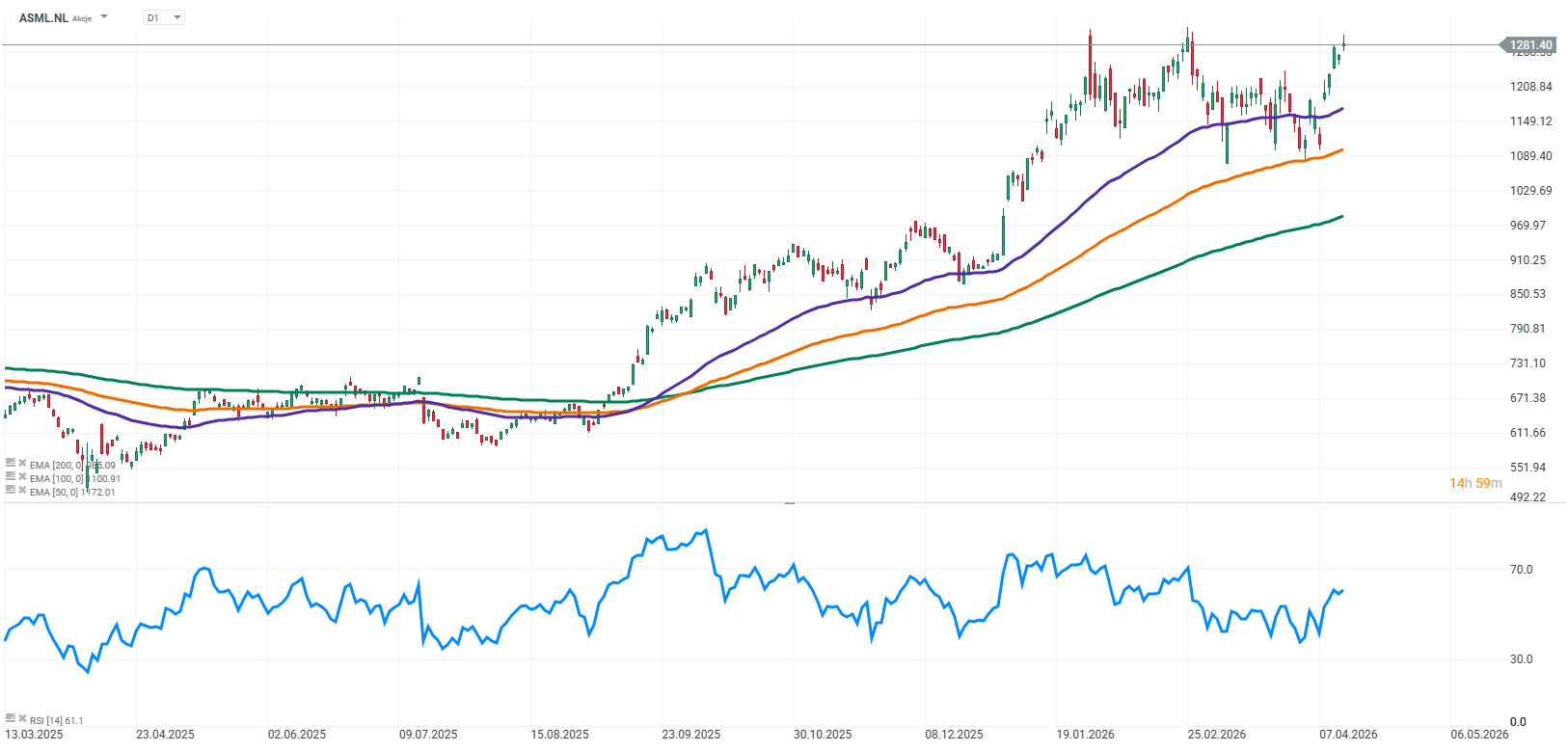

ASML Earnings: strong start to the year and a signal of a continued chip boom!

ASML delivered a very strong first quarter of 2026, with results landing in the upper end of its own guidance range and earnings per share coming in above analyst consensus. At the same time, the company raised its full-year outlook, which in the current macroeconomic and geopolitical environment is a very strong signal of demand durability. The report clearly shows that the key growth driver remains artificial intelligence infrastructure, while the semiconductor investment cycle continues to strengthen. Management also communicated that 2026 is expected to be another year of growth across all segments, with the updated guidance range explicitly incorporating potential impacts from export restrictions. In practice, this means that even under a more adverse regulatory scenario, the company still expects growth, which significantly strengthens the credibility of the outlook and points to very strong underlying demand fundamentals. Key financial results

- Revenue: EUR 8.8bn (reported EUR 8.767bn)

- Net income: EUR 2.8bn (reported EUR 2.757bn)

- Earnings per share (EPS): EUR 7.15 (approx. EUR +0.54 above consensus)

- Gross margin: 53.0% (top end of guidance range)

- Installed Base (services and modernization): ~EUR 2.5bn

- System sales: 67 new systems + 12 used systems

- Share buybacks: ~EUR 1.1bn in Q1

- 2025 dividend: EUR 7.50 per share (+17% YoY)

