Key takeaways

- Oil: Geopolitical deadlock in the Middle East and the threat of Iranian control over the Strait of Hormuz keep prices elevated, though Goldman Sachs tempers sentiment, forecasting an average of $90 as the forward curve stabilizes.

- Natural Gas: Prices are breaking out of their downward trend, fueled by a 14% y/y surge in demand and lower-than-expected inventory builds; forecast US heatwaves open the door to testing the $3.2–$3.4/MMBTU range.

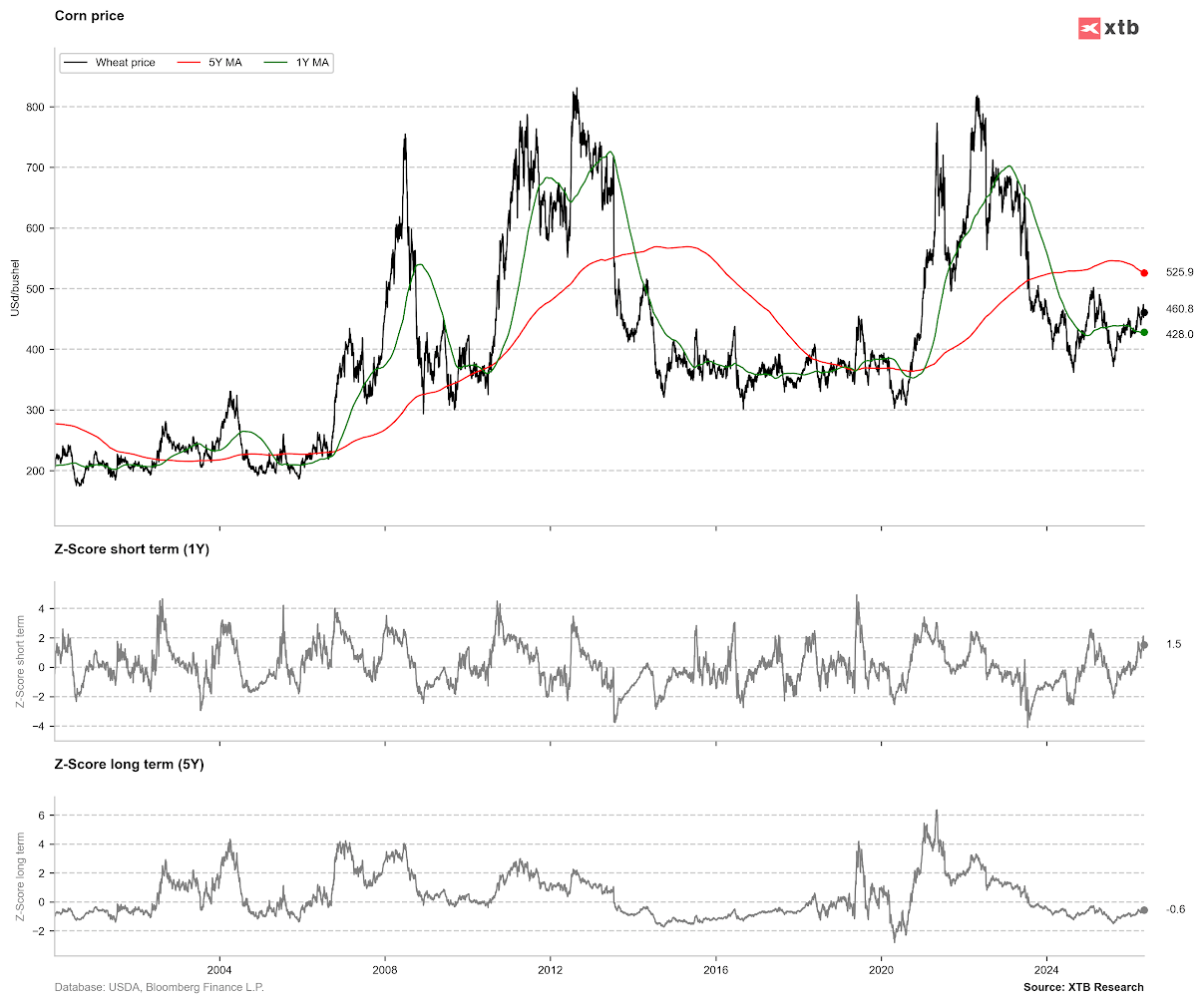

- Corn: The market is tensely awaiting the WASDE report amid record speculative long activity, currently overlooking the fact that US planting (57% complete) is progressing significantly faster than the five-year average.

