EMEA is dragging down Ferrari’s results, But the profits and FCF tell a different story

Ferrari NV (RACE.IT and RACE.US) has published its results for the first quarter of 2026, which turned out to be mixed – solid in terms of profitability, but disappointing in terms of delivery volumes. The company’s shares are currently attempting to regain some ground following initial declines resulting from the results release. At the moment, the shares are up 3% in Milan. The main factor casting a shadow over the results was the armed conflict in the Middle East, which significantly disrupted deliveries to the EMEA region.

Results

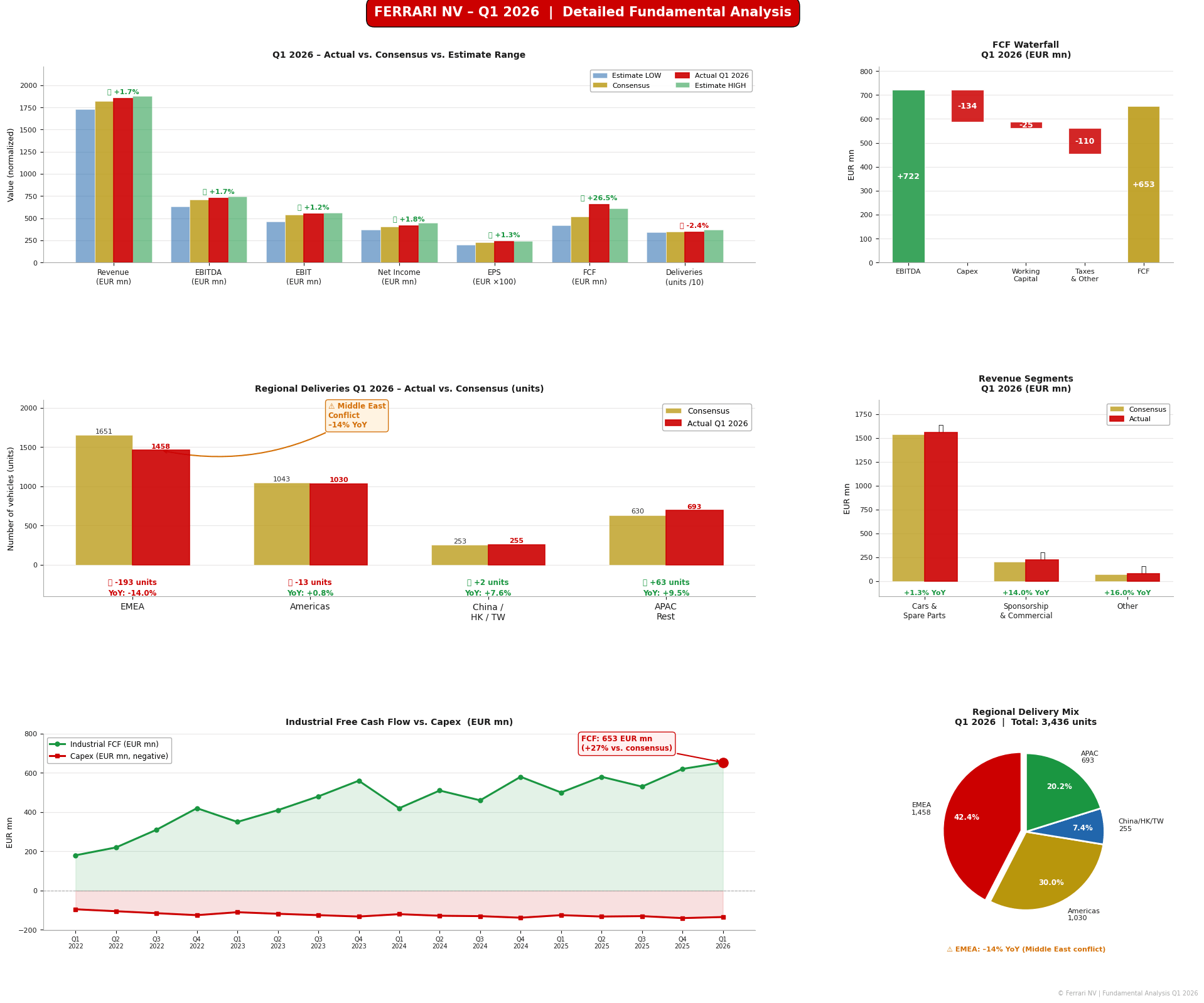

Ferrari’s revenue stood at €1.85 billion, representing a 3.2% year-on-year increase and exceeding the analysts’ consensus estimate of €1.82 billion. EBITDA reached €722 million, rising by 4.2% year-on-year and beating market expectations of €710 million. The EBITDA margin stood at 39.1%, slightly below the estimated 39.3%. EBIT came in at EUR 548 million (+1.1% y/y), with an operating margin of 29.7%, in line with the consensus, though lower than the 30.3% recorded a year earlier. Net profit stood at EUR 413 million, rising by just 0.2% y/y. Diluted EPS reached EUR 2.33 compared to EUR 2.30 a year earlier and above the consensus of EUR 2.30. Industrial free cash flow (Industrial FCF) proved spectacular – EUR 653 million against an expected EUR 516 million, representing an increase of nearly 40% above the consensus.

A graphical representation of the company’s results for selected items. Source: Bloomberg Financial Lp, XTB

What was disappointing?

The key disappointment was global vehicle deliveries, which totalled just 3,436 units, down 4.4% year-on-year and significantly below expectations of 3,520 units. Deliveries to the EMEA region plummeted by 14% y/y to just 1,458 units, against a consensus of 1,651 – a clear effect of the armed conflict in the Middle East. Ferrari partially offset these losses by redirecting deliveries to other regions. Deliveries to the Americas rose by 0.8% y/y to 1,030 units. Mainland China, Hong Kong and Taiwan recorded a 7.6% y/y increase to 255 units. The rest of the APAC markets rose by 9.5% y/y to 693 units.

Forecasts

