It is noteworthy that today marks a trading holiday in the US markets. Americans are observing an extended weekend in celebration of the 250th anniversary of independence (4 July).

🗓️ Yesterday’s market review

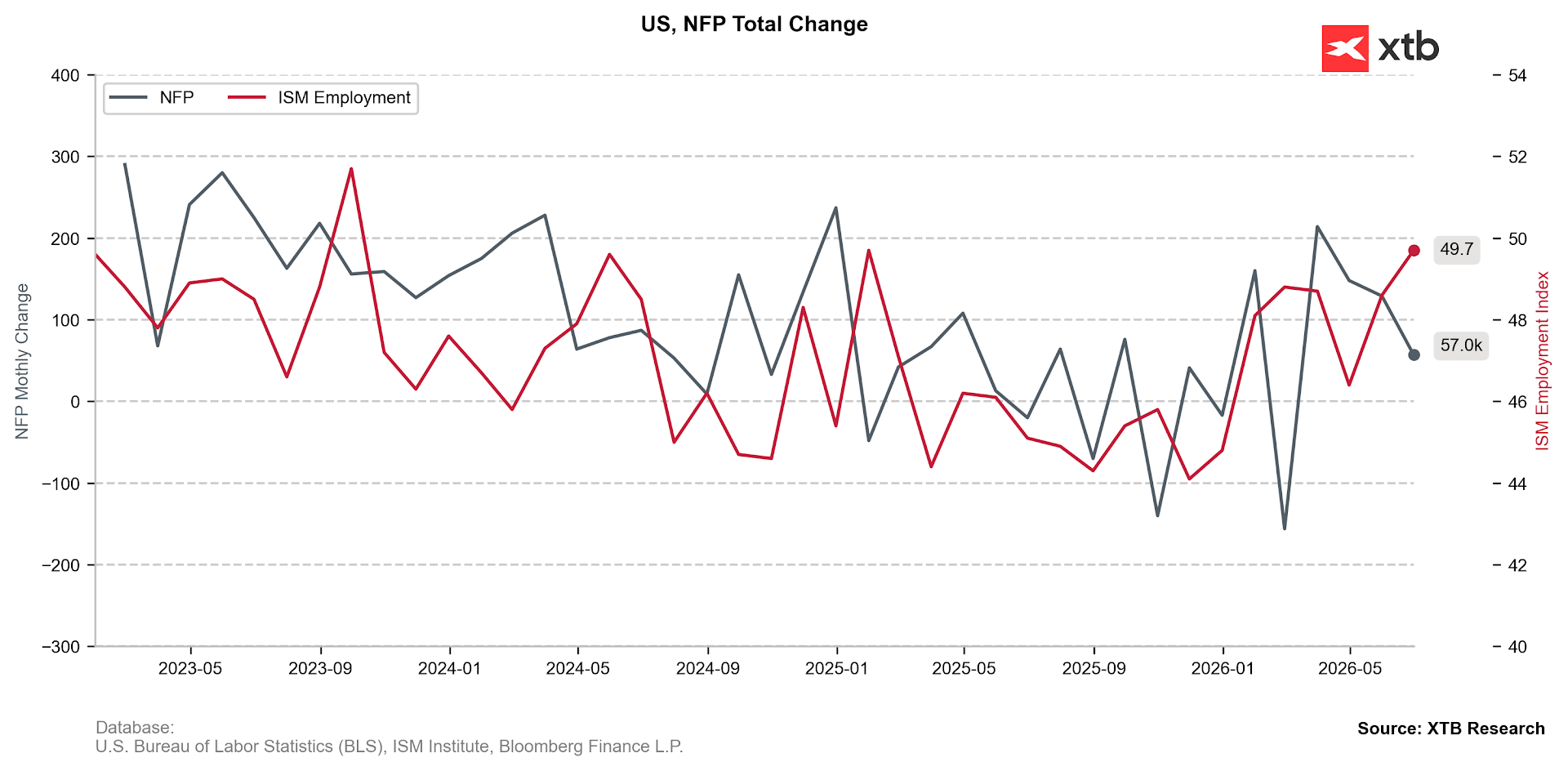

Yesterday’s trading was dominated by the publication of NFP data, which proved to be a disappointing surprise for investors.