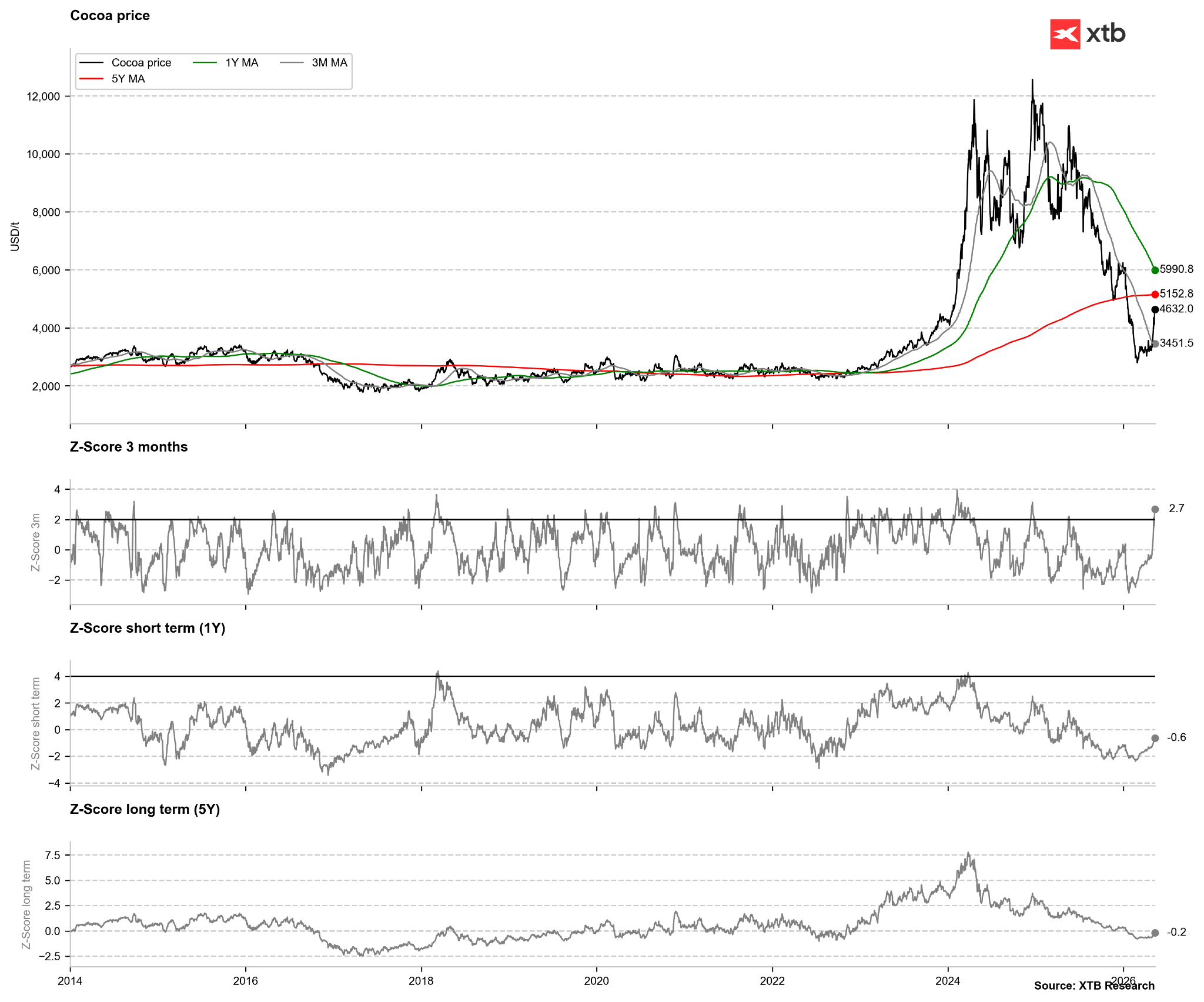

- Cocoa: A speculative 40% rally over the past fortnight, fueled by drought fears, has led to technical overbought conditions—prices may target $7,000 despite weakening demand and projected surpluses in upcoming seasons.

Oil:

- Crude oil prices remain at elevated levels as the geopolitical impasse in the Middle East persists. The US has rejected peace proposals from Iran, which previously stated that conditions proposed by Donald Trump were unacceptable.

- Mr Trump has hinted at a potential resumption of strikes, though action is unlikely before his scheduled meeting with Xi Jinping this Thursday.

- Reports suggest that Pakistan has been presenting overly “sanitised” versions of the US and Iranian positions, leading to misunderstandings and a lack of diplomatic progress.

- Tehran is demanding the lifting of the US maritime blockade and sanctions, alongside recognition of Iranian sovereignty over the Strait of Hormuz. Such a move could allow Iran to impose transit fees or control volumes through this vital energy artery.

- Saudi Arabia and Kuwait have moved to lift restrictions on US military access to their respective bases.

- Goldman Sachs noted in a recent report that current tensions in oil and fuel markets have had a limited impact on the global economy. Existing inventories are offsetting tight supply and demand destruction.

- While Goldman’s extreme scenario envisions prices reaching $140 per barrel by June, its base case forecasts near-term consolidation followed by a decline to an average of $90 this year.

- Trade rerouting has provided a significant cushion. The US is boosting exports, particularly to Asia, while China is sharply reducing seaborne imports by drawing down its substantial domestic stockpiles. However, a potential closure of the Strait of Hormuz after June could trigger physical market tightness exceeding that seen in April.

- Physical-to-front-month spreads have retreated to levels last seen in January and February. Nonetheless, a resurgence in Chinese or Asian import demand could reintroduce volatility.

- The forward curve suggests the market is adjusting to a new reality. Long-dated contracts have risen notably month-on-month, leading to a visible narrowing of calendar spreads.

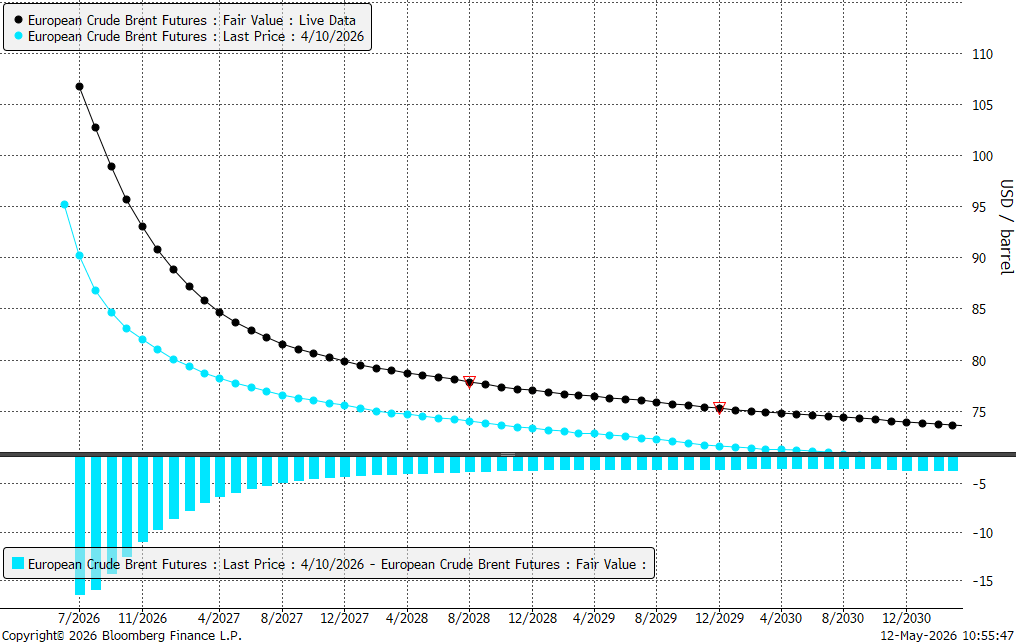

The market remains in steep backwardation, though curve differentials are narrowing. Medium-term price expectations are rising in tandem; the market is currently pricing December 2027 delivery at $80 per barrel as it continues to stabilise. Source: Bloomberg Finance LP

