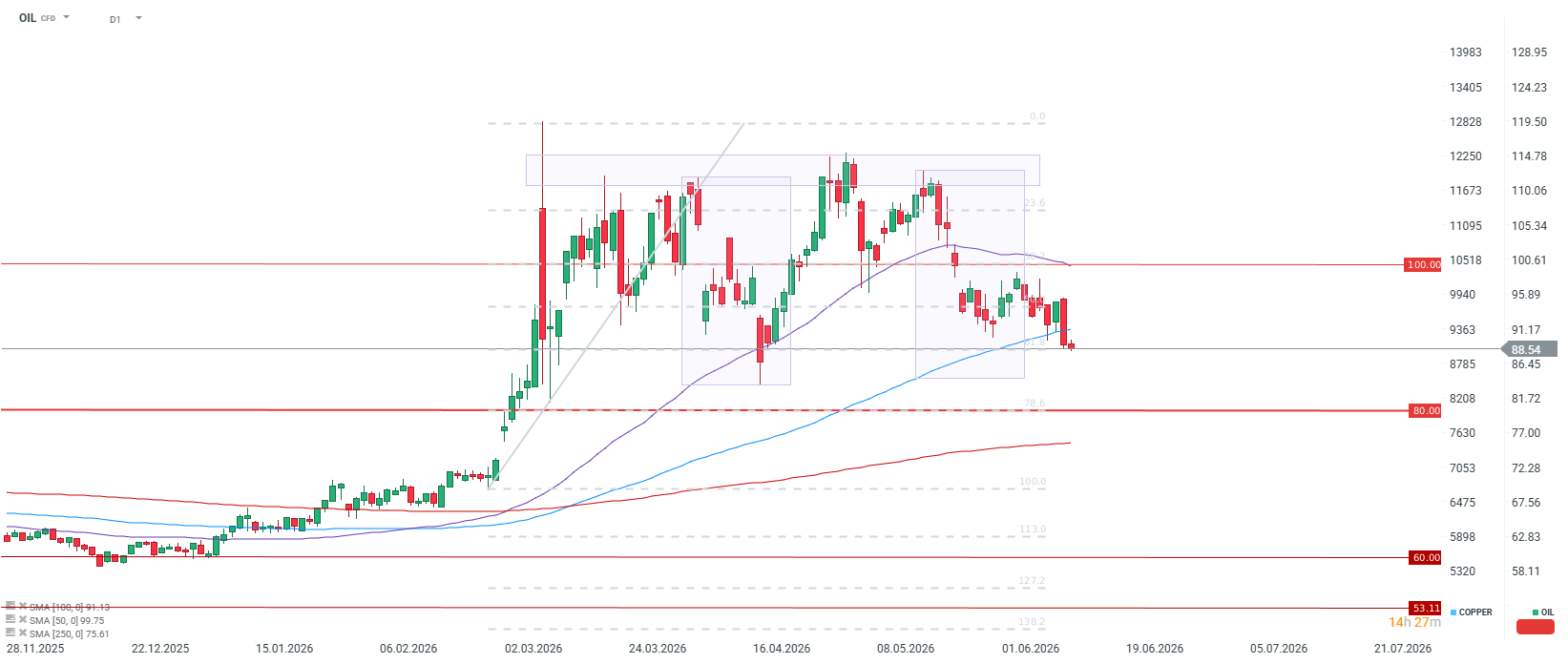

Oil prices have returned to sharp declines, reacting to Donald Trump’s announcements. First, he cancelled planned strikes on Iran that were supposed to take place last night, and second, he indicated that an agreement with Iran is essentially settled and may be signed in Europe in the near future. Brent crude fell below $90 per barrel, and following the rollover of WTI crude futures, quotes indicate a level below $85 per barrel.