- The data revealed a significantly lower-than-expected creation of new jobs (+49k vs. +107k), accompanied by a substantial downward revision of data for the previous two months (-74k).

Figure 1: Change in Non-Farm Payrolls (NFP) and ISM PMI Employment Sub-component (2023 – 2026)

Source: XTB Research, 03.07.2026

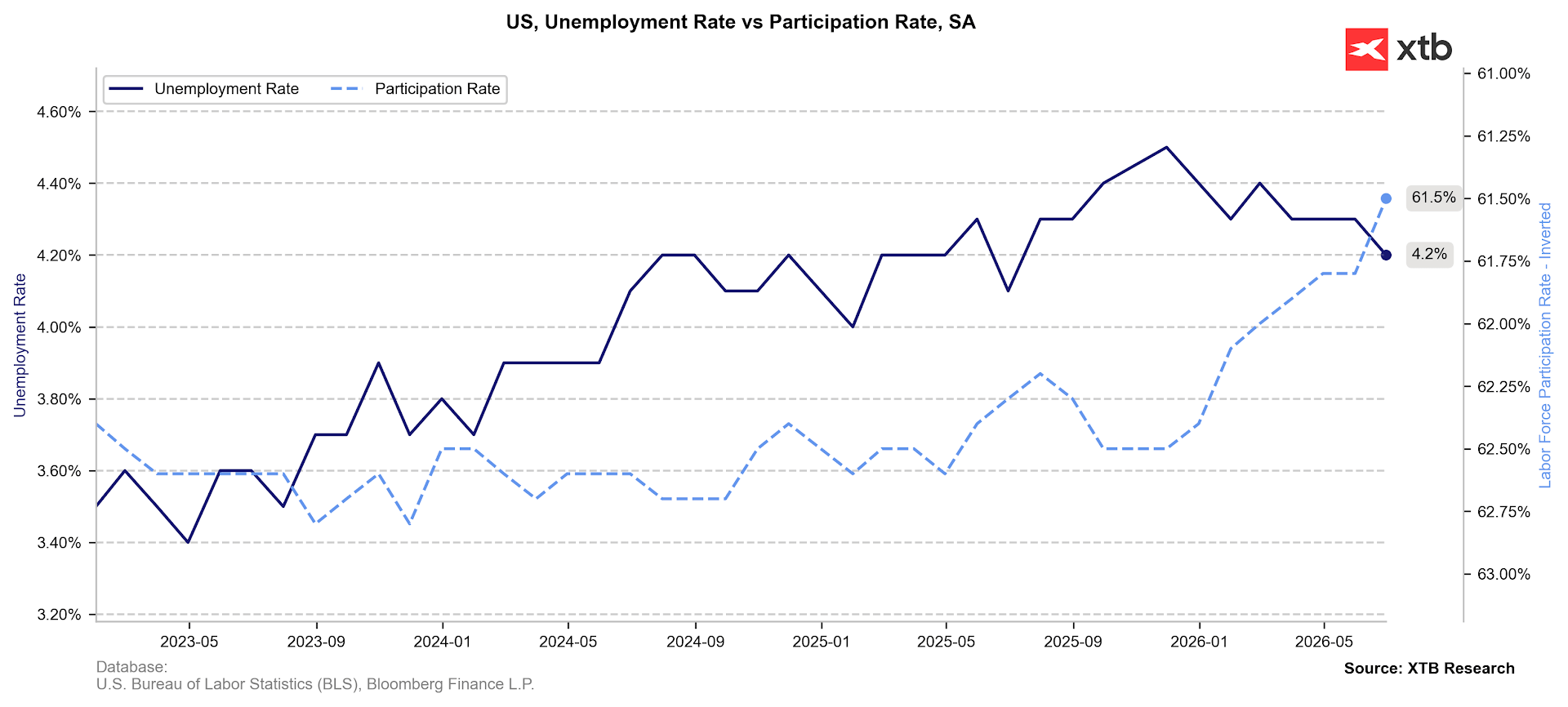

- The unemployment rate fell to 4.2%, which would typically invite optimism were it not for the significant decline in the labour force participation rate (61.5%). This metric was last seen at such low levels during the pandemic period.