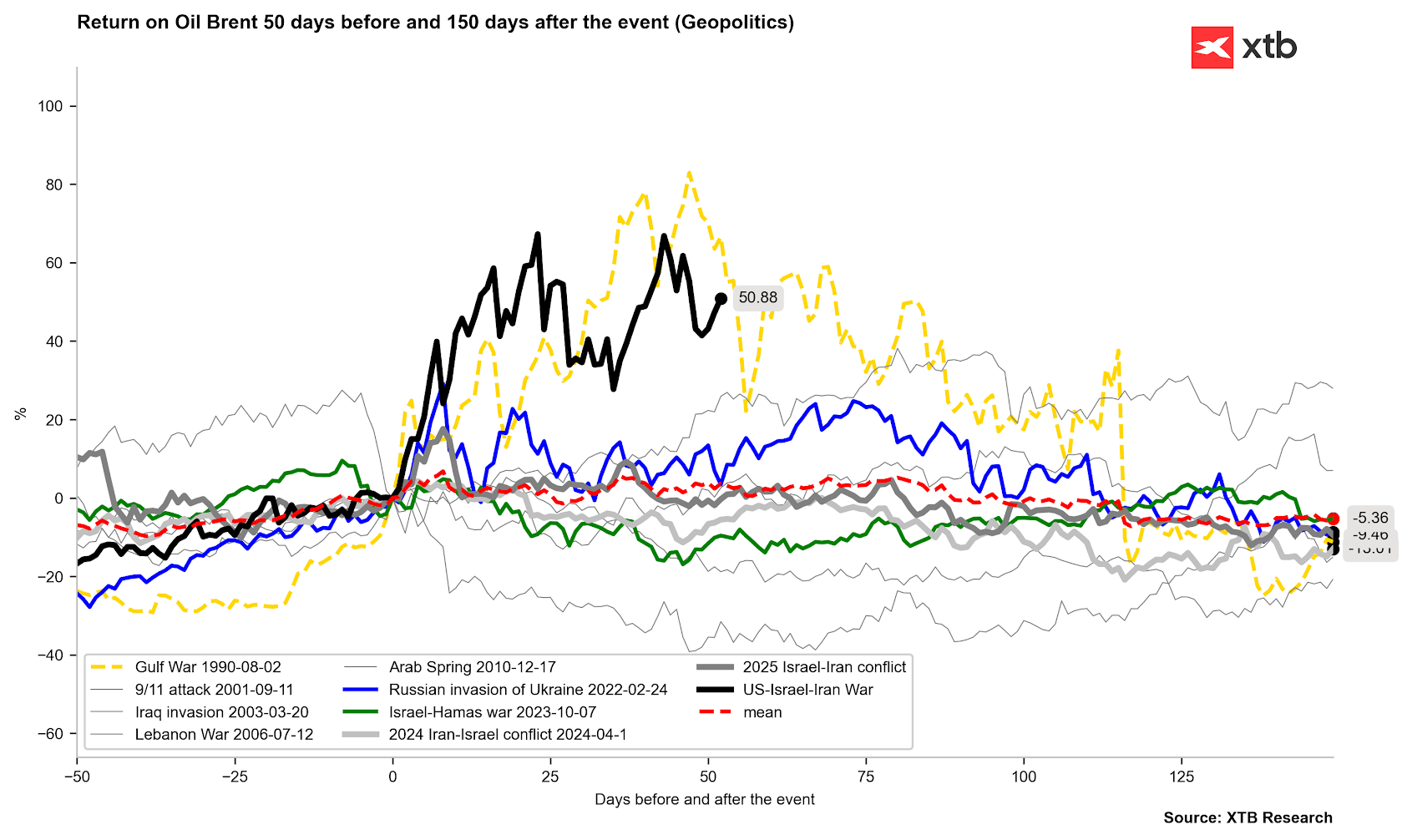

Historical patterns suggest we are approaching a pivotal juncture. A return to aggressive growth would signal a complete paradigm shift, though the current energy crisis already stands as the most significant in history—despite its potential for a swift resolution. Source: Bloomberg Finance LP, XTB

