Behind us are days full of events significant from a market perspective – not only in the Middle East. On Wednesday, the May inflation data from the United States was published, which was a pleasant surprise for Fed policymakers. On Thursday, President Lagarde took the podium. With her statements, she unexpectedly struck hawkish tones. Today, macroeconomic attention focused on British GDP dynamics. There were no major surprises here. The economy contracted by 0.1% month-over-month. Investors’ minds, however, are elsewhere – on today’s SpaceX IPO.

Macroeconomic Data Thursday

- The European Central Bank raised interest rates by 25 bps. The decision was accompanied by relatively hawkish rhetoric from President Lagarde, who emphasized that economic growth in the eurozone is neither absent nor significantly threatened. She spoke with caution regarding inflation too. As we could hear: “Our decision is justified under any of the inflation projections – the one assuming significant escalation, the baseline scenario, and the scenario assuming de-escalation.”

- The decision was accompanied by relatively hawkish rhetoric from President Lagarde, who emphasized that economic growth in the eurozone is neither absent nor significantly threatened.

- She spoke with caution regarding inflation too. As we could hear: “Our decision is justified under any of the inflation projections – the one assuming significant escalation, the baseline scenario, and the scenario assuming de-escalation.”

- Weekly US unemployment claims rose to 229k, the highest level since February. Still, there is no major reason for concern regarding the labor market, especially since the market is still living off the extremely strong NFP reading.

- Still, there is no major reason for concern regarding the labor market, especially since the market is still living off the extremely strong NFP reading.

Friday

- The British economy contracted in April by 0.1% month-over-month. The decline was in line with expectations and follows two months of substantial growth (0.4% and 0.3%), which limits its negative undertone.

- The decline was in line with expectations and follows two months of substantial growth (0.4% and 0.3%), which limits its negative undertone.

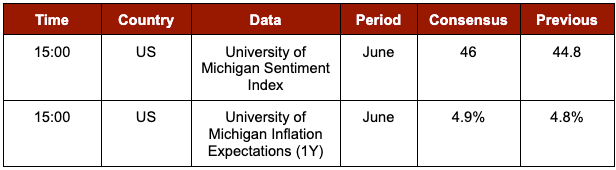

Macroeconomic Calendar Friday

Earnings Calendar USA

- Bitcoin Depot Inc. (BTM.US) – BMO (before market open)

- Replimune (REPL.US) – BMO (before market open)

- CURRENC Group (CURR.US) – BMO (before market open)

- Jiayin Group (JFIN.US) – BMO (before market open)

- Children’s Place (PLCE.US) – AMC (after market close)

- The Children’s Place (PLCE.US) – AMC (after market close)

- Fathom Holdings (FTHM.US) – AMC (after market close)

3 Markets to Watch

Nasdaq 100 (US100) SpaceX joins the index today. Interest in the company is massive, but the stock price is very high. This does not change the fact that it will be the largest IPO in history.

Dolar amerykański (USD) President Trump’s erratic communication is leading to heightened volatility in the currency market. Investors are also awaiting next week’s FOMC meeting.

Apple (AAPL.US) A few months ago, the company signed a $2.5 billion contract for television broadcasting rights to the MLS. The commercial success of this year’s World Cup, which may popularize soccer stateside, is therefore not without significance for it.