Figure 2: Unemployment Rate and Labour Force Participation Rate in the USA (2023 – 2026)

Source: XTB Research, 03.07.2026

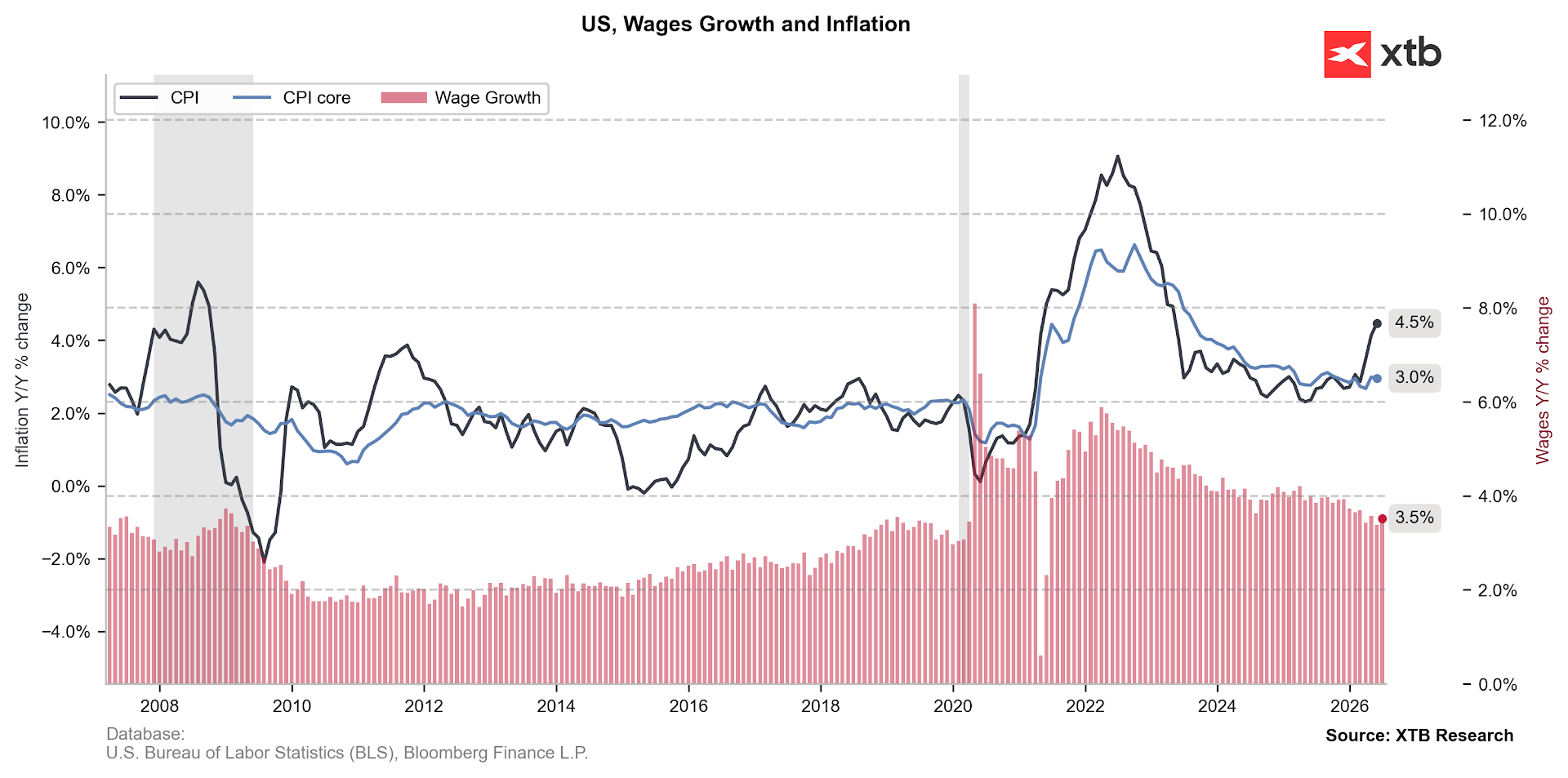

- Wage growth did not deviate from expectations (3.5%); however, it reached negative territory in real terms (-0.7%) after accounting for inflation. This is significant given that US consumption is currently being sustained largely at the expense of savings, with the savings rate having fallen to a mere 3%.