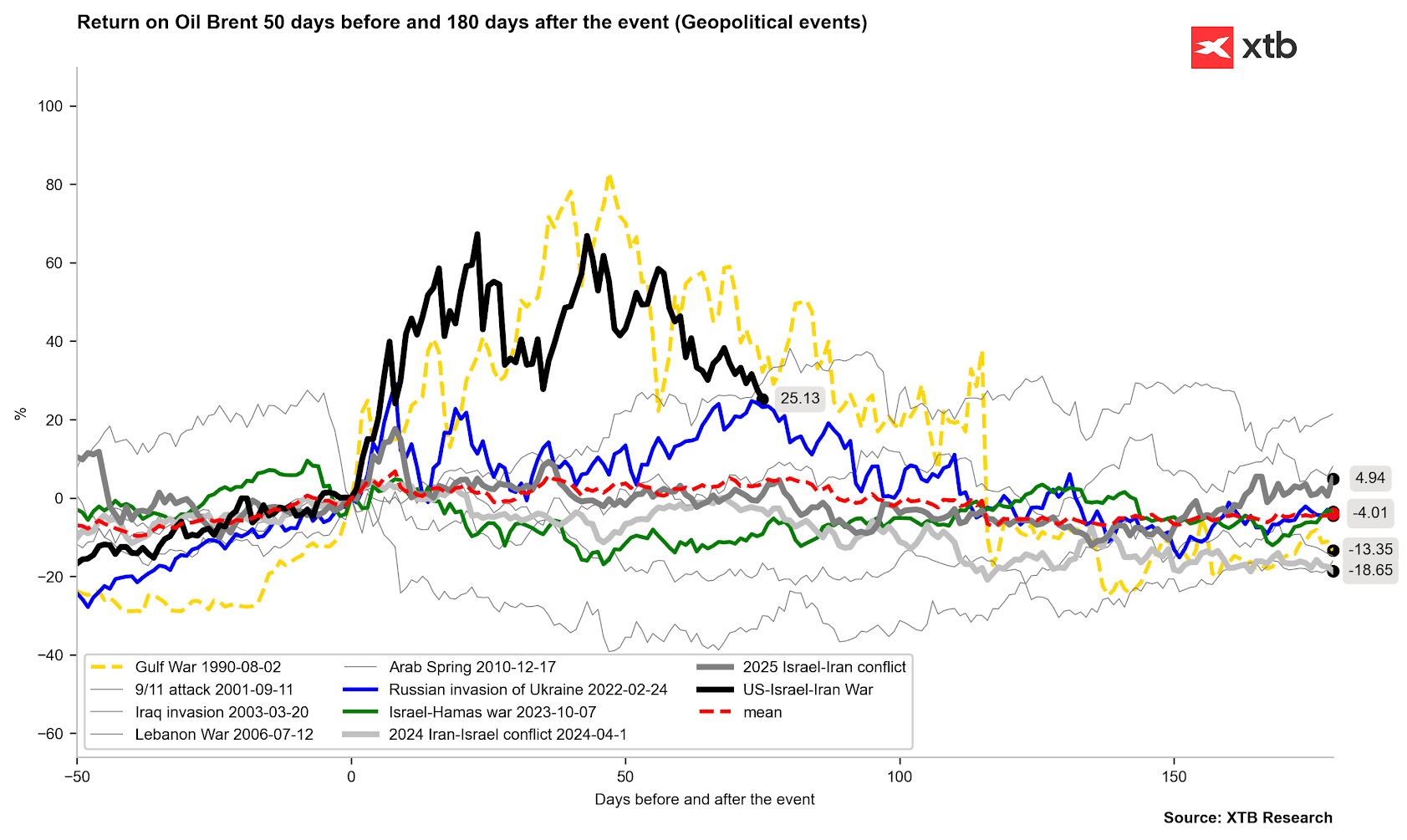

Excluding the impact of futures rollovers, oil prices are already just 25% higher than at the start of the conflict. The situations from 1990 and 2022 point towards further declines, although it should be remembered that the Strait of Hormuz remains closed. Source: Bloomberg Finance LP, XTB Déjà vu effect, or caution above all else Although the price reaction is sharp, history teaches us far-reaching restraint. It is worth remembering the hard facts:

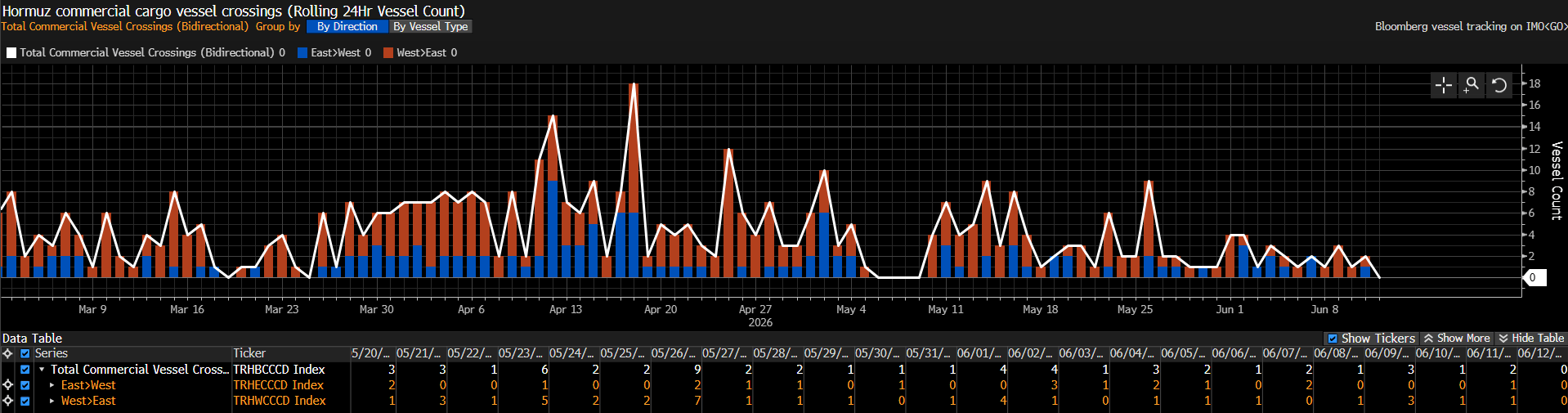

- Past promises: The American president has claimed dozens of times before that an agreement with Iran is within reach, yet so far none have materialized. Furthermore, even despite attempts, the number of ships passing through the Strait has fallen even compared to the situation when we had actual military operations.

- Skepticism from the other side: Tehran is effectively dampening enthusiasm, stating that final conclusions have not yet been reached, and local news agencies report that the text of the agreement has not been officially approved. The potential agreement itself is said to be in the form of a memorandum assuming, among other things, a 60-day ceasefire and the lifting of the naval blockade in exchange for a return to nuclear talks.

As can be seen, more ships passed through the Strait of Hormuz in April and March than now, although it should be noted that a large part of them could have come from Iran. Source: Bloomberg Finance LP, XTB The market believes in a compromise. Spreads and curve down Nevertheless, investors seem to strongly believe in a positive scenario this time. As voices from Wall Street indicate, there is a growing conviction that both sides simply have too much to lose in the event of a failure of talks, and a complete breakdown of negotiations has stopped being perceived as the most likely course of events. In light of these reports, we are observing classic behavior on the futures market implying de-escalation:

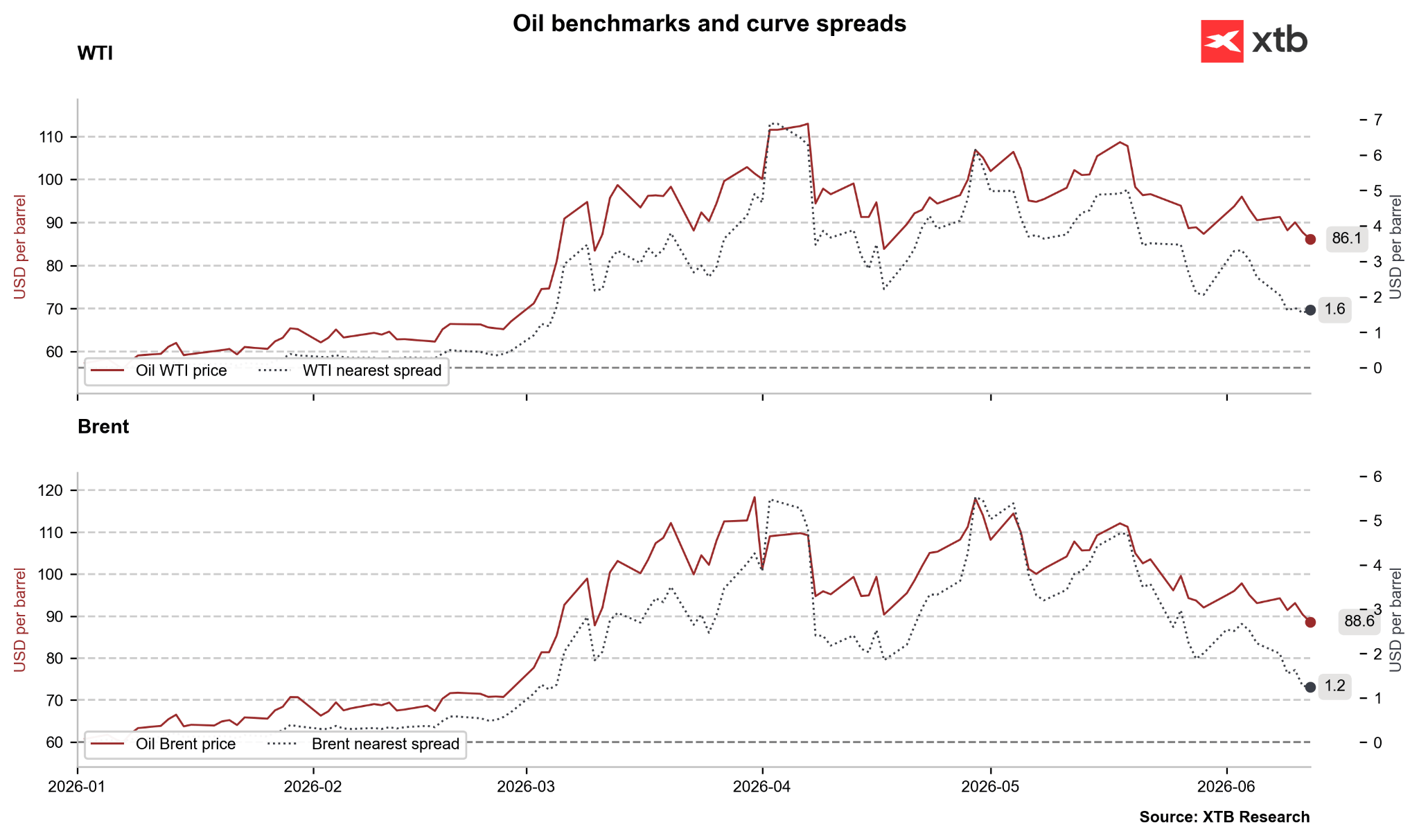

- Flattening of the forward curve: The market is sharply pulling the war risk premium out of pricing, which pushes the nearest contracts down significantly and flattens the entire term structure.

- Decline in calendar spreads: The vision of the imminent opening of the crucial Strait of Hormuz without additional fees means that market concerns about the immediate availability of the commodity are weakening. The premium for immediate delivery (backwardation) is falling sharply along with the sell-off of the nearest July and August series.

Spreads have fallen to levels from the start of the conflict. Source: Bloomberg Finance LP, XTB Technical and physical obstacles Remember that even if the documents are signed, a return to full physical normality will take months. Additionally, a successfully closed strait creates the risk of returning to a similar escalation if both sides start quarreling again. Furthermore, the need to remove mines from the Strait of Hormuz, repair energy infrastructure after drone attacks, and the time needed to restore shut-in production stand in the way. Interestingly, this de-escalation process overlaps with a very tight spot market. Inventories are clearly falling. Although globally they remain at high levels, in some places, such as Singapore or even at the Cushing terminal, stocks are extremely low and point to potential problems in the coming weeks if normal deliveries are not restored.