In the context of an expected end to hostilities in the Middle East, many investors may turn their attention to the situation of defense companies. Despite a period of unprecedented geopolitical tension, several active armed conflicts, and large-scale rearmament programs in the US, Russia, and much of Asia, these companies are marking new lows.

Beyond the question of what may be driving this behavior in valuations, it is also worth asking whether, given a seemingly negative impulse, these companies still have room for further declines. The issue of declining valuations is not specific to particular sub-sector, countries, or individual companies; rather, it is a broad market move that can be observed across the entire industry.

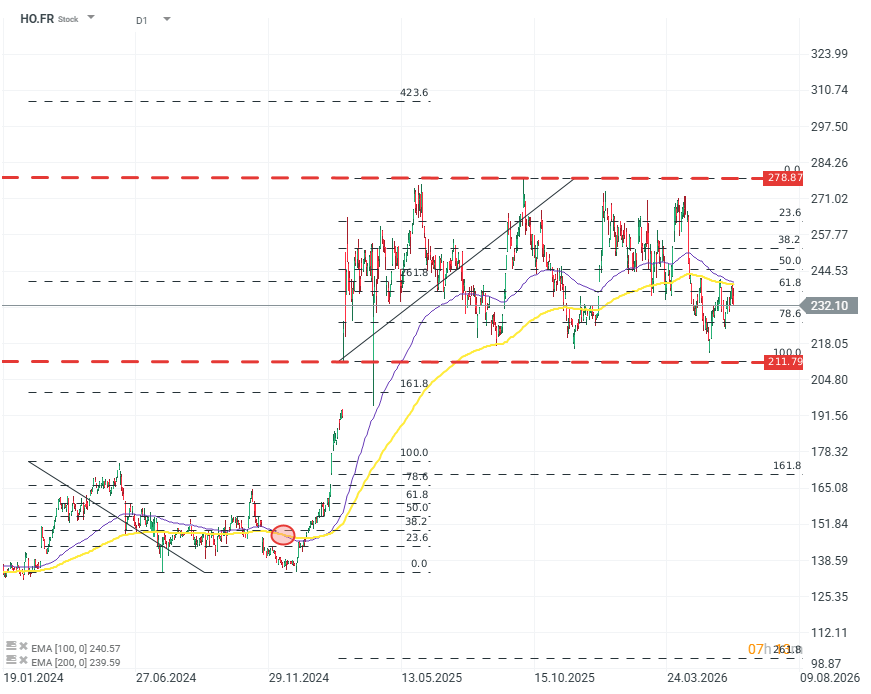

HO.FR (D1)

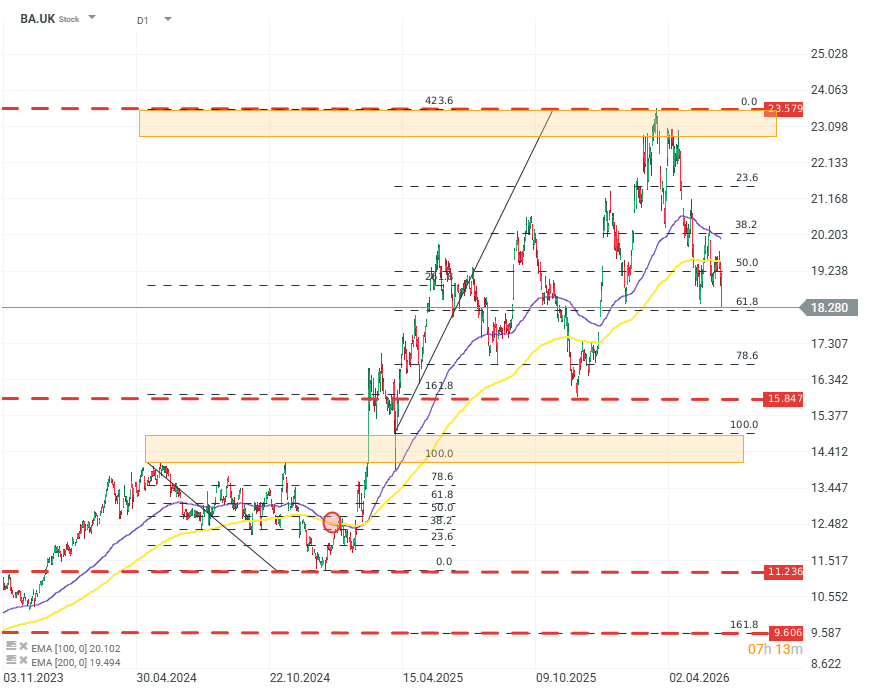

BA.UK (D1)

