US over the last 3 months. Both Italian and Greek indices rose by more than 14%, and Spain’s index rose by 10%. Europe is also having a stronger start to Q3 than US indices and are outperforming so far in July. Whether European stocks can keep this up could depend on how well US tech earnings are received. If we get a wobble in tech results in the US in the coming weeks, then Europe should maintain its lead over US indices.

Chart 1: The Nasdaq 100, the Dax and the FTSE 100, 1-month chart

Source: XTB