Michael Burry, the investor known for correctly betting against the U.S. housing market ahead of the 2008 crisis, has revealed another set of positions he has taken. This time it is about bookmakers: Flutter Entertainment and DraftKings. Burry’s thesis on companies offering sports betting looks, at first glance, logical and straightforward, but it has an important flaw. Bookmakers and some adjacent gambling-related businesses suffered sharp declines in 2025. This was driven by the growing mainstream adoption and expansion of so-called “prediction markets,” platforms offering bets not only on sports, but also on geopolitics, pop culture, weather, and many other topics.

While the justification for the business model of these companies, mainly Polymarket and Kalshi, is very fragile and stretches existing U.S. legal frameworks to their absolute limits, the impact on the market and the industry has been enormous. Monthly trading volumes on both platforms are already measured in billions of dollars, and Polymarket’s annual revenue has already reached one billion dollars. Their growth is currently measured in the hundreds of percent, and that growth is happening at the expense of “conventional” licensed operators. Burry believes this trend will soon come to an end. Platforms operating “prediction markets” are making fewer and fewer attempts to appear compliant, and they have begun offering sports betting, which is now in open conflict with U.S. law.

However, what is supposed to be the nail in the coffin for this fast-growing industry is not illegality, but money. Specifically, taxpayers’ money, and the lack of it. U.S. law provides that entities offering sports betting are subject to regulation and taxation at the state level. Prediction markets, meanwhile, despite offering sports betting, are classified as derivatives businesses, fall under the CFTC, and avoid state taxes and state law, while competing with local, law-abiding entities for the money of gamblers and speculators. In the shadow of the war in Iran, fears about inflation, AI, and the approaching midterm elections, a heated dispute between state and federal authorities is taking on a market character. In this dispute, Burry is clearly betting on the states, which over time are supposed to force compliance and tax payment, stripping platforms like Polymarket of their reason to exist.

CFTC defending prediction markets

Burry’s intuition is moving in the right direction, because individual U.S. states matter, and in groups they can force legislative change nationwide, but this scenario ignores a large and obvious risk. So far, the federal regulator in the U.S. has openly protected prediction markets:

- In April, the CFTC sued Arizona, Connecticut, and Illinois, arguing that states cannot create their own regulatory system for contracts on federally supervised markets.

- The CFTC also sued New York, seeking recognition that federal law gives it exclusive authority over derivatives and that state gambling rules cannot be applied to registered contract markets.

- In a similar vein, the regulator moved against Wisconsin after the state sued, among others, Kalshi, Polymarket, Crypto.com, Robinhood, and Coinbase, alleging violations of gambling law.

- A very important example was Rhode Island. In its complaint, the CFTC argued that sports contracts are “swaps” under the federal Commodity Exchange Act and that markets offering such contracts are registered Designated Contract Markets.

Regardless of the facts, legality, or the logic of the CFTC’s actions in the context of prediction markets, nothing currently indicates the agency will change its stance toward prediction markets anytime soon. The situation remains complex, because the CFTC is a regulator, not a court, as a simple narrative about an “upcoming ban” would suggest. The latest federal court decision in New York was unfavorable for Kalshi: the court held that the CEA does not automatically preempt New York gambling laws with respect to sports event contracts. Beyond the regulatory context, there is also the fundamental outlook for both companies, which looks promising even without Burry’s claims.

Flutter

Flutter is a global operator of online betting and gaming, with a strong position in the U.S. through FanDuel, and meaningful scale in the UK, Australia, and Italy. Investment bank analysts have noted that some of the pressure on results in 2026 is temporary, and their forecasts assumed group revenue rising from USD 18.3 billion in 2026 to USD 19.6 billion in 2027, with further EBITDA growth in the years that follow. Flutter is also one of the key players in the context of the World Cup, because it has one of the largest geographic exposures to countries present in the World Cup knockout stage. At the same time, Flutter is not staying passive in the face of the prediction market invasion. FanDuel, together with CME Group, launched FanDuel Predicts, its own event-contract platform, initially in five states, with plans to expand further. This is critically important, because sports contracts are meant to be offered where online sports betting is not yet legal, and after sports betting is legalized in a given state, FanDuel Predicts is supposed to stop offering sports event contracts there. Flutter can beat competitors on their own turf, supported by a diversified business and a giant partner like CME.

DraftKings

DraftKings is a different investment profile: pure exposure to the American market for online betting, iGaming, and its own attempt to enter prediction markets, with its pluses and minuses. The company launched DKeX, its own prediction market exchange, which vertically completes DraftKings’ integrated product ecosystem. If prediction markets are restricted, DraftKings benefits as a regulated bookmaker. Based on current trends, even if prediction markets remain under the current regime, the company is building its own infrastructure and customer base on solid foundations. JPMorgan estimated that in June, DraftKings was on track for more than USD 200 million in consumer volumes in prediction markets, more than 80% higher than in May.

