Nike Slides After Earnings – Shares Hit a 12-Year Low

Key takeaways

- Nike warns of a longer turnaround as weak China demand overshadows earnings beat

- The company reported revenue of $11.0 billion, down approximately 1% year-over-year, but slightly ahead of market expectations.

- Adjusted earnings per share came in at $0.20, well above the analyst consensus estimate of $0.13.

Although Nike delivered better-than-expected results for the fourth quarter of fiscal 2026, investors focused primarily on what management had to say about the future. Executives acknowledged that the company’s turnaround is taking longer than anticipated, consumer demand remains under pressure, and persistent weakness in China continues to weigh on performance. As a result, Nike shares fell nearly 3% in after-hours trading following the earnings release.

Key takeaways

- Nike reported $11.0 billion in revenue, down approximately 1% year-over-year , but slightly ahead of market expectations.

- Adjusted earnings per share came in at $0.20 , well above the analyst consensus of $0.13 .

- Reported EPS reached $0.72 , although it was significantly boosted by a one-time benefit related to import tariff refunds.

- The company expects revenue to decline further during the first half of fiscal 2027 .

- Sales in Greater China fell 17% , accelerating from the previous quarter.

- Nike shares are down roughly 35% year-to-date .

Better-than-expected earnings, but investors are looking ahead

At first glance, Nike’s earnings report appeared encouraging. The company exceeded analysts’ revenue expectations, improved profitability, and generated substantially higher net income than a year earlier. The biggest positive surprise came from margins and operating costs. Operating profit increased to roughly $1.3 billion , while net income reached approximately $1.1 billion . Lower cost of sales helped offset weaker revenue and supported stronger profitability. However, investors quickly shifted their attention away from historical results toward management’s forward guidance. That outlook ultimately became the biggest disappointment.

Management: Nike’s recovery will take longer

The most important takeaway from the earnings call was not the quarterly figures but the tone adopted by CEO Elliott Hill . Hill admitted that Nike’s turnaround remains uneven and will require considerably more time before meaningful improvements become visible. According to management:

- sales growth is improving only in selected categories,

- many new product launches are only now reaching stores,

- rebuilding wholesale partnerships is a multi-year process,

- the full impact of the new product strategy will not materialize until future quarters.

Hill also announced that Nike plans to introduce more than a dozen new footwear models, while emphasizing that these launches will take time to generate sustainable revenue growth.

China remains Nike’s biggest challenge

Greater China continues to be the company’s largest area of concern. Sales in the region declined 17% , compared with a roughly 10% decline in the previous quarter, making it one of Nike’s weakest-performing markets. Several factors continue to weigh on the business:

- softer consumer demand,

- market share losses to domestic competitors,

- elevated inventory levels at retail partners,

- a product portfolio that has recently been less compelling than rivals’.

Chinese sportswear brands such as Anta Sports and Li Ning continue gaining market share by capitalizing on rising consumer preference for domestic brands while responding more effectively to local trends. This is particularly important because Greater China still accounts for roughly 15% of Nike’s annual revenue , making it the company’s third-largest market after North America and Europe, the Middle East and Africa.

Consumers remain under pressure

Investors were also concerned by comments from outgoing Chief Financial Officer Matthew Friend . According to Friend: “We are not expecting the environment to improve meaningfully over the next six months.” Management believes consumers around the world remain pressured by elevated living costs, with sportswear and athletic footwear among the categories experiencing the greatest slowdown. Additional headwinds include:

- higher tariffs,

- geopolitical uncertainty,

- cautious consumer spending,

- continued clearance of older inventory.

Early signs of progress are beginning to emerge

Despite the cautious outlook, management highlighted several encouraging developments. The strongest improvement is currently visible in North America . Revenue in the region increased approximately 3% , supported by Nike’s renewed focus on rebuilding wholesale relationships after the previous Direct-to-Consumer strategy under former CEO John Donahoe. The company also reported improving demand for football products following a temporary slowdown earlier this year, helped by increased marketing around this year’s FIFA World Cup and a faster pace of new product launches. Nike additionally expects gross margin to turn slightly positive during the first quarter of fiscal 2027.