The company has confirmed its full-year forecast for 2026, projecting revenue of around €7.5 billion, adjusted EBIT in excess of €2.22 billion, and industrial FCF in excess of €1.5 billion. CEO Benedetto Vigna assured that the situation in the Middle East is “under control” and that no extraordinary order cancellations have been recorded. Ferrari’s order book has extended to the end of 2027, giving the company exceptional revenue visibility within the automotive industry. Goldman Sachs analysts expect Ferrari to raise its conservative forecast in Q2 or Q3 2026, supported by the ramp-up of the F80 supercar and the 296 Versione Speciale model. The company is also preparing for the launch of the all-electric Luce supercar, priced at around €550,000, which represents a key test for the brand’s electrification strategy. The sponsorship and commercial rights segment grew by an impressive 14% y/y to €218 million, whilst other revenue jumped by 16% y/y to €74 million.

Key Findings and Forecasts – Summary

- 📊 Q1 2026 revenue: €1.85 billion (+3.2% y/y) vs. consensus of €1.82 billion ✅

- 💰 EBITDA: EUR 722 million (+4.2% y/y) vs. consensus of EUR 710 million ✅

- 📉 EBITDA margin: 39.1% vs. expected 39.3% ⚠️

- 🔧 EBIT: EUR 548 million (+1.1% y/y) vs. consensus of EUR 541.5 million ✅

- 📉 EBIT margin: 29.7% vs. 30.3% a year earlier ⚠️

- 💵 Net profit: €413 million (+0.2% y/y) vs. consensus of €405.7 million ✅

- 📈 Diluted EPS: €2.33 vs. consensus of €2.30 ✅

- 💸 Industrial FCF: 653 million EUR vs. consensus of 516 million EUR ✅✅

- 🚗 Global deliveries: 3,436 units (-4.4% y/y) vs. consensus of 3,520 units ❌

- 🌍 EMEA deliveries: 1,458 units (-14% y/y) vs. consensus of 1,651 units ❌❌

- 🌎 US deliveries: 1,030 units (+0.8% y/y) vs. consensus of 1,043 units ✅

- 🇨🇳 Shipments from China/HK/TW: 255 units (+7.6% y/y) vs. consensus of 253 units ✅

- 🌏 Other APAC deliveries: 693 units (+9.5% y/y) vs. consensus of 630 units ✅

- 🏎️ Cars & Spare Parts revenue: €1.56 billion (+1.3% y/y) vs. consensus of €1.54 billion ✅

- 📺 Sponsorship/Commercial Revenue: €218 million (+14% y/y) vs. consensus of €203.9 million ✅

- 📦 Revenue forecast for FY2026: ~€7.5 billion (confirmed)

- 🎯 FY2026 EBIT forecast: ≥€2.22 billion (confirmed)

- 💰 Industrial FCF forecast for FY2026: >€1.5 billion (confirmed)

