Market sentiment at the start of the session The market opened Thursday clearly influenced by a global rotation out of the AI/tech sector—gold and silver are leading the gains (up 0.79% and 1.10%, respectively), serving as safe-haven assets, while WTI and Brent crude are down more than 0.4–0.55%, continuing their worst quarter since 2020. Bitcoin is down 0.41% amid the general risk-off sentiment, and European indices are opening mixed—the DE40 is up a symbolic 0.03%, while the UK100 and US100 are slightly in the red, signaling investor caution ahead of this afternoon’s NFP report.

The greatest volatility is seen outside the main CFD table—the KOSPI opened with a drop of as much as 5–6%, triggering a trading halt (“sidecar”), while Samsung Electronics and SK Hynix lost over 7–9% at the open after the chip sell-off on Wall Street directly impacted Korean memory manufacturers. The Nikkei 225 is reacting more moderately (about -1% to -1.2%), and the Japanese yen, at a 40-year low (USDJPY 162.37–162.38 on our platform), is fueling speculation about intervention by the Japanese Ministry of Finance, especially given Friday’s low liquidity due to the U.S. holiday.

What to Look For—Today’s Top Stories

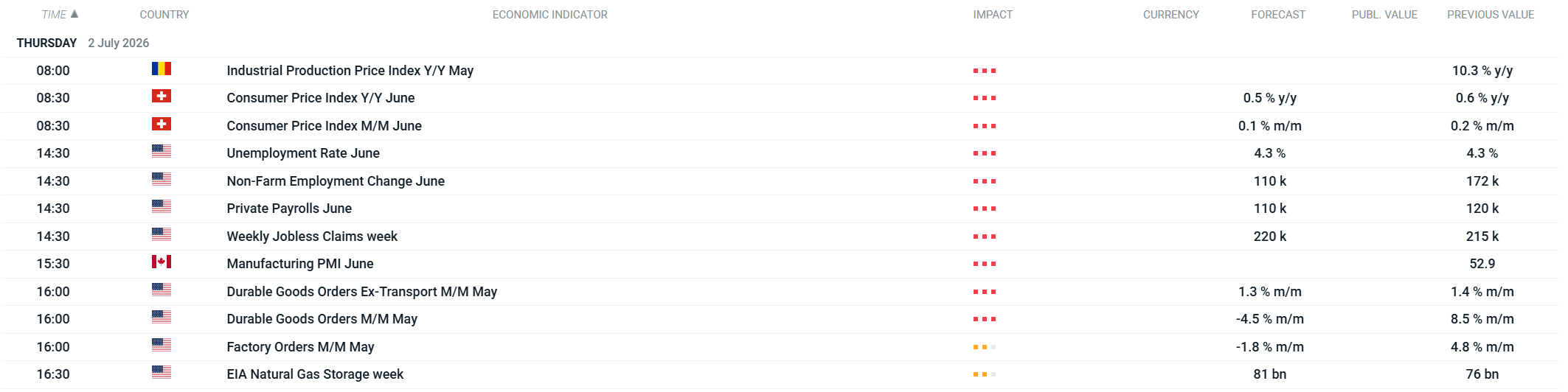

The key event of the day will be the June NFP report at 2:30 p.m. – the consensus is 110,000–115,000, compared to 172,000 in May, with the unemployment rate stable at 4.3% – and the wide range of forecasts (25,000–200,000) suggests a potentially sharp reaction from the USD and yields. It’s also worth keeping an eye on this afternoon’s data on durable goods orders and weekly jobless claims, which could further influence expectations regarding the Fed’s September decision. It’s also worth keeping an eye on the CPI data from Switzerland (8:30 a.m.) and durable goods orders from the U.S. (4:00 p.m.).

Today’s Macro Calendar. Source: xStation