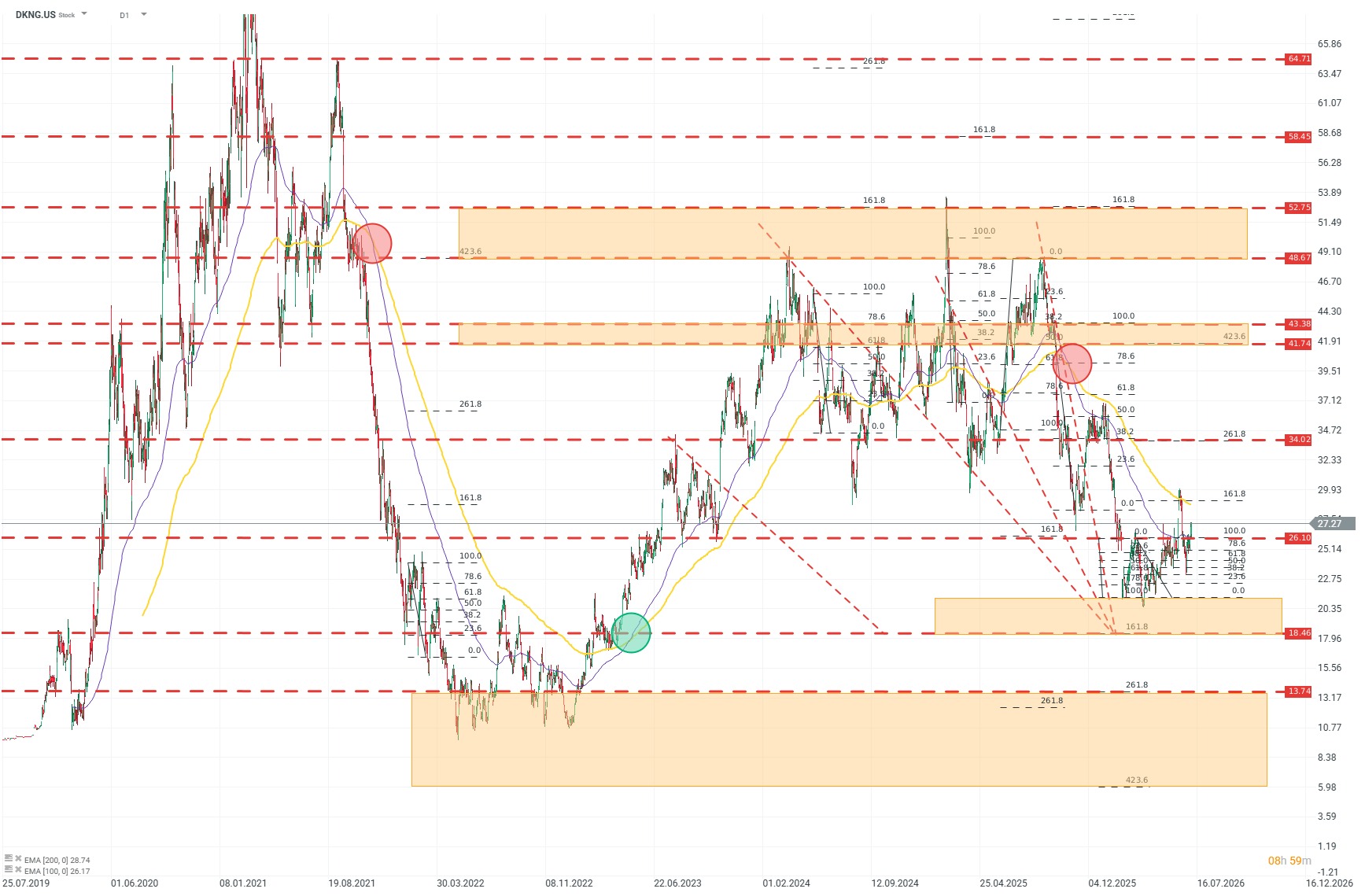

Technical analysis of DraftKings (D1)

From a technical perspective, DraftKings is in an interesting place. After the losses in the second half of 2025, one can see a slowdown in the trend and an increasingly bullish consolidation from around the USD 18 level. Fibonacci targets, set based on key price moves from the last few quarters, indicate potential demand targets at USD 41 to 43 and USD 48 to 52. Source: xStation5

Conclusion

In effect, all of this means these companies may outperform the broader market not because the CFTC will inevitably clamp down on the semi-legal activity of prediction markets. No. The best players in the betting and gambling sector have built their businesses under difficult conditions for decades. After a short-lived shock and market and regulatory turbulence, they are moving onto the offensive, and businesses like Polymarket or Kalshi may have no way to stop them. Burry may be right about the economic illogic of the current system, but wrong about the speed and scale of the political reaction. This contrarian and somewhat naive bet is supported by strong fundamentals and clear trends in performance.