- 📅 Order book: Extended until the end of 2027

- ⚡ Ferrari Luce (electric): Launch in May 2026, price ~€550,000

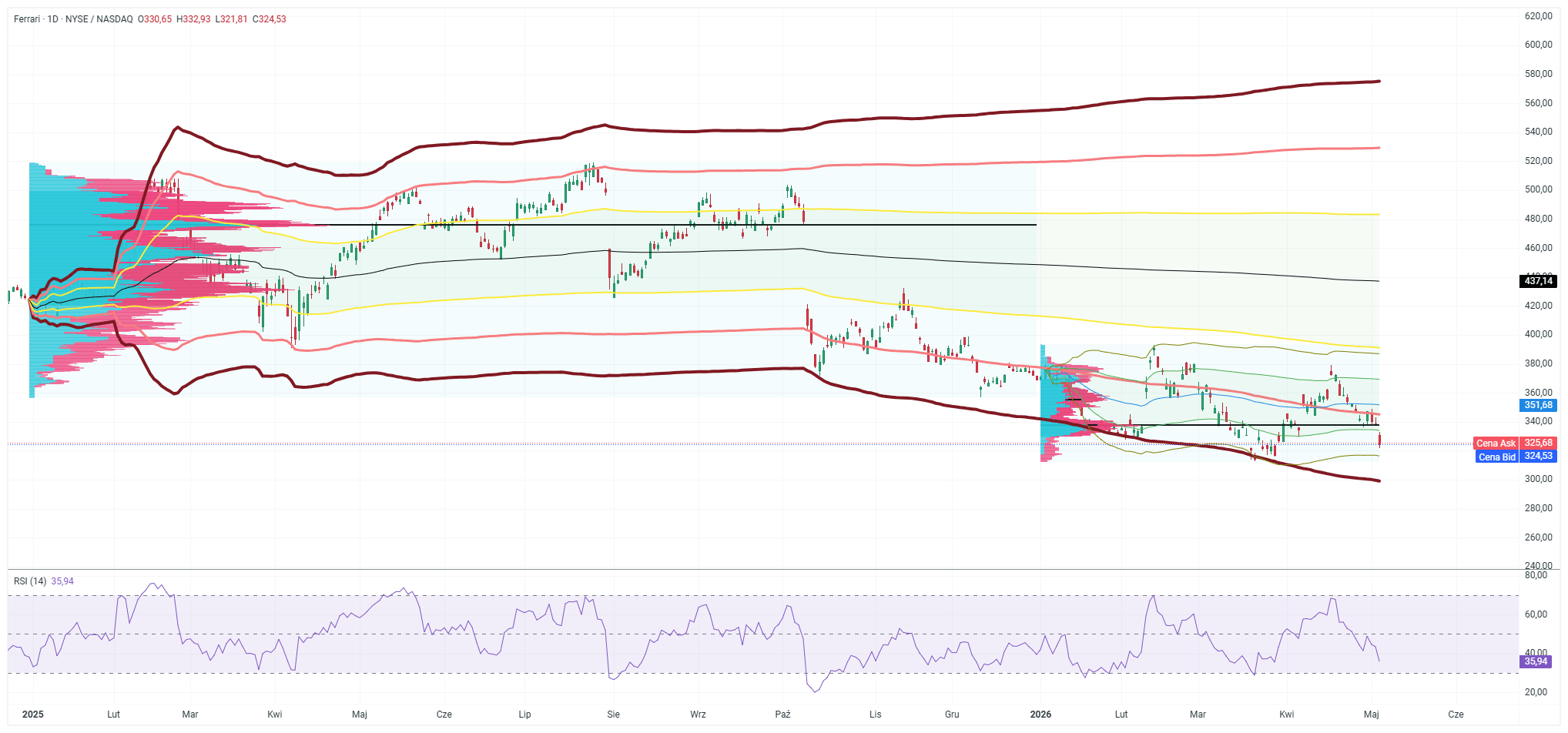

Ferrari shares listed in the US are maintaining a long-term downward trend. Furthermore, recent movements have pushed the shares below the lower boundaries of the VWAP-anchored zones for both the start of 2025 and 2026, indicating that sharp declines continue to dominate the market. In the long term, the company’s generation of substantial free cash flow could allow it to continue its share buyback programme and thereby support value creation for shareholders. However, this does not mean that, in such a scenario, the current trend would come to an end quickly. It appears that the company’s share price is focusing more on the prospects for further growth and, in this regard, is re-evaluating the multiples at which the company is trading. Yesterday, as shown in the chart above, US shares were falling in value, whilst today their Italian counterparts are regaining ground and rising by 3%. However, the overall technical picture remains unchanged in both cases.