Rheinmetall Earninigs – Weak sales overshadow strong prospects

The leader of Europe’s defence industry published the final version of its results ahead of Thursday’s market open. This situation shows how volatile market sentiment can be toward the company and, de facto, the entire sector. Preliminary results released earlier this week showed almost the same figures as the final report, yet the market reacted very differently to similar releases. In the afternoon, shares of the German company are down between 2% and 3%. Financial metrics:

- Sales revenue increased to EUR 1.94bn, representing a 7.7% y/y rise.

- Operating profit rose to EUR 224m (+17% y/y), but still below the consensus of EUR 262m.

- FCF also came in above expectations, rising to EUR 285m versus expectations of EUR 181m.

- Operating margin increased to 11.6% compared with 10.6% a year ago.

- EPS came in at EUR 2.42 versus expectations of around EUR 2.70.

- Backlog increased by 30%, reaching a record EUR 73bn.

Despite strong growth, especially in profitability, investors reacted negatively to sales that came in clearly below expectations. The company disappointed, de facto, across the entire breadth of its operations. Market consensus had assumed sales revenue above EUR 2.1 – 2.2bn. Company guidance: Although the company reported sales and operating profit below expectations, management reassured investors on the conference call that the annual target of 40 – 45% sales growth remains valid. Other highlights:

- Investors may welcome the ramp-up to full-scale production at the ammunition plant in Murcia.

- The market currently appears to pin meaningful near-term hopes on an increase in truck deliveries and the company’s significant expansion in the maritime segment.

- Management explained the weak sales and operating performance mainly by a high comparison base and the characteristics of the sales cycle.

- A series of internal transactions also stands out. Two key management board members, including the CEO, purchased shares with a combined value of nearly EUR 1m.

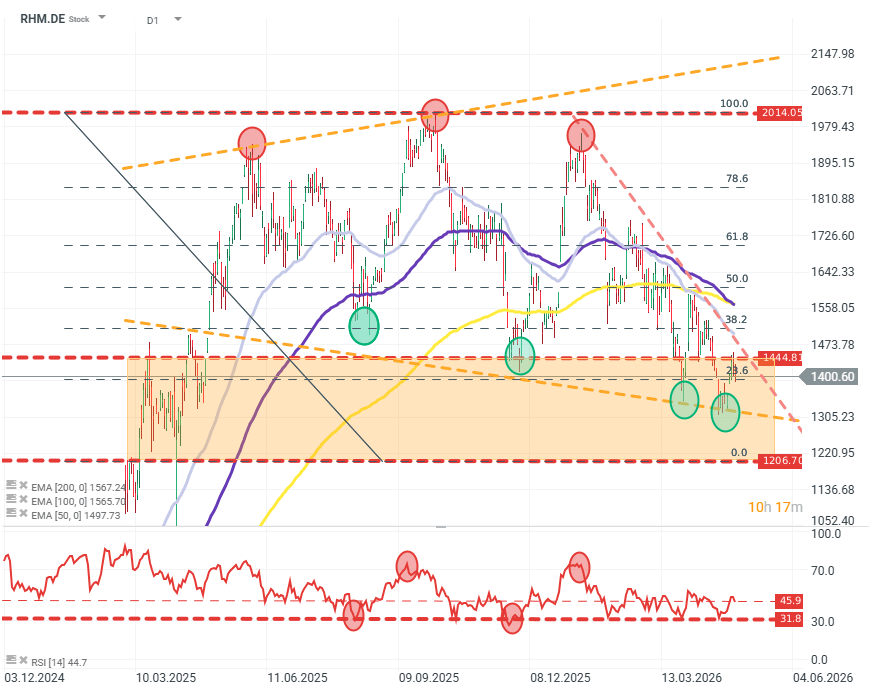

Conclusion: Historically, the first quarters of the financial year have been the weakest for Rheinmetall. This does not reflect a lack of demand, but rather the scheduling of defence contracts. Record backlog alongside rising margins is a strong signal of improving efficiency and solid prospects – sales growth coming in below fairly elevated expectations is merely a single indicator of a temporary slowdown. Insider transactions highlight this clearly. When analysing insider trading, it is worth remembering that there are many reasons to sell, but only one reason to buy shares. RHM.DE (D1)

On the chart, the share price remains in the lower part of a long-term consolidation range. Historically, the price is close to zones and levels (especially RSI) where rebounds have occurred and the price has returned to the upper boundary of the range. From a technical perspective, closely monitoring the EMA100 and EMA200 will be key. Source: xStation5.