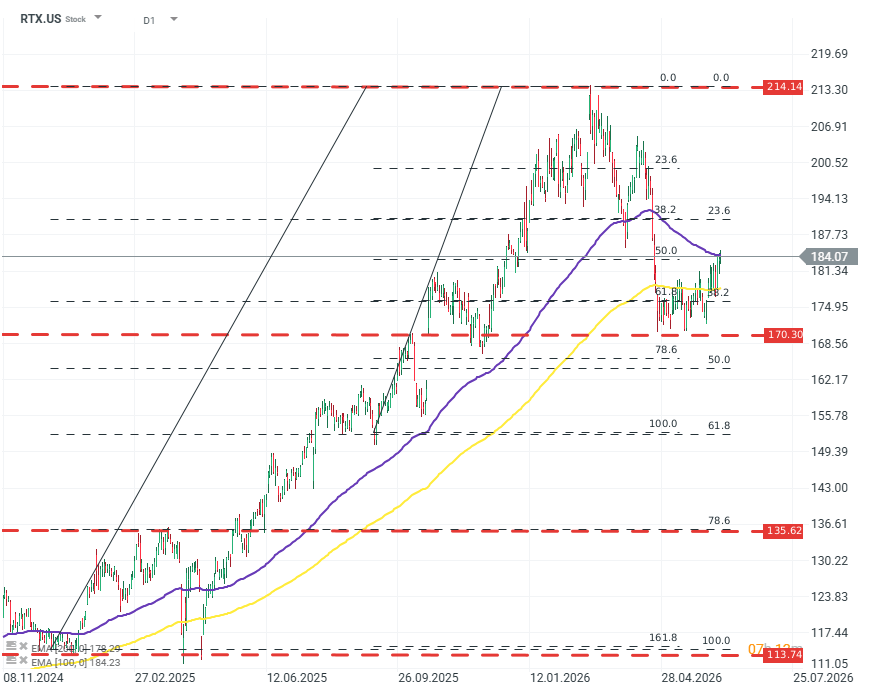

RTX.US (D1)

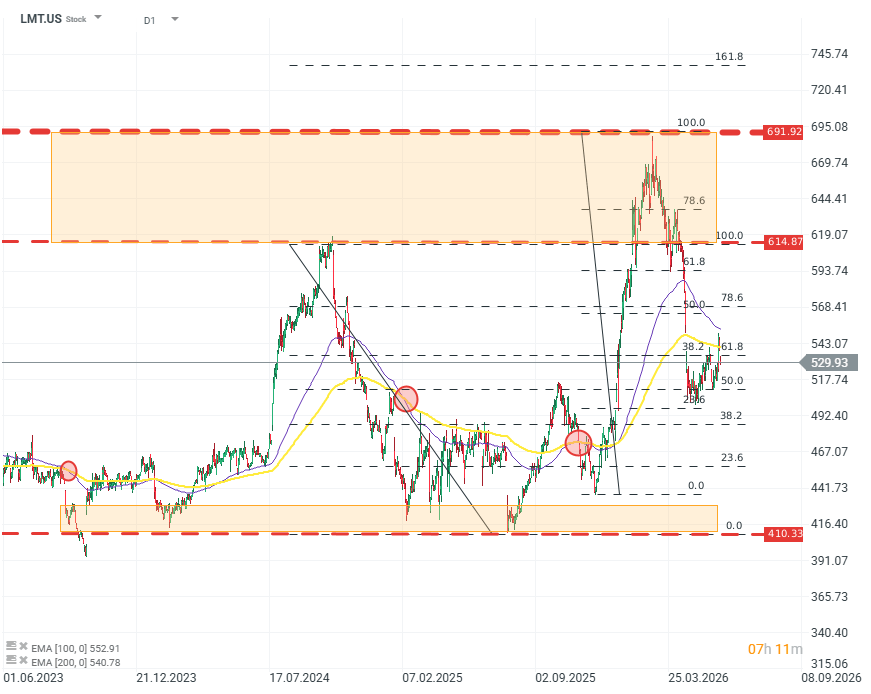

LMT.US (D1)

From a technical perspective, it can be noted that nearly all major contractors, both in the US and Europe, are currently in a relatively negative, tet also specific and similar, position. All entities of this class are currently below or very close to the EMA200 moving average, where the EMA100 crossing below it (from underneath) traditionally signals a deepening of declines, a loss of momentum, and/or a reversal into a downtrend. However, this tendency is not as clear in the case of defense stocks, particularly European ones, where such a formation has often preceded the exact opposite phenomenon.

Source: xStation5

Are there grounds for growth beyond the technical view?

The fundamental situation of companies in the sector is currently much better than the technical picture. In terms of (adjusted) EPS, companies in both Europe and the US have been able to deliver annual earnings-per-share growth ranging from a few percent to several dozen percent, and the market expects improvement across the sector in the years 2026–2028.

EPS changes (Adjusted) in 2023–2025

- BAE Systems (BA.UK) – 9% annual growth

- Rheinmetall (RHM.DE) – 30% annual growth

- RTX (RTX.US) – 11% annual growth

- Lockheed Martin (LMT.US) – 12% annual decline

- Thales (HO.FR) – 7% annual growth

Expected growth for 2026–2028 according to Bloomberg Finance data

- BAE Systems (BA.UK) – 13% annual growth

- Rheinmetall (RHM.DE) – 42% annual growth

- RTX (RTX.US) – 10% annual growth

- Lockheed Martin (LMT.US) – 7% annual growth

- Thales (HO.FR) – 13% annual growth

The data shows not only that valuations do not reflect significant profitability growth. More importantly, the market does not seem to differentiate between the momentum or situation of specific entities, which would suggest that valuations at this stage are driven more by sentiment than by data. There may be several reasons for valuations behaving this way, but the most important phenomenon here may be the “crowding-out effect”, mainly from the technology sector. Capital is flowing into entities that promise even higher growth rates, and as a result, high-quality companies are being discounted despite a lack of fundamental justification. In the current market and geopolitical environment, one can expect these companies to continue their downward trend in the short/medium term; however, both the technical and fundamental situation may point to a potential “inflection point” for the sector.