Trump rejected Iran’s response to the peace proposal, calling it “TOTALLY UNACCEPTABLE” in a post on Truth Social, which triggered a widespread sell-off in the markets. Oil prices opened the week significantly higher in response to the US–Iran diplomatic deadlock, whilst the US dollar strengthened, thereby pushing gold and other precious metals lower. Amid shifting market sentiment, the major indices also saw their upward momentum stall. The key question now is “What next?”. Investors will once again be focusing their attention on the geopolitical landscape, as this is likely to remain the main driver of market volatility. It is also worth keeping an eye on:

- The main risk factor is the further development of US–Iran diplomatic relations — any sign of escalation (e.g. confirmation of military action against nuclear facilities) could send oil prices soaring and weaken equities. Tuesday will see a meeting of 40 defence ministers on the Strait of Hormuz — it is worth keeping an eye on the statements.

- US CPI data and retail sales this week will shape the narrative surrounding the Fed; PIMCO is already signalling that rate cuts are off the table.

- The Trump–Xi summit (13–15 May) — a potential game-changer for trade, sanctions and the situation in Iran; markets will be positioning themselves in advance.

- European markets likely to open under pressure : higher energy prices, weaker global sentiment, geopolitical tensions — a negative backdrop for the DAX, CAC and Euro Stoxx 50

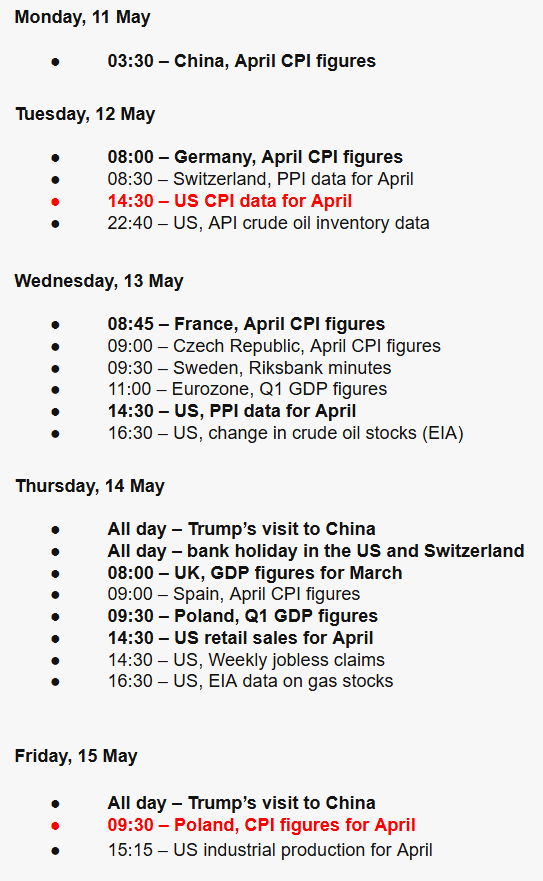

A detailed macroeconomic calendar for the whole week. Source: XTB Research, Bloomberg Financial Lp

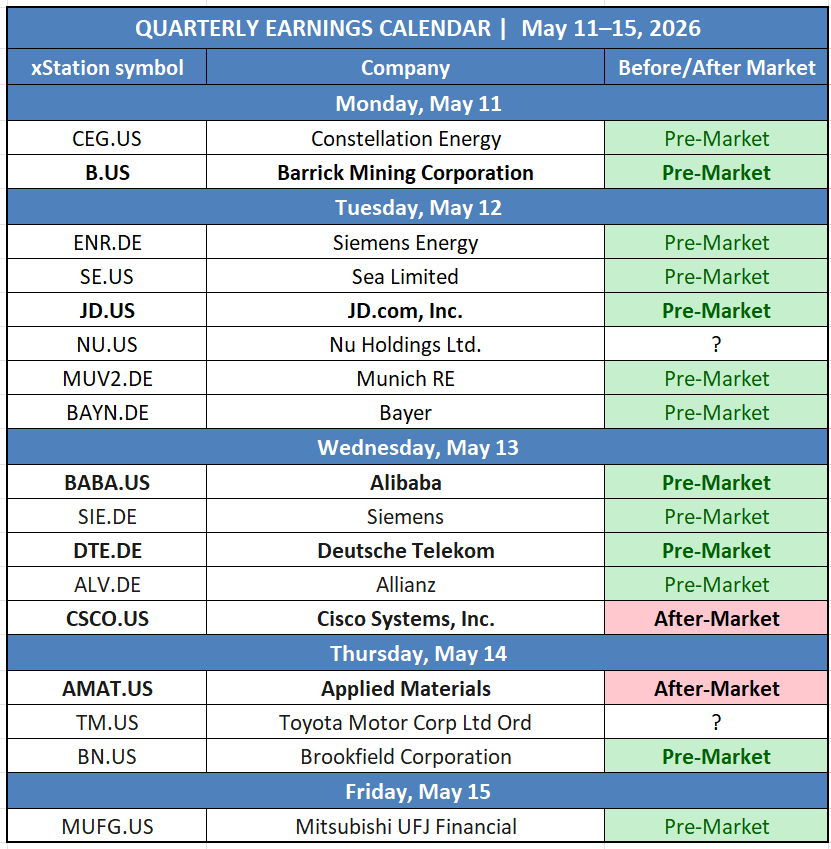

A detailed corporate calendar for the whole week. Source: XTB Research, Bloomberg Financial Lp