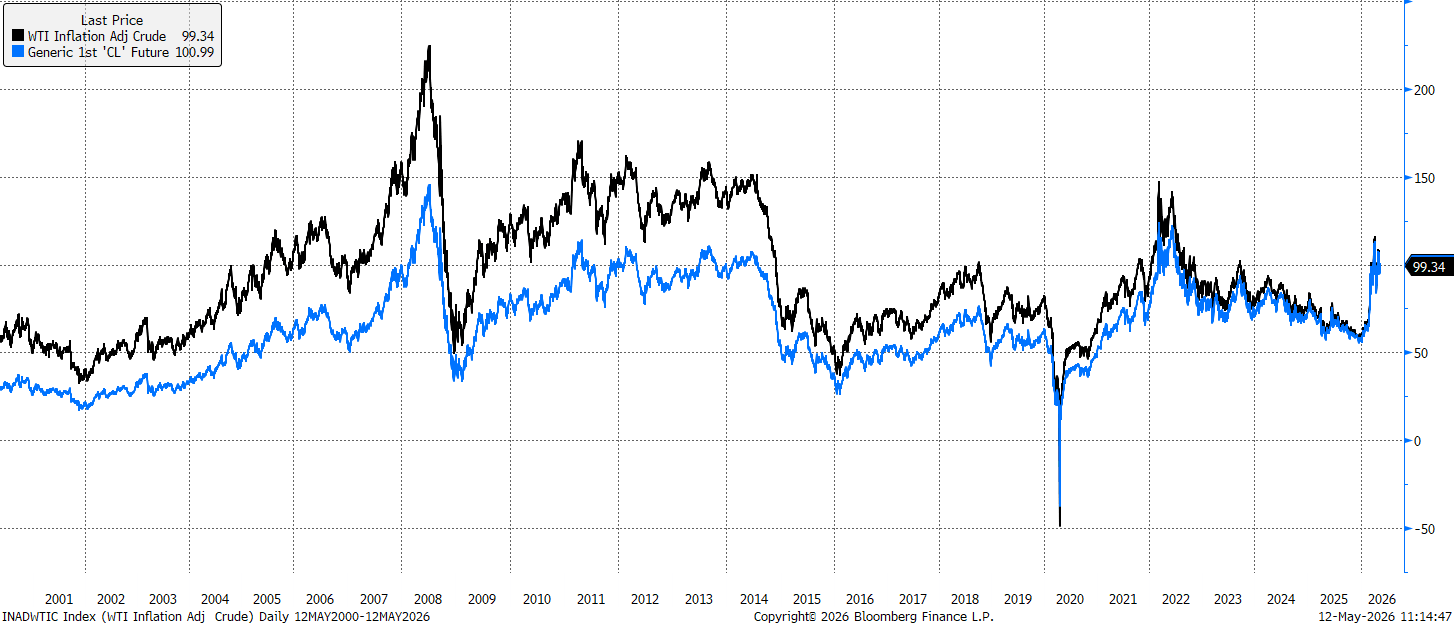

Global markets appear resilient to current price levels. When adjusted for inflation, 2022 prices would equate to nearly $150 per barrel, while the 2008 peak would represent $225 today. This suggests that meaningful demand destruction may require significantly higher prices. Currently, demand is being curtailed more by limited availability than by outright cost. A surge to $150-$200 could necessitate a sustained reduction in consumption of up to 5m barrels per day. Source: Bloomberg Finance LP Natural Gas:

- Natural gas prices rallied in early May on expectations of recovering demand and potential production curbs, which are forecast to slow inventory builds relative to seasonal averages.

- The push for increased US LNG exports persists, though further growth is currently constrained by liquefaction capacity.

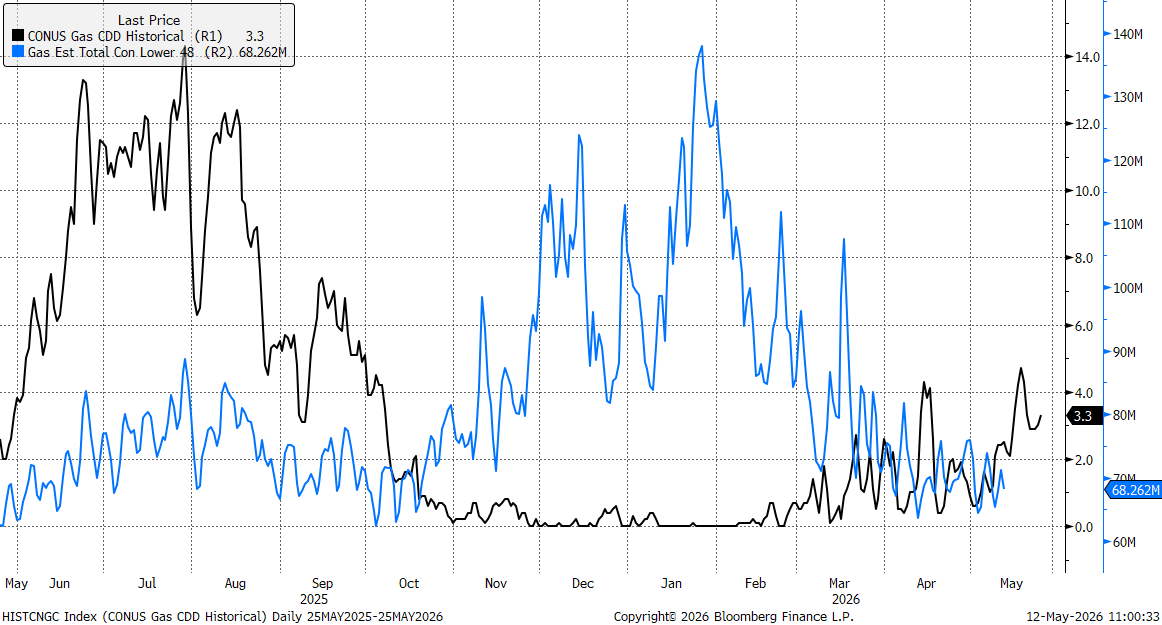

- Monday’s demand reached 69.1 bcfd, an increase of nearly 14% compared to the previous year.

- The latest storage report showed an injection of 63 bcf, trailing both market expectations of 72 bcf and the five-year average of 77 bcf.

- Pipeline bottlenecks in the Permian Basin continue to suppress prices at the Waha hub in West Texas. Prices there have remained in negative territory relative to the benchmark for 66 consecutive days.

- Negative pricing is sustained by the fact that gas is produced as a byproduct of oil extraction in the Permian, the premier US shale oil region.

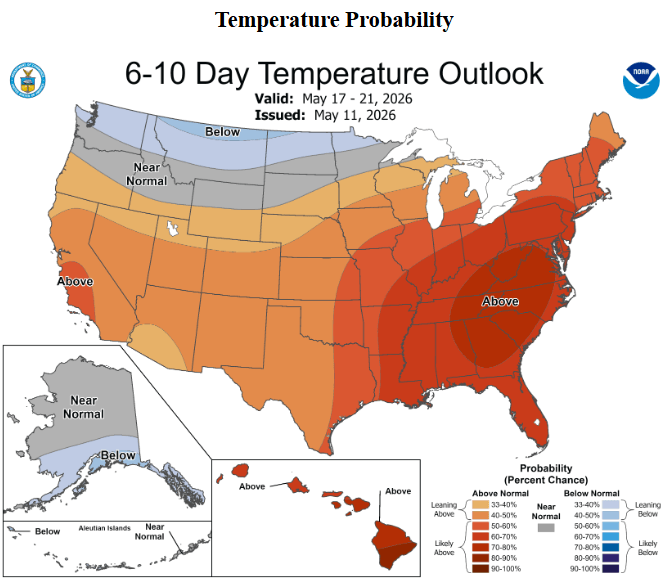

Short-term weather forecasts indicate above-average temperatures across the US, potentially driving cooling demand above seasonal norms. Source: NOAA

