Philip Morris reports strong quarterly results

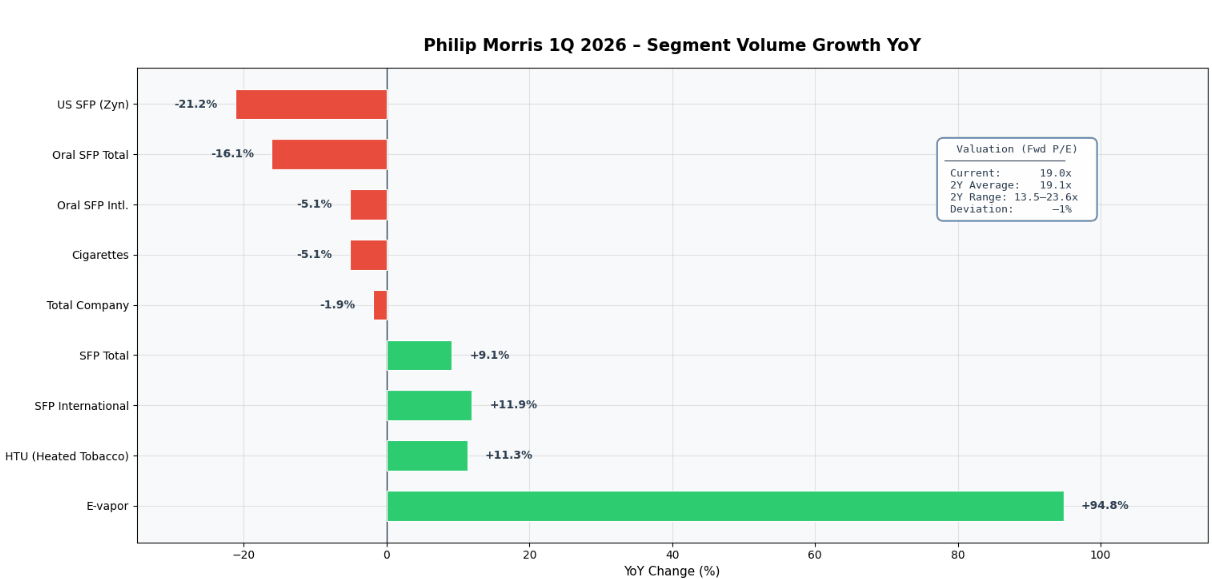

Philip Morris (PM.US) reported strong results yesterday for the first quarter of 2026, significantly exceeding market expectations. The main driver of growth remains the international smoke-free products segment (primarily IQOS), which recorded organic revenue growth of 15.8% with volume growth of 11.9%. This segment now accounts for 43% of the company’s total revenue, bringing it closer to its goal of generating more than two-thirds of sales from smoke-free products by 2030. The weak point was the U.S. Zyn nicotine pouch segment, where volumes fell by 21.3% y/y due to an uneven competitive environment and shipping issues—they totaled 155 million pouches versus the expected ~160 million.

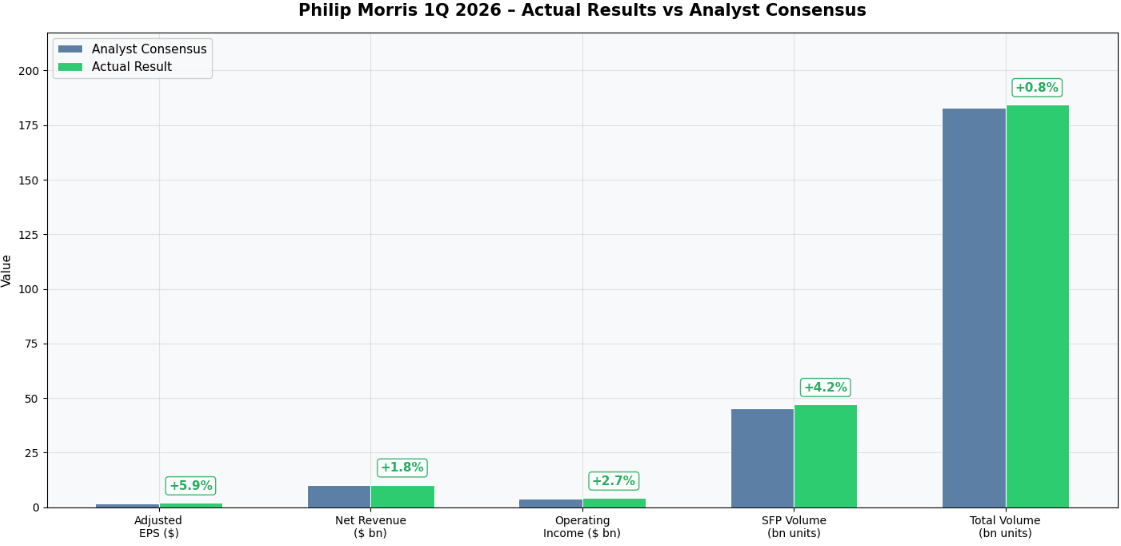

Philip Morris beat analysts’ expectations across all key metrics for Q1 2026, with the biggest positive surprise coming from adjusted EPS (+5.9% vs. consensus), which drove the stock price up by more than 6% on the day of the earnings release. Source: XTB Key Q1 results vs. analyst consensus:

- Adjusted EPS: $1.96 vs. forecast of $1.85 (beat by 6%, up 16% year-over-year)

- Net revenue: $10.15 billion vs. forecast of $9.97 billion (beat by ~2%)

- Adjusted operating profit: $4.17 billion vs. forecast of $4.06 billion (beat)

- Total shipment volume: 184.3 billion units vs. forecast of 182.9 billion (beat)

- Volume of smoke-free products: 47.0 billion units vs. forecast of 45.1 billion (beat)

- Cigarette volume: 137.3 billion units vs. forecast of 138.3 billion (miss)

- Growth in e-cigarette volume: +94.8% year-over-year

- Decline in total volume: -1.9% (consensus estimate was -2.6%)

A clear divergence between segments – spectacular growth in e-vapes (+94.8%) and solid growth in IQOS (+11.3%) contrast with a sharp decline in the U.S. Zyn market (-21.2%). Source: XTB

Annual forecast and the impact of external factors

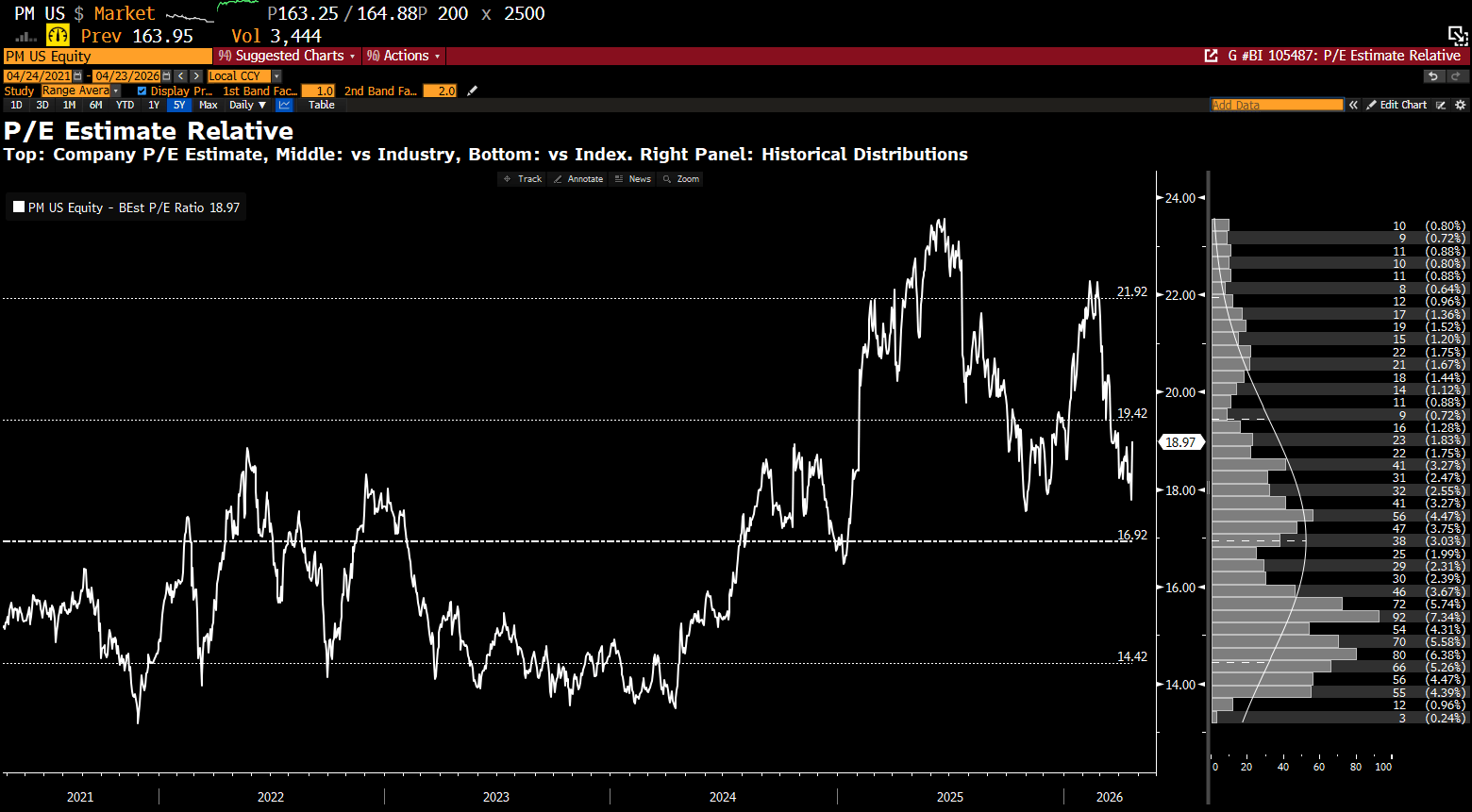

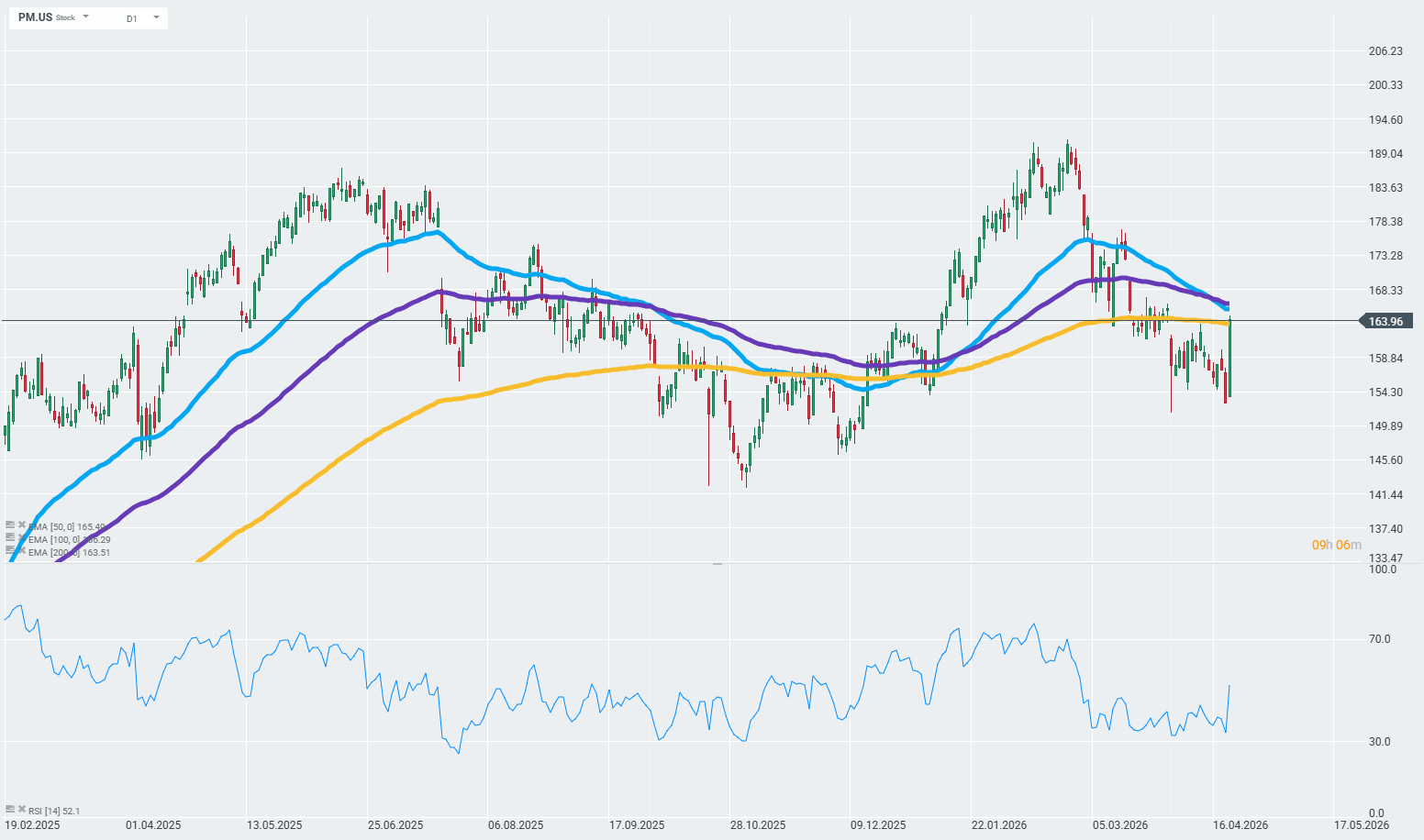

Management slightly lowered its full-year adjusted EPS guidance by 2 cents (to $8.36–$8.51 vs. the consensus of $8.39), which is solely due to a smaller-than-expected positive impact from foreign exchange rates (25 cents instead of 27 cents). The remaining elements of the guidance were maintained: organic revenue growth of +5–7%, organic operating profit growth of +7–9%, and operating cash flow of ~$13.5 billion. The company noted a slight impact of the conflict in the Middle East on transportation and energy costs, but observed no significant change in consumer behavior. Pricing PM shares are trading at a forward P/E ratio of ~19.0x, which is virtually equal to the two-year historical average (19.1x)—the deviation is just -1% (-0.1 standard deviations). Similarly, EV/EBITDA (15.3x vs. an average of 15.1x) and EV/EBIT (16.5x vs. 16.3x) are close to historical norms. The historical P/E distribution over the last 5 years shows that the current multiple of ~19x falls in the upper part of the range (2-year range: 13.5x–23.6x), suggesting that the company is fairly valued—neither at a discount nor at a significant premium. The stock rose by over 6% following the earnings release, recouping part of this year’s ~4.5% loss.

Source: Bloomberg Financial L.P.

The company’s shares closed above the 200-day EMA yesterday, which can be seen as an important indicator of the long-term trend. Source: xStation