One-time gains boosted reported earnings

Reported earnings also benefited from a significant non-recurring item. Nike recognized approximately $986 million related to the anticipated recovery of previously paid import tariffs. As a result, reported earnings per share reached $0.72 , while adjusted EPS excluding one-off items amounted to only $0.20 . For investors, this suggests that the underlying operational improvement is more modest than the headline earnings figures initially indicate.

What investors are watching now

Over the coming quarters, investors are likely to focus on several key developments:

- whether sales in China begin to stabilize,

- the pace of rebuilding wholesale partnerships,

- the success of upcoming product launches,

- the impact of tariffs and import costs on margins,

- consumer demand trends in North America and Europe.

If Nike’s new product cycle gains traction and North American momentum continues, investors may begin reassessing the company’s long-term earnings potential. For now, however, management itself acknowledges that Nike’s turnaround will take longer than the market had expected only a few quarters ago. Nike is currently in a transition phase. Operational fundamentals are gradually improving, supported by stronger profitability, revenue growth in North America, and the first signs that the company’s new strategy is gaining traction.

Nevertheless, the business continues to face significant challenges, particularly in China, where demand remains weak, competition is intensifying, and inventory normalization is still ongoing. Over the next several quarters, investors are likely to place greater emphasis on evidence that the turnaround is accelerating rather than on individual quarterly earnings beats.

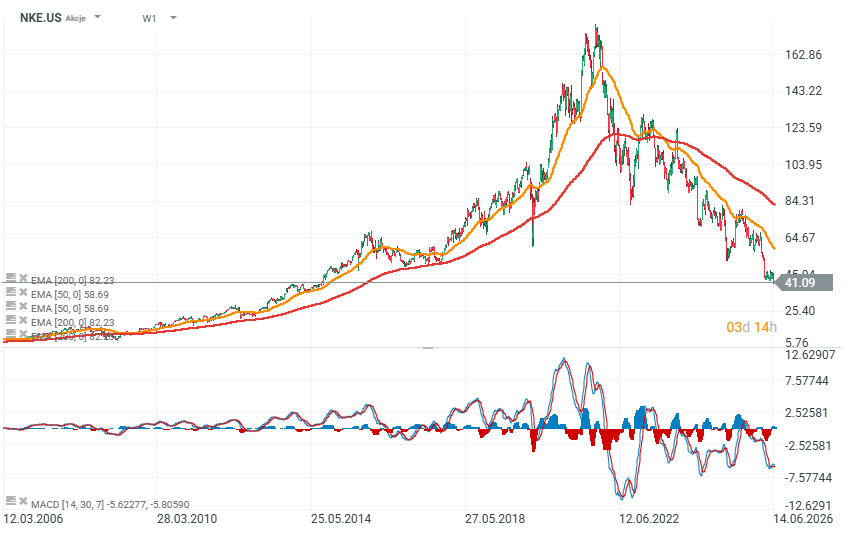

Nike shares and valuation (NKE.US)

Nike shares are now trading at levels not seen since 2014 , having declined nearly 80% from their all-time highs . After-hours trading following the earnings release suggested the stock could open below $40 per share , roughly 50% below its 200-week moving average . The scale of the selloff is historically significant and reflects investors’ concerns about the pace of the company’s recovery.