Cooling degree days remain below the five-year average, yet overall demand is tracking higher than historical norms. Source: Bloomberg Finance LP

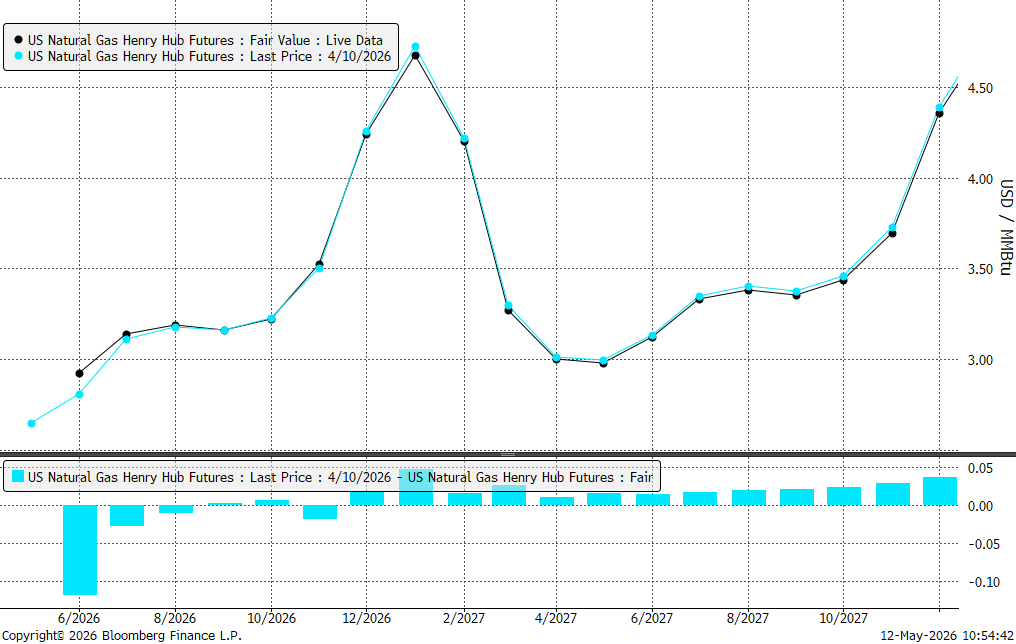

The forward curve for natural gas is largely unchanged from last month, barring a slight uptick in the front-month contract. Rising demand could see prices test the July-September contracts, currently trading around $3.1-$3.2/MMBTU. Source: Bloomberg Finance LP

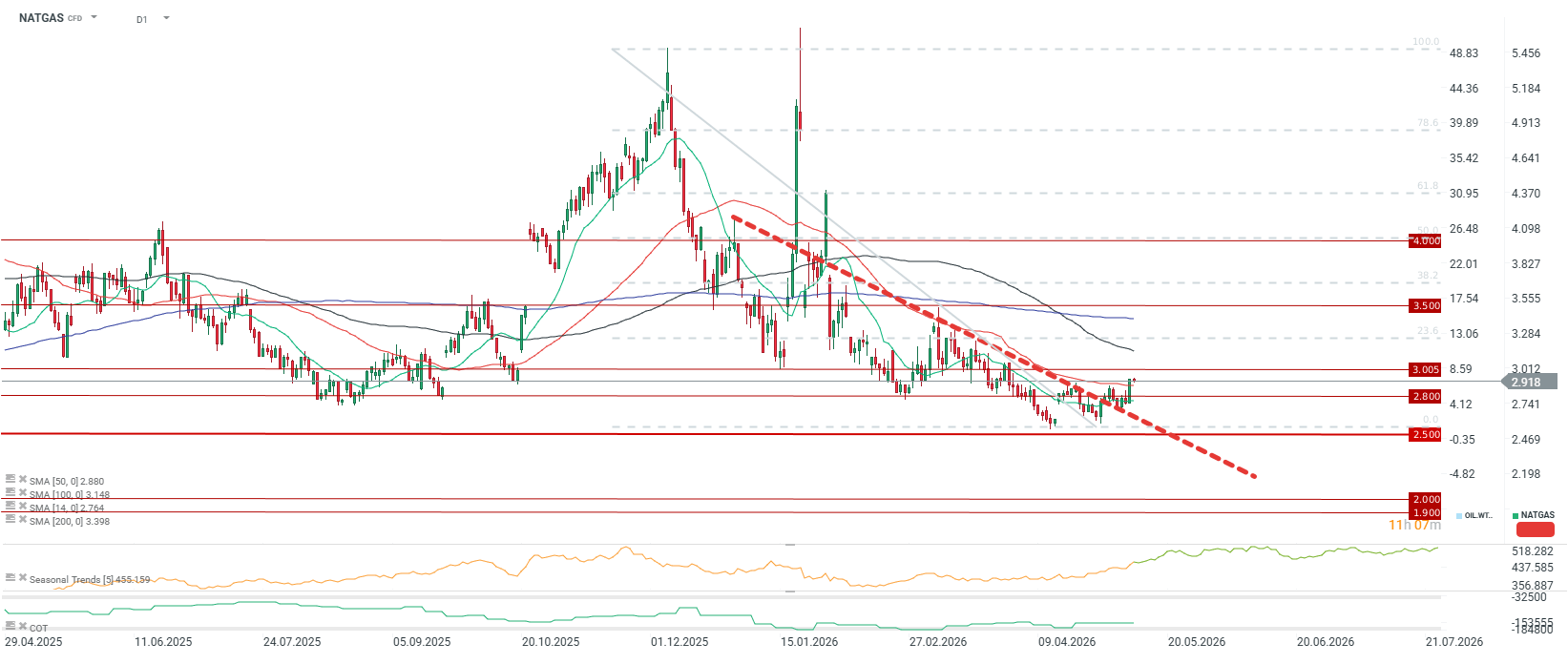

Prices are breaking out of a downward trend, moving above the 14-period moving average that has acted as resistance since January. Should this breakout hold post-rollover on May 18th, the next target is the $3.2-$3.4 range, near the 200-period average. Source: xStation5 Corn:

- The USDA is set to release its WASDE report later today, providing the first full outlook for the 24/25 US season and global supply-demand estimates.