Figure 3: CPI Inflation and Wage Growth in the USA (2006 – 2026)

Source: XTB Research, 03.07.2026

The report triggered a correction in the market-implied interest rate path for the Fed. Investors continue to fully price in a rate hike before the year’s end, yet they assign a diminishing probability to such a move occurring during either of the next two meetings. This naturally weighed on the Dollar, which weakened by 0.5% against the Euro. The data also provided a temporary boost to the equity market. During later trading hours, we witnessed further capital rotation and a sell-off in technology sector stocks. Giants such as Intel and Micron recorded losses exceeding 5%, weighing on the Nasdaq 100 (-0.7%). Conversely, the more defensive Dow Jones closed the day with a clear gain (+1.1%).

🌏 Asian market trading Negative sentiment regarding big-tech firms was also present at the opening of Asian trading. However, the tide turned as the day progressed, and indices are concluding the session with significant strength. Following an initial sell-off, Korean exchange giants SK Hynix (10.2%) and Samsung (8%) experienced a robust rally, allowing the KOSPI to close over 5% higher. Over the past 12 months, the index has moved by nearly 160%. The Japanese Nikkei 225 and Chinese Hang Seng also strengthened by over 1%. In China, gains were driven by companies benefiting from rising gold prices, which have climbed by 4% over the last two days.

🌍 Geopolitics Donald Trump stated in a CNBC interview that negotiations with Iran are proceeding successfully and that Tehran has “agreed to practically everything we need.” He further remarked that the country has been “completely destroyed militarily.” On the Truth Social platform, he continued his criticism of NATO.

Markets paid closer attention, however, to communiqués issued by the Iranian military command: “Any disregard for orders, deviation from designated routes, or negligence of navigation protocols of the Islamic Republic of Iran in the Strait of Hormuz will be met with an immediate and decisive response from the armed forces, endangering the safety of vessels violating the prohibition.”

🛢️ Commodities This may partially justify the modest increase in crude oil prices at the opening.

- Brent crude oil (+0.9%) is currently trading at approximately $72 per barrel.

- WTI (+1.1%) is priced slightly above $69.

Natural gas prices have also moved higher:

- NATGAS (+1.2%) is hovering around $3.24 per MMBtu.

- TTF (+2.9%) is trading at just over $44 per MWh.

Precious metals continue their ascent, which can be primarily attributed to lower Treasury yields in major economies. This movement is supported by yesterday’s US labour market data.

- Gold is currently trading at just under $4181 per troy ounce, while silver is priced at over $62. This represents increases of 4% and 6.3% respectively over the past two days since the beginning of July.

📈Macroeconomic Data

During Asian trading hours, attention focused on the June PMI data. China Growth in the services sector slowed slightly but remained robust (54.1). A key driver was the increase in export orders.

- The number of orders rose for the eighth consecutive month, leading to a renewed increase in employment at the fastest pace since July 2024.

- Higher personnel, raw material, and transport costs drove prices higher, consistent with recent PPI inflation data (3.9%, the highest level in nearly 4 years).

Japan In Japan, the focus was primarily on data revisions, which are of secondary importance. Nonetheless, the services sector index rose from 51.8 to 52.2.

- It is worth noting that new orders in both the manufacturing and services sectors grew at their second-fastest rate in three years, largely due to stronger domestic demand rather than exports.

Further attention was drawn to statements by the Minister of Finance, Satsuki Katayama, who affirmed that Tokyo remains prepared to intervene in the foreign exchange market. She also emphasised close cooperation with Washington in this regard. Additionally, she addressed rising bond yields, stating that fiscal policy will be managed to restore market confidence. Australia A modest upward revision to June’s PMI data was also recorded in Australia.

- The services sector index was ultimately confirmed at 50.5.

- However, new orders, both domestic and foreign, declined.

- Output price inflation reached its lowest level since January.

- Confidence regarding the outlook for the next 12 months fell to its lowest point since November 2023, influenced by concerns over the economic environment and federal budget tax changes.

💱 Currencies The Dollar continues the sell-off initiated by yesterday’s disappointing NFP reading. The EURUSD pair is currently breaking the 1.146 level, rebounding by over 1% from recent lows. The Yen is also strengthening against the Dollar, with USDJPY returning below the 161 level. We are also observing an improvement in sentiment towards most emerging market currencies.