Source: xStation

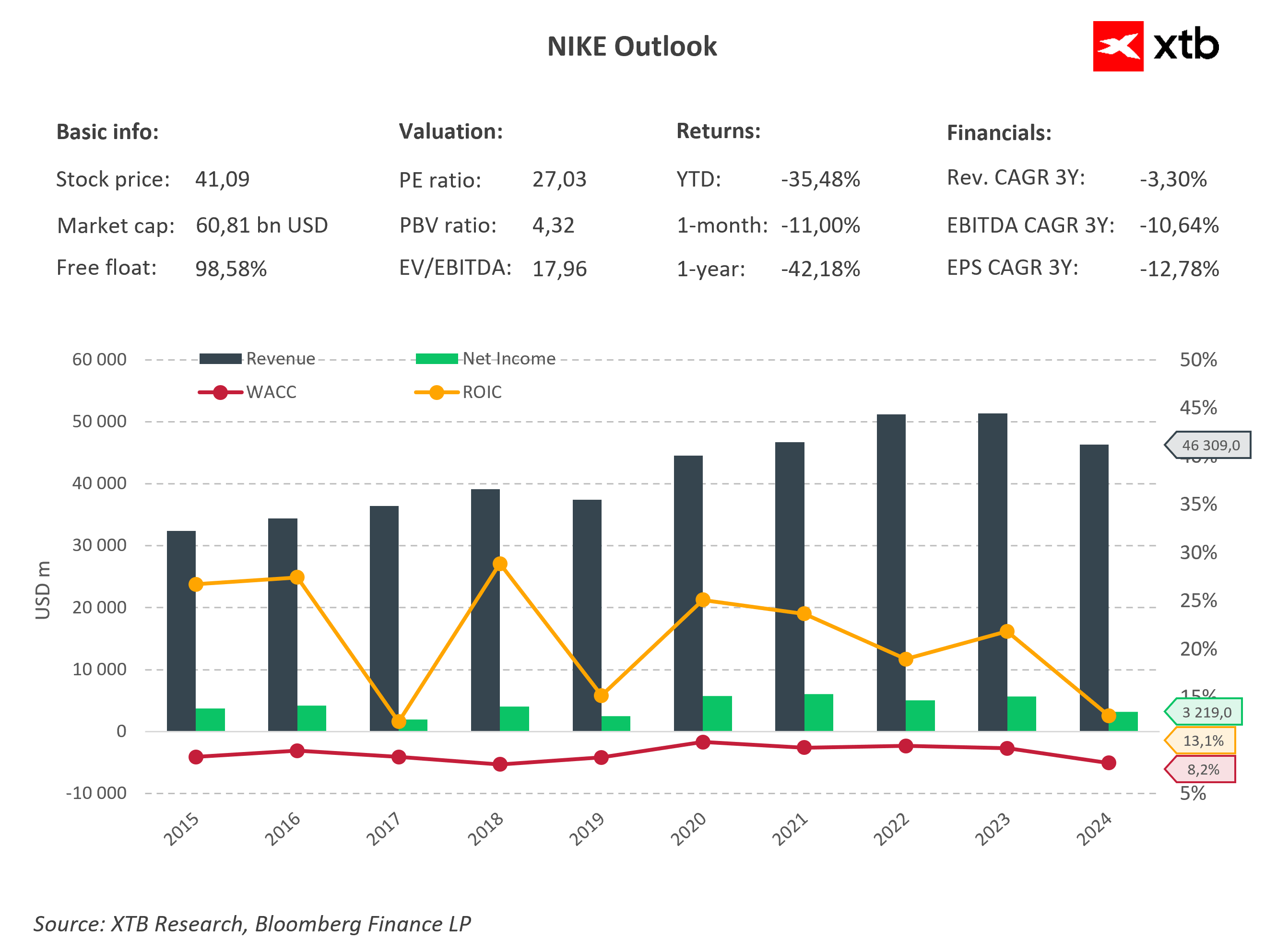

Despite losing more than 35% year-to-date and over 42% during the past twelve months , Nike remains one of the world’s most profitable sportswear companies. The company has a market capitalization of approximately $60.8 billion , while its price-to-earnings ratio of around 27 —roughly 10% above the average for S&P 500 companies —suggests that the stock is not particularly cheap, with investors still assigning meaningful value to its long-term recovery potential. At the same time, deteriorating fundamentals cannot be ignored. Over the past three years, revenue, EBITDA, and earnings per share have all posted negative compound annual growth rates. The chart clearly illustrates that after reaching record revenue of more than $51 billion in fiscal 2022 and 2023, sales have started to decline, falling to approximately $46.3 billion . Net income has dropped even more sharply to around $3.2 billion , reflecting margin pressure caused by inventory clearance, softer consumer demand, and continued weakness in China. Even so, Nike continues to generate a return on invested capital (ROIC) of approximately 13% , comfortably above its estimated weighted average cost of capital (WACC) of around 8% . This indicates that the company is still creating value for shareholders, although the margin between returns and the cost of capital is considerably narrower than it was several years ago. The next few quarters will be critical in determining whether CEO Elliott Hill’s turnaround strategy can reverse the company’s negative trajectory. If sales in China begin to stabilize and new product launches successfully accelerate revenue growth, today’s valuation could ultimately prove attractive. However, if revenue continues to decline throughout fiscal 2027, investors may once again lower their expectations for one of the world’s most recognizable athletic brands.

Source: XTB Research