Financial performance and earnings quality The most important aspect of the report is not only the scale of revenues, but their quality. The EUR 8.8bn revenue level confirms sustained very strong demand, with no visible signs of demand cooling. Net income and EPS demonstrate very strong conversion of revenue into bottom-line profit. For ASML, this is particularly important as its business model is based on extremely high-value capital equipment, which requires strong operational efficiency. A gross margin of 53% is one of the strongest indicators of business quality. It reflects both the company’s dominant technological position and an increasing contribution from higher-margin business segments. Importantly, this is not a one-off effect but rather a more structural shift in the revenue mix. Installed Base as a core pillar of the business model The Installed Base segment refers to the installed base of machines already operating at customer sites. In practice, it includes service, upgrades, spare parts, additional options, and software that enhances system performance. Installed Base generated approximately EUR 2.5bn in revenue, indicating a meaningful and growing share of total results. Crucially, this is a higher-margin, more recurring, and less cyclical business compared to equipment sales. In the current environment, its importance is increasing further. Customers, constrained by limited availability of new tools and long lead times, are focusing on maximizing the productivity of existing equipment. Upgrades and service become the fastest way to expand effective production capacity. From a strategic perspective, this represents a shift toward a more stable and predictable earnings and cash flow profile, which is particularly important in a historically highly cyclical industry. Demand, AI, and the changing cycle The key takeaway from the report is simple: chip demand currently exceeds supply. Customers, especially in the memory segment, are already indicating that 2026 capacity is largely sold out, and they expect supply constraints to persist beyond that period. The main driver is the rapid expansion of artificial intelligence, which is fueling massive investment in new manufacturing capacity. At the same time, semiconductor manufacturers are building new fabs and advancing more sophisticated process technologies, which increases the number of steps required to produce a single chip. In practical terms, this translates into higher demand for lithography systems, which are the core products of ASML. For the company, this is highly favorable, as increased process complexity directly translates into stronger demand for its technologies. Q2 guidance The second-quarter outlook calls for revenue in the range of EUR 8.4bn to 9.0bn, with Installed Base revenue expected to remain around EUR 2.5bn. Gross margin is expected to come in between 51% and 52%, which represents a slight decline versus the exceptionally strong Q1, but still remains at historically elevated levels. Operating expenses include approximately EUR 1.2bn in R&D and around EUR 0.3bn in SG&A, reflecting continued heavy investment in EUV and other advanced technology development. Raised full-year outlook and its implications The company raised its 2026 revenue guidance to EUR 36bn to 40bn, up from the previous range of EUR 34bn to 39bn. Even more importantly, the gross margin guidance was maintained at 51% to 53%, suggesting a durable improvement in profitability structure. Management emphasized that this range incorporates potential scenarios related to export controls, particularly in relation to China. In practice, this implies that demand from other regions, including the United States, Europe, and the rest of Asia, is strong enough to offset potential restrictions. Capacity constraints and supply limitations One of the most important conclusions is that the main constraint on growth is not demand, but production capacity. The company plans to reach at least 60 EUV system deliveries in 2026, with the potential to increase this to around 80 systems in 2027 under favorable conditions. Manufacturing these systems is highly complex and time-consuming, meaning supply increases only gradually. As a result, ASML operates in an environment of structural supply shortage, which represents a fundamental shift compared to previous semiconductor cycles. Risks The most important risk remains geopolitics and potential export restrictions, particularly regarding China. Customer concentration is also a key factor, as the company depends heavily on investment decisions by a small number of leading semiconductor manufacturers. In addition, the long production cycle of its systems limits flexibility in responding to demand changes. Opportunities and growth drivers The primary growth driver remains artificial intelligence, which is fueling investment in data centers and advanced semiconductor chips. ASML sits at the center of the global semiconductor ecosystem as a critical technology supplier. In addition, rising investment in regional supply chains and government support for semiconductor independence further strengthen long-term demand. Outlook In the coming quarters, the key focus will be sustaining strong demand and continuing to scale production capacity. If the current AI-driven trend persists, ASML may be entering a multi-year structural growth cycle. However, the main uncertainty remains geopolitical developments and the pace of technological adoption. Key conclusions The first quarter of 2026 was very strong for ASML, both in terms of growth dynamics and earnings quality. The company not only beat expectations but also raised guidance, which is a strong signal for the market. The report confirms that the business is undergoing a structural shift toward higher stability, stronger profitability, and greater predictability. The AI boom continues to provide a long-term growth foundation, and ASML remains one of the key beneficiaries of this global trend.

Source: xStation5

The material on this page does not constitute financial advice and does not take into account your level of understanding, investment objectives, financial situation or any other specific needs. All information provided, including opinions, market research, mathematical results and technical analyzes published on the Website or transmitted To you by other means, it is provided for information purposes only and should in no way be construed as an offer or solicitation for a transaction in any financial instrument, nor should the information provided be construed as advice of a legal or financial nature on which any investment decisions you make should be based exclusively To your level of understanding, investment objectives, financial situation, or other specific needs, any decision to act on the information published on the Website or sent to you by other means is entirely at your own risk if you In doubt or unsure about your understanding of a particular product, instrument, service or transaction, you should seek professional or legal advice before trading. Investing in CFDs carries a high level of risk, as they are leveraged products and have small movements Often the market can result in much larger movements in the value of your investment, and this can work against you or in your favor. Please ensure you fully understand the risks involved, taking into account investments objectives and level of experience, before trading and, if necessary, seek independent advice.