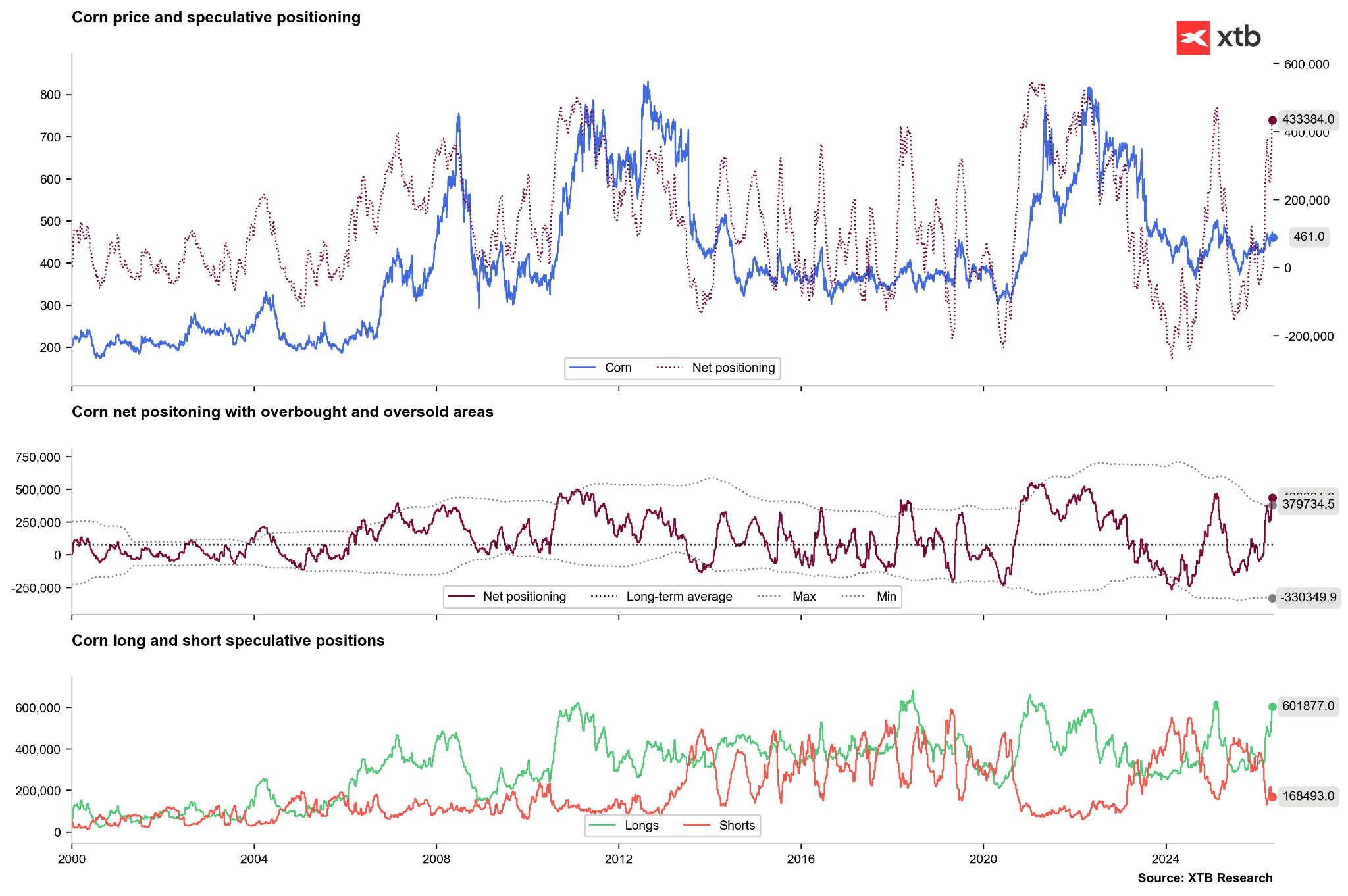

- Speculative investors are notably increasing long positions across agricultural commodities, with a particular focus on corn.

- US planting progress is significantly ahead of schedule. The latest report shows 57% completion, versus a five-year average of 52%. Emergence stands at 23%, four percentage points above the norm.

- The pivotal May WASDE report, offering the first projections for the upcoming season, is due at 18:00 CET today.

- The report is expected to show a marginal increase in old-crop ending stocks to 2.13bn bushels. Globally, ending stock estimates were revised higher in April.

- Investors anticipate stronger export demand and a drop in US ending stocks to the 1.8-1.9bn bushel range, based on 95.3m planted acres and a yield of 183 bushels per acre.

There is a pronounced build-up of speculative long positions in corn, following a reduction in shorts. Net positions are at their highest since February 2025, a period that previously triggered a contrarian signal. While market conditions are not dire, increased export pressure could support prices, which remain historically low. Source: Bloomberg Finance LP, XTB

Technically, while the price has deviated significantly from the one-year average, it has not yet reached overbought levels (2-3 standard deviations). The current setup mirrors the 2014-2020 period, though a fertiliser-related crisis could echo the volatility of 2021-2022. Source: Bloomberg Finance LP, XTB

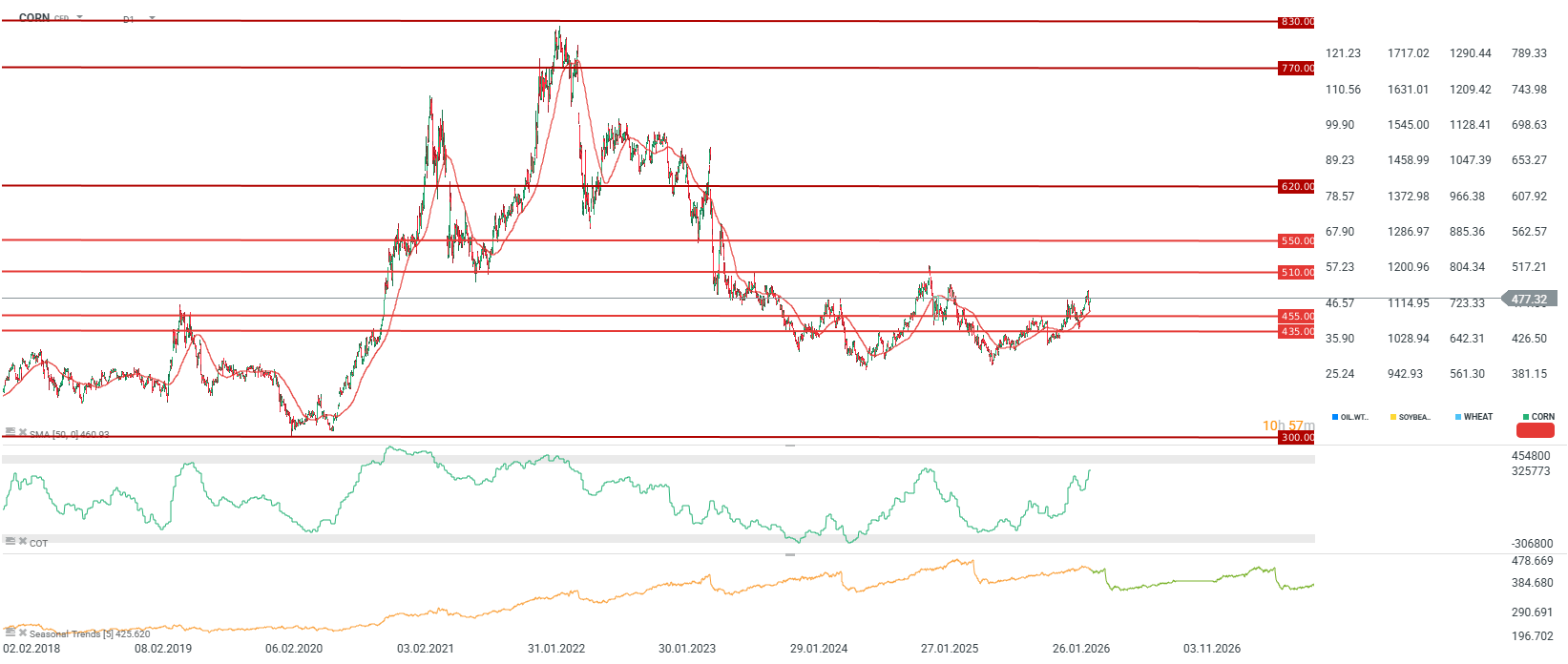

Historically, the corn market exhibits strong seasonality around mid-June, often marked by sharp sell-offs. A Middle Eastern peace deal in the coming weeks could trigger another correction, though likely less severe than the downturns of 2022-2024. Source: xStation5 Cocoa:

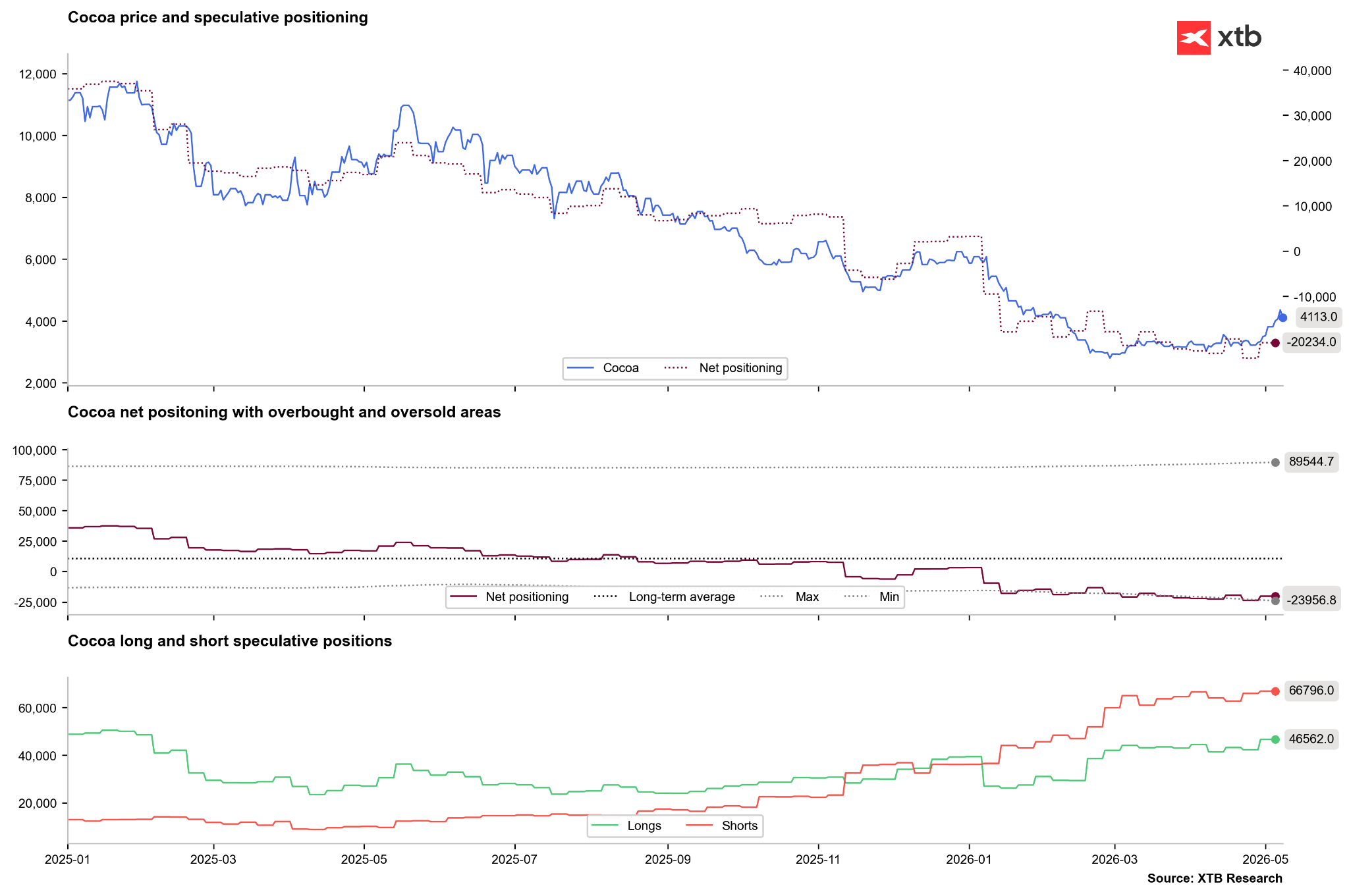

- Drought concerns and fears of a short squeeze have fuelled a 40% rally in cocoa prices over the past fortnight.

- Fundamentally, the market remains unchanged. Panic covering of short positions has not materialised in New York, and London saw only symbolic activity.

- Demand remains subdued; current price gains are driven by anxiety over the next season, despite expectations of a significant surplus.

- Prices have breached key resistance, including the upper bound of the downward channel and the 50% retracement of the recent bearish impulse.

- The CCI indicator is nearing multi-year averages; overvaluation levels would likely be reached around the $6,900–$7,000 per tonne mark.

- Financial results from Hershey and Mondelez indicate that consumer demand is beginning to stabilise.

- StoneX has revised its surplus forecast for the 2026/2027 season down to 149k tonnes, from an initial January estimate of 267k tonnes.

Prices are nearly three standard deviations above the 100-period moving average, suggesting short-term overvaluation, though historical peaks have seen four-fold deviations. Source: Bloomberg Finance LP, XTB

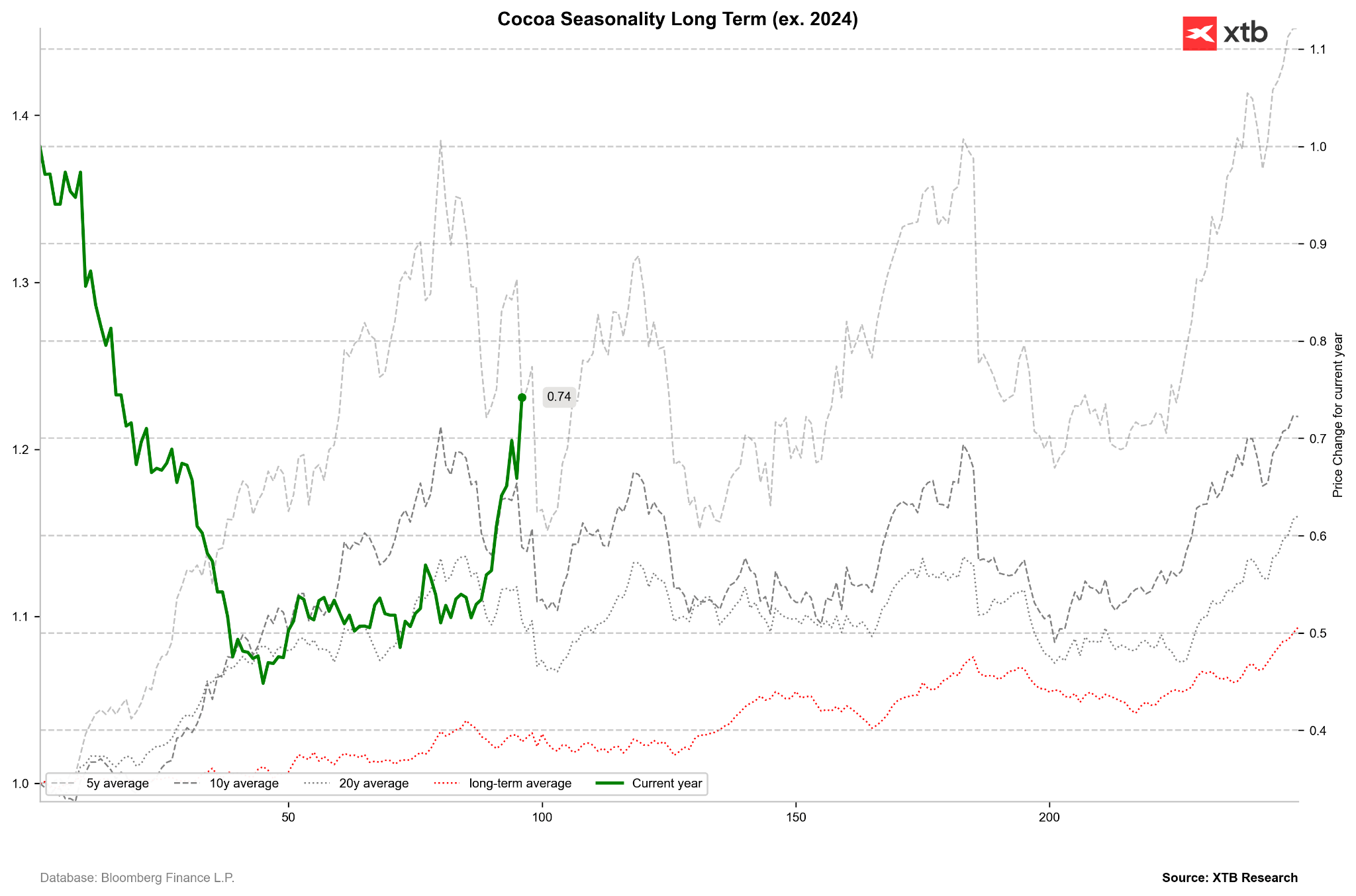

The current rally aligns with seasonal trends typically seen four months into the year. If cyclical patterns hold, a correction may follow within a month. Notably, this upturn began earlier than usual after a particularly bearish start to the year. Source: Bloomberg Finance LP, XTB

Short interest in New York remains high, with no immediate signs of a short squeeze. Source: Bloomberg Finance LP, XTB