Apple (AAPL.US) has found itself at the center of a serious geopolitical and regulatory dispute—the company is actively lobbying the Trump administration for permission to purchase memory chips from ChangXin Memory Technologies (CXMT) , a Chinese manufacturer that appears on the Pentagon’s 1260H list as a so-called “blacklisted” entity. Why Is Apple Turning to CXMT? Cost pressures are real and already evident in price lists. Apple has raised the prices of iPads and MacBooks, stating outright that it can no longer shield customers from sharp increases in memory and storage costs, driven by the construction of data centers for AI. Lobbying efforts at the Department of Commerce have been ongoing for over a month, and Apple has expanded its campaign to other agencies and allies in Washington. Technically, Apple is not prohibited from purchasing chips from CXMT—but the company’s presence on the 1260H list creates a significant political and reputational barrier.

Senate Floor: Cotton’s Warning

Senator Tom Cotton left no room for doubt—the company’s use of products from this Chinese supplier would be a “fatal mistake” both for long-term shareholder value and for customer privacy and U.S. security. This is not just rhetoric: CXMT was designated as a Chinese military company by the Biden administration and subsequently approved by an interagency committee for inclusion on the Commerce Department’s Entity List. Licenses to purchase from entities on this list are, as a rule, denied . Real Risks for Apple The case highlights a structural problem facing the entire big tech sector:

- Memory costs are rising due to the AI boom in data centers — Apple isn’t the only one affected, but as a mass-market consumer electronics manufacturer, it is particularly vulnerable

- Supply-chain concentration — The DRAM market, dominated by Taiwan and South Korea (Samsung, SK Hynix), does not offer much room for negotiation

- Legislative and regulatory risks — any approval by the White House would be politically costly and could trigger a bipartisan response from Congress

- Reputation in the U.S. — One of Apple’s most valuable assets is consumer trust, especially in the premium segment

Valuation in Historical Context — What Do the Numbers Say? EV/EBITDA (NTM) currently stands at 23.6x , which places the company slightly above the 3-year median of 23.2x . The range of standard deviations shows that current multiples are right at the upper limit of the historical norm—+1 standard deviation is 24.9x—so the company is not extremely expensive, but it is not cheap either. By comparison, during the COVID-19 crisis at the turn of 2023–2024, Apple regularly traded below the median, closer to the -1 standard deviation level (~21.2x).

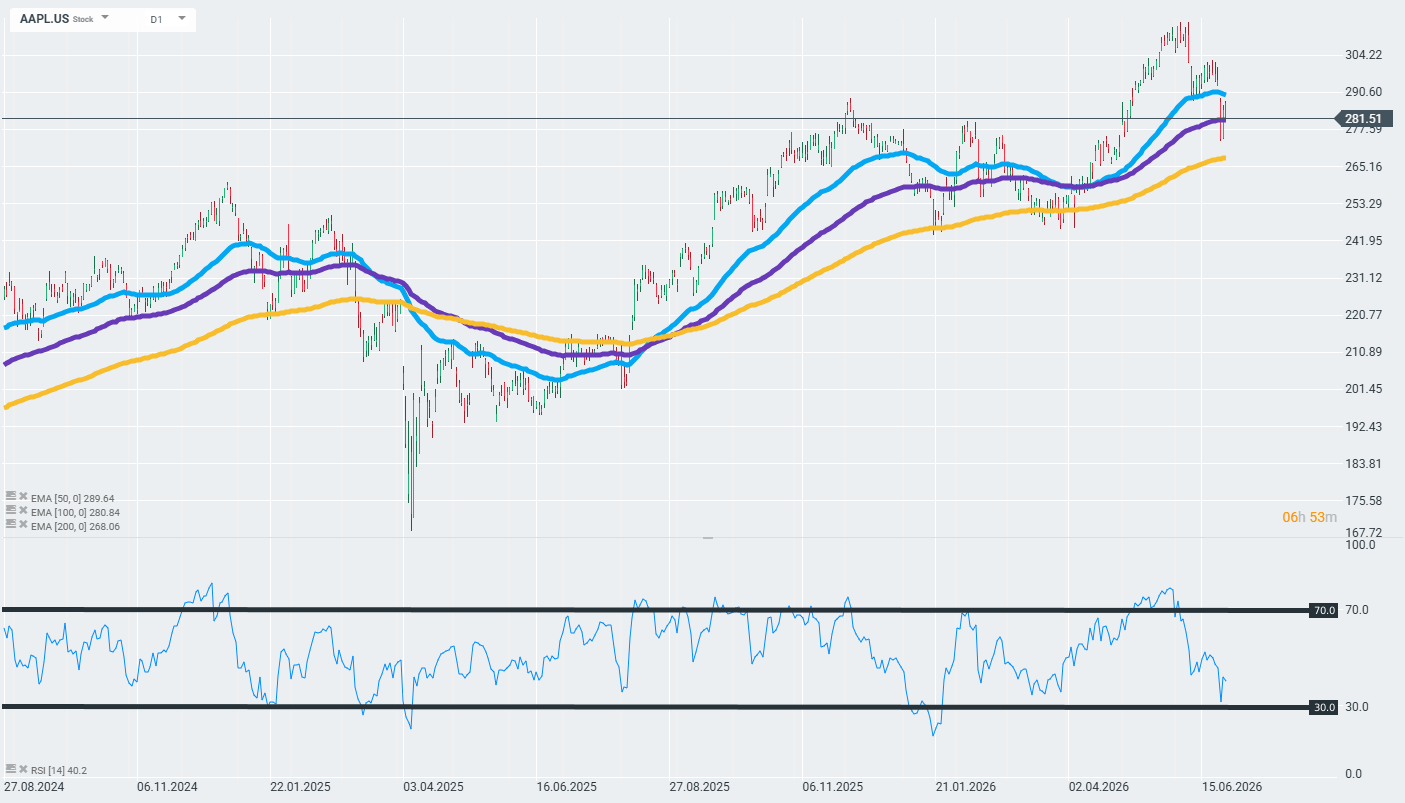

From a technical standpoint , the situation is just as mixed:

- The price (~$281) is below the EMA50 ($289) and is currently testing the EMA100 ($280) as support

- The EMA200 at ~$268 remains well below that level, indicating a continuing long-term uptrend

- RSI(14) = 40.2 — the company has clearly moved out of the overbought zone (70+, where it was in May 2026) and is approaching the neutral zone, with the potential to further test support levels