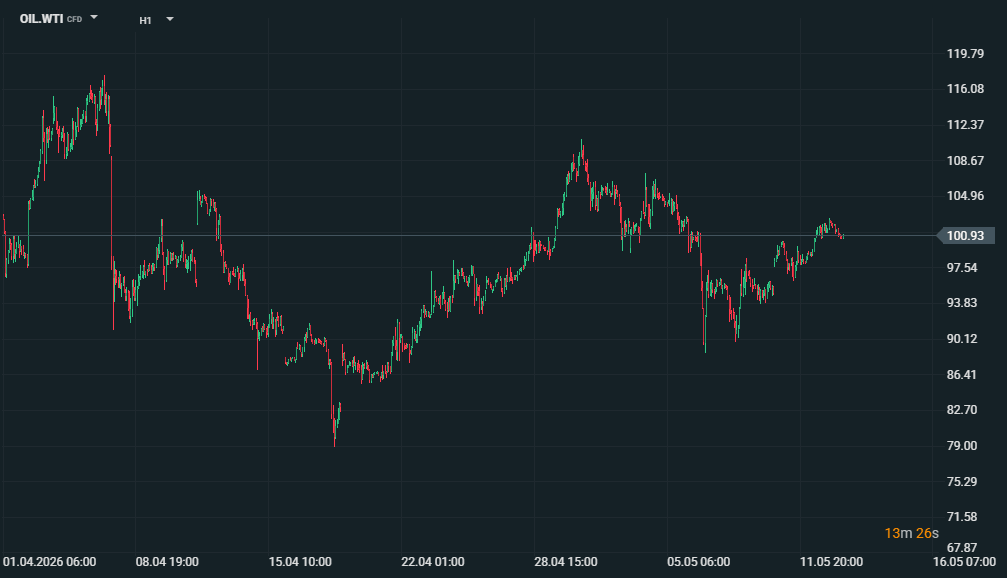

Oil prices remain highly sensitive to developments in the Middle East, with Brent and WTI still holding around 100 USD per barrel despite a slight pullback today. The market continues to be supported by ongoing disruptions around the Strait of Hormuz, where the blockade is still restricting a significant portion of global supply. Prices started to edge lower after three consecutive days of gains, as investors looked for greater clarity regarding the fragile ceasefire and the upcoming Trump–Xi summit in China. The latest EIA forecasts point to a much deeper and longer-lasting supply shock than previously expected.

The agency now assumes that the Strait of Hormuz will remain effectively closed until the end of May, with Middle Eastern oil supply losses peaking at around 10.8 million barrels per day this month. As a result, global inventories are expected to decline by 2.6 million barrels per day this year, a significantly larger draw than in previous forecasts. The EIA expects Brent to average around 106 USD per barrel in May and June before easing toward 89 USD in the fourth quarter as regional production gradually recovers.

At the same time, the agency warns that if disruptions persist for one additional month, prices could temporarily rise by another 20 USD per barrel. At the same time, high prices are increasingly weighing on the demand outlook. The EIA cut its forecast for global oil demand growth to just 200 thousand barrels per day this year from the previous 600 thousand, citing demand destruction caused by high energy costs. More expensive fuel is already translating into broader inflation concerns, complicating the outlook for consumers, central